Since the start of the Third Industrial Revolution in the 1980s, the world has changed in many different ways:

- rapid introduction and adoption of technological innovation (global internet; social networks; mobile technologies; evolving payment solutions; data availability);

- new economic realities (volatile and shorter economic cycles; interconnected financial climate; under utilisation of assets);

- structural shifts in society’s values (desire for community; generational altruism; active citizenship);

- and demographic readjustment (increasing population; urbanization; longer life expectancy; millennials in the work force).

While these changes have been happening, the Insurance industry has seemingly preferred to operate in a closed environment oblivious to much of the impact these changes could bring:

- Resistance to change,

- Failure to meet changing customer demands

- Decrease in the importance of attritional risks

has led the Insurance industry to reduce its relevance.

However

- the availability of data,

- the introduction of new capital providers,

- the impact of new business models emerging from the sharing economy

- and the challenge of InsurTechs

are affecting the industry complacency. Collectively, these factors are creating the perfect storm for the incumbents allowing them to re-evaluate their preference for maintaining the status quo. There is an ever increasing expectation from the industry to be more innovative and deliver a vastly improved customer experience.

As data and emerging technology are accelerating the need for change, they are also opening doors. The industry is at cross roads where it can either choose to regain relevance by adapting to the new world order or it can continue to decline. Should it choose the latter, it could expose the US$ 5 trillion market to approaches from large technology firms and manufacturers who have the access to customers, transformational capabilities and more than enough capital to fill the void left by the traditional players.

Insurance industry is slow to evolve

The Insurance industry has historically lacked an appetite to evolve and has shown reluctance in adopting industry-wide changes. A number of key elements, have created high barriers to entry. New entrants have found it difficult to challenge the status quo and lack appetite to win market share from incumbents with significantly large balance sheets. Such high barriers have kept the impact of disruption to minimal, allowing the industry to stay complacent even when most other industries have undergone significant structural shifts. In many ways ‘Darwin’ has not been at work.

- A complex value chain

The Insurance industry started with a simple value chain involving four roles – the insured, a broker who advices the insured, an underwriter who prices the risk and an investor who provides the capital to secure the risk. Over centuries, the chain has expanded to include multiple other roles essential in helping the spreading of large risks across a broad investor community, as shown below.

These new parties have benefitted the chain by providing expertise, access to customers, secure handling of transactions, arbitration in case of disputes and spreading of risk coverage across multiple partners. However, this has also resulted in added complexities and inefficiencies as each risk now undergoes multiple handovers.

While a longer value chain offers opportunities to new entrants to attack at multiple points, the added complexities and the importance of scale reduces opportunities to cause real disruption.

- Stringent regulations

Insurance is one of the highest regulated industries in the world. And since the global financial crisis of last decade, when governments across the globe bailed out several financial service providers including insurers, the focus on capital adequacy and customer safety has increased manifold.

While a proactive regulatory regime ensures a healthy operating standard with potential measures in place to avoid another financial meltdown, multiple surveys have highlighted the implications of increased regulatory burden, leading to increased costs and limited product innovation.

- Scale and volatility of losses

The true value of any insurance product is realised when the customer receives payments for incurred losses. This means that insurers must maintain enough reserves at any time to meet these claims.

Over the years volatility in high severity losses have made it difficult for insurers to accurately predict the required capital levels.

In addition, regulators now require insurers to be adequately capitalised with enough buffer to sustain extreme losses for even the lowest probability of occurrence (for example 1-in-100 years event or 1-in-200 years event). This puts additional pressure on the insurers to maintain bulky balance sheets.

On the other hand, a large capital base gives established insurers advantage of scale and limits growth opportunities for smaller industry players/new entrants.

- Need for proprietary and historical data

Accurate pricing of the risk is key to survival in the industry. The insurers (specifically underwriters supported by actuaries) rely excessively on experience and statistical analysis to determine the premiums that they would be willing to take to cover the risk.

Access to correct and historical data is of chief importance and has been a key differentiating factor amongst insurers. Since the dawn of Third Industrial Revolution in the 1980s, insurers have been involved in a race to acquire, store and develop proprietary databases that allow them to price risks better than the competitors.

The collection of these extensive databases by incumbent insurers have given them immense benefits over new entrants that do not typically have similar datasets. Additionally, the incumbents have continued to add on to these databases through an unchallenged continuation of underwriting– which has further widened the gap for new entrants.

Struggling to meet customer needs

Despite years of existence, the Insurance industry has failed to keep up with the demand for risk coverage. For example the economic value of losses from all natural disasters has consistently been more than the insured value of losses by an average multiple of 3x-4x.

The gap is not limited to natural disasters. As highlighted by Aon’s Global Risk Management Survey 2019, multiple top risks sighted by customers are either uninsurable or partially insurable leading to significant supply gap.

Six of the top 10 risks, including Damage to reputation/brand and Cyber, require better data and analytical insights to achieve fully effective risk transfer. However, current capabilities are primarily applied to drive better pricing and claims certainty across existing risk pools, and have not yet reached their full potential for emerging risks.

This inability to meet customer need has been driven by both an expensive model (for most risks only 60% of premiums paid are actually returned to the insured) and a lack of innovation. Historically, the need for long data trends meant insurance products always trailed emerging risks.

Status Quo is being challenged

While the industry has been losing relevance, it is now facing new challenges which are creating pressure for change. While these challenges are impacting the incumbents they also provide the potential for insurance to regain its key role in supporting innovation. Creating opportunity for lower costs and new innovations.

The insurance customer landscape has changed considerably: traditional property and casualty losses are no longer the only main risks that corporations are focused on mitigating. The importance of intellectual property and brand/reputation in value creation is leading to a realignment in the customer risk profile.

Value in the corporate world is no longer driven by physical/ tangible assets. As technology has advanced, it has led to the growth of intangibles assets in the form of intellectual property. The graph below shows that 84% of market capitalization in 2018 was driven by intangible assets. While the five largest corporations in 1975 were manufacturing companies (IBM; Exxon Mobil; P&G; GE; 3M), that has completely changed in 2018 as the first five positions were occupied by Tech companies (Apple; Alphabet; Microsoft; Amazon; Facebook). Yet, organizations are only able to secure coverage to insure a relatively small portion of their intangible assets (15%) compared to insurance coverage for legacy tangible assets (59%).

This shift represents both a challenge and an opportunity for the Insurance industry. The ability to provide coverage for intangible assets would enable insurance to regain relevance and support innovation and investment. Until it can, its importance is likely to remain muted.

InsurTech

The Insurance industry has had traditionally manual processes, and has been a paper driven industry with huge inefficiencies. While customers´ needs are evolving at an unprecedented quick pace, the incumbents´ large legacy systems and naturally conservative approach, make them slow to reach the market with new products and an improved customer experience.

InsurTechs are companies that use technology to make the traditional insurance value chain more efficient. They are beginning to reshape the Insurance industry by targeting particular value pools or services in the sector, rather than seek to provide end-to-end solutions.

InsurTechs have seen more than US$ 11 billion of funding since 2015, and the volume in 2018 is expected to reach US$ 3,8 billion (FT PARTNERS). While Insurtechs were originally viewed as a disruptive force competing with traditional insurers to gain market share, there is a growing collaboration and partnership with the incumbent players. Most of them are launched to help solve legacy insurer problems across the organization, from general inefficiency in operations to enhancing underwriting, distribution, and claims functions, especially in consumer facing insurance. More recently they are also moving into the commercial segment focusing on loss prevention and efficiency. (CATLIN, T. et al. 2017). Incumbent insurers have managed to leverage InsurTechs to speed up innovation (DELOITTE, 2018: 11). From a funding perspective most of the US$ 2.6 billion that went into the InsurTechs in the first nine months of 2018 came from incumbent Insurers. (MOODY`S, 2018: 6).

The accelerated use of technology and digital capabilities again represents both a challenge for the industry but also an opportunity to innovate and develop more efficient products and services.

Data and technology with potential to transform

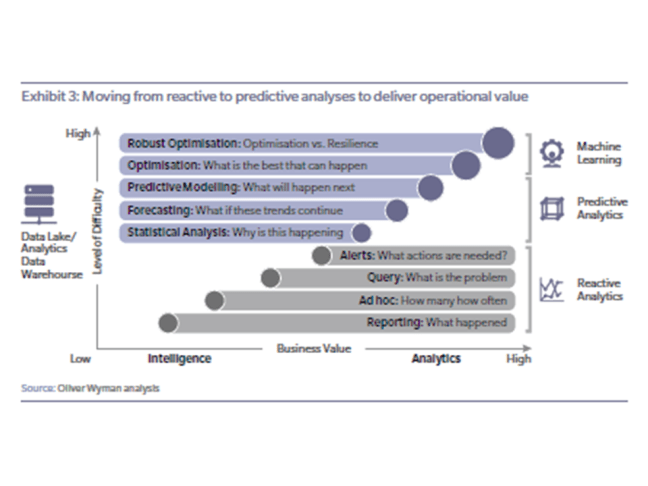

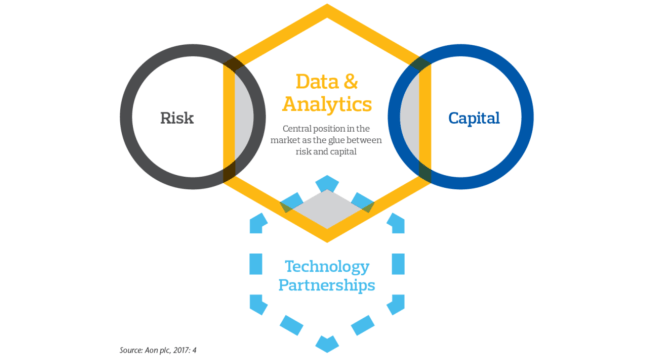

Traditionally, the Insurance industry has used proprietary historic data to match the demand from risk owners with the supply from capital providers. Focusing on relative simplistic regression analysis as the main approach.

While robust, this approach is reliant on a long data history and limits insurers ability to move into new areas. Increasingly the transformative power of data and technology is changing this relationship, as shown in the graph below. While underwriting data used to be in the hands of the incumbents only, emerging technologies, new analytical techniques and huge increases in sensors are enabling usage of new forms of data that are much more freely accessible. In addition, these technologies are supporting instant delivery of in-depth analytics that can potentially lead to significant efficiency gains and new types of products.

- Artificial Intelligence

Artificial Intelligence – Robotic Process Automation (RPA) and Cognitive Intelligence (CI) – is know as any system that can perceive the world around it, analyse and understand the information it receives, take actions based on that understanding and improve its own performance by learning from what happended.

Artificial Intelligence not only gives the opportunity to reduce costs (process automation; reduction of cycle times; free up of thousands of people hours) but improves accuracy that results in better data quality. For insurers this offers significant potential to both enable new ways of interpreting data and understanding risks. As well as reducing the costs of many critical processes such as claims assessment.

This dual impact of better understanding and lower costs is highly valuable. Insurers’ spend on cognitive/artificial intelligence technologies is expected to rise 48% globally on an annual basis over five years, reaching US$ 1.4 billion by 2021. (DELOITTE, 2017: 15).

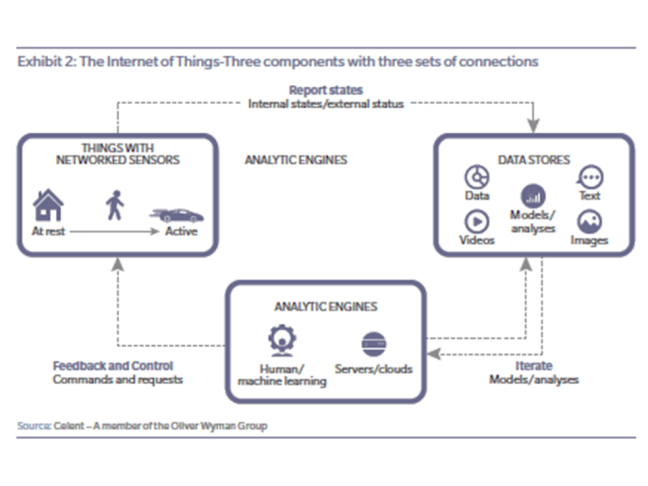

- Internet of Things

The Internet of Things refers to the digitization of objects around us. It works by embedding advanced hardware (e.g. sensors, cameras and meters) into everyday objects and even people themselves, linking those objects further to online networks. (MOODY`S, 2018: 11).

For example, connected devices in the homes such as water leakage detectors, smoke alarms, C02 readers and sophisticated home security systems will support prevention and reduction in losses from water damage, fire and burglary, respectively.

The Internet of Things has the potential to significantly change the way that risks are underwritten. The ability to have access to data in ‘real time’ will provide greater precision in the pricing of risk and also help insurers to respond better to the evolving customer needs. Consider the example of home insurance; customers will be forced to resconsider the decision to buy home insurance as packaged currently when their house is already monitored 24/7 for break-ins and the sensors are constantly monitoring the appliances to prevent fires. The insurers could utilise the same data to develop customised insurance policies depending on usage and scope of sensors.

The Internet of Things applies equally to wearable devices with embedded sensors for tracking vital statistics to improve the health, safety and productivity of individuals at work. It is predicted that the connected health market will be worth US$ 61 billion by 2026.

The Internet of Things offers the Insurance industry an opportunity to reinvent itself and to move from simply insuring against risk to helping customers protect the properties / health. This integration of insurance with products through live sensor data can revolutionise how insurance is embedded into our every day lives.

- Blockchain

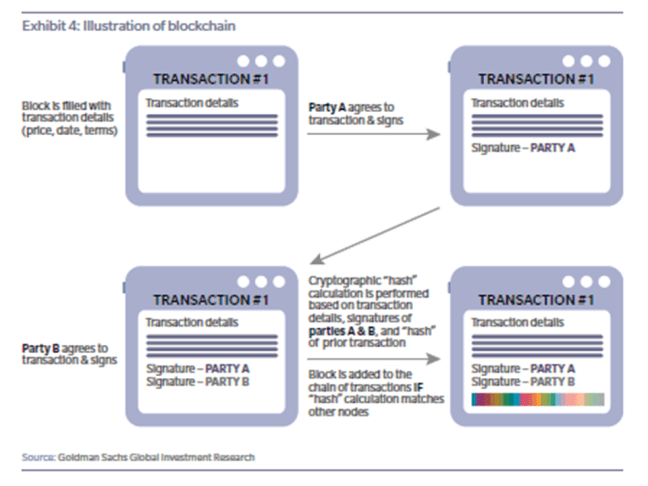

All disruptive technologies have a “tipping point” – the exact moment when it moves from early adopters to widespread acceptance. Just as it was for Google in the late 1990s and smartphones in the 2000s, could we be approaching the tipping point for the next big disruptive technology – blockchain?

Essentially, blockchain is a shared digital ledger technology that allows a continuously growing number of transactions to be recorded and verified electronically over a network of computers. It holds an immutable record of data, stored locally by each party to remove the barrier of trust. Through smart contacts, blockchain can enable automation of tasks for more efficient processing. It made its debut in 2009 as the system used to track dealing in the first cryptocurrency, Bitcoin, and, since then, organisations around the world have spotted blockchain’s potential to transform operations.

Most industries are currently experimenting with blockchain to identify and prove successful use cases to embrace the technology in business as usual. IDC, a leading market intelligence firm, expects the spend on blockchain to increase from US$ 1.8 billion in 2018 to US$ 11.7 billion in 2022 at a growth rate of 60%.

With all the aforementioned benefits, blockchain also has potential to impact the Insurance industry. It can help Insurers reduce operational and administrative costs through automated verification of policyholders, auditable registration of claims and data from third parties, underwriting of small contracts and automation of claims procedures. Equally, it can help reduce the fraud which would contribute to reduce total cost.

In an industry where ‘trust’ is critical, the ability to have guaranteed contracts, with claims certainty will help the take-up of insurance in new areas. BCG estimates that blockchain could drastically improve the end-to-end processing of a motor insurance policy and any claims arising thereof as shown in the graph below.

Conclusion

The relevance of insurance, which has declined over the last few decades, after peaking in the early 1980s, is set to increase again:

- Big shifts in insurance needs, both in the commercial and consumer segments,

- New sources of cheap capital,

- Prevelance of cheap and accessible data and the technology to automate and analyse

will transform the Insurance industry.

Not only is this important for insurers, it is also important for all of us. Insurance is the grease behind investment and innovation. The long term decline in the Insurance´s industry ability to reduce risk could be a significant impediment on future growth.

However we believe that the reversal of this trend will mean that insurance can once again grow in its importance of protecting our key investments and activities.

Click here to access Aon’s White Paper