Attitudes to governance, risk and compliance (GRC) activities are changing among Tier 1 financial institutions. The need to keep up with rapid regulatory change, and the pressure of larger, more publicised penalties dealt out by regulators in recent years have prompted an evolution in how risk is viewed and managed. Financial firms also face an increasingly volatile market environment that requires them to remain nimble – not just to survive, but to thrive.

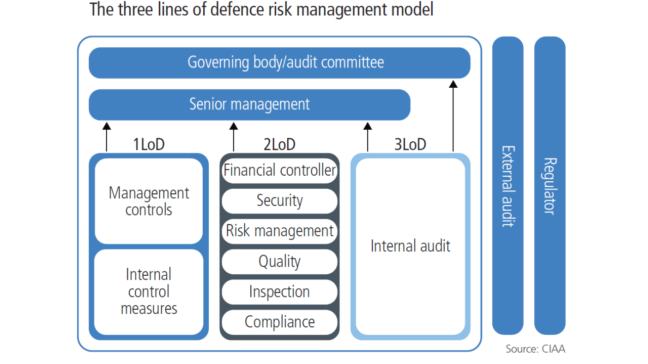

As a result of these market developments, GRC is now seen, rather than as one strand of the business, as a far more integrated activity with many companies realigning resources around the ‘three lines of defence’ model. GRC is increasingly being treated as an enterprise-wide responsibility by organisations that are successfully navigating these challenging times for global financial markets. This shift in attitudes is also leading to a rethink in relation to the tools used by all three lines of defence to participate in GRC activities. Some are exploring more innovative solutions to support and engage infrequent users – particularly those in the first line of defence (1LoD). The more intuitive design of such tools enables these users to take a more active role in risk-aware decision-making.

These and other innovations promise to bring greater effectiveness and efficiency to an area into which firms have channelled increasing levels of resource in recent years but are struggling to keep up with demand. A recent survey carried out by Risk.net and IBM found that risk and compliance professionals acknowledge the limitations of existing operational risk and regulatory compliance tools and systems to satisfy current and future GRC requirements. The survey polled 106 senior risk, compliance, audit and legal executives at financial firms including banks (53%), insurance companies (21%) and asset management firms (12%). The results revealed that nearly one third of these respondents remain unimpressed with the effectiveness of their organisation’s ability to cope with the complexity and pace of regulatory change. Nearly half gave a similar response regarding their organisation’s efficiency in this area.

With these issues in mind, many of the firms surveyed have started to explore user-experience needs more deeply and combine the results with artificial intelligence (AI) capabilities to further develop GRC systems and processes. These capabilities are designed to enhance compliance systems and processes and make them more intuitive for all. As such, user-experience research and design has become a key consideration for organisations wanting to ensure employees across all three lines of defence can participate more fully in GRC activities. In addition, AI-powered tools can help 1LoD business users better manage risk and ensure compliance by increasing the efficiency and effectiveness of these GRC systems and processes. The survey shows that, while some organisations are already developing these types of solutions, there is still room for greater understanding of the benefits of new and innovative forms of technology throughout the global financial markets. For instance, nearly half of respondents to the survey, when asked about the benefits of AI for GRC activities, were unsure of the potential time efficiencies such tools can bring. More than one-quarter were undecided on whether AI would free up employees’ time to focus on more strategic tasks.

Many organisations are still considering how to move forward in this area, but it will be those that truly embrace user-focused tools and leverage innovative technologies such as AI and advanced analytics to increase efficiencies that can expect to reap the rewards of successfully managing regulatory change and tackling market volatility.

Current and Future Applications

The survey highlights that financial firms already recognise that these solutions can be used to more efficiently manage the regulatory change process. For example, AI-based solutions can provide smart alerts to highlight the most relevant regulatory changes – 35% of survey respondents see AI as offering the biggest potential improvements in this area.

Improving the speed and accuracy of classification and reporting of information – for example, in relation to loss events – was another area identified for its high AI potential. Nearly one-third of respondents (31%) see possibilities for improvement of current GRC processes in this area. Some financial firms have already started to reap the rewards of this type of approach. Larger firms are typically ahead of the game with such developments, often having more resources to put into research and development. Out of the 13% of larger firms that have seen a decrease in GRC resources over the past year, one-third of survey respondents attribute that to “tools and automation improvements”.

Similarly, 44% of those polled work at organisations already making improvements to improve end-to-end time and user experience in relation to GRC processes and tools. A further 19% plan to do this in the next 12 months and, in line with this, 64% of survey respondents expect their firm’s GRC resources to increase over the next 24 months (see figure 8). While it is not clear from the survey whether these additional resources will be specifically directed towards AI, more than 80% of respondents work at organisations currently considering AI for a range of GRC activities.

The most popular use of AI among financial firms is to improve the speed and/or accuracy of classification and reporting information, such as loss events – 19% of respondents say their organisation is currently using AI for this purpose, with 81% currently considering this type of use. Such events happen fairly infrequently, so training employees to classify and enter such information can be time consuming, but incorrect classification can have a real impact on data quality. By using natural language processing (NLP) tools to understand and categorise loss events automatically, organisations can streamline the time and resources required to train employees to collect and manage this information.

According to the survey, 83% of respondents are also currently considering the use of AI tools to develop smart alerts that will highlight any new rules or updates to existing regulations, helping financial firms manage regulatory change more efficiently. Many organisations already receive an overwhelming amount of alerts every day relating to new rules or changes, but some or all of these changes may not actually apply to their businesses. AI can be used to tailor these alerts to ensure compliance teams only receive the most relevant alerts. Using NLP to create this mechanism can be the difference between sorting through 100 alerts in one day and receiving one smart alert that has been identified by an AI-powered solution.

Control mapping is another area to which AI can add value. When putting controls in place relating to specific obligations within a regulation, for example, compliance teams can either create a new control or, using NLP, detect whether there is already an applicable control in place that can be mapped to record the organisation’s compliance with the rule. This reduces the amount of time spent by the team reading and understanding new legislation or rule changes to determine applicability, as well as improving accuracy and reducing duplicate controls.