Historically, the insurance industry has collected vast amounts of data relevant to their customers, claims, and so on. This can be unstructured data in the form of PDFs, text documents, images, and videos, or structured data that has been organized for big data analytics.

As with other industries, the existence of such a trove of data in the insurance industry led many of the larger firms to adopt big data analytics and techniques to find patterns in the data that might reveal insights that drive business value.

Any such big data applications may require several steps of data management, including collection, cleansing, consolidation, and storage. Insurance firms that have worked with some form of big data analytics in the past might have access to structured data which can be ingested by AI algorithms with little additional effort on the part of data scientists.

The insurance industry might be ripe for AI applications due to the availability of vast amounts of historical data records and the existence of large global companies with the resources to implement complex AI projects. The data being collected by these companies comes from several channels and in different formats, and AI search and discovery projects in the space require several initial steps to organize and manage data.

Radim Rehurek, who earned his PhD in Computer Science from the Masaryk University Brno and founded RARE Technologies, points out:

« A majority of the data that insurance firms collect is likely unstructured to some degree. This poses several challenges to insurance companies in terms of collecting and structuring data, which is key to the successful implementation of AI systems. »

Giacomo Domeniconi, a post-doctoral researcher at IBM Watson TJ Research Center and Adjunct Professor for the course “High-Performance Machine Learning” at New York University, mentions structuring the data as the largest challenge for businesses:

“Businesses need to structure their information and create labeled datasets, which can be used to train the AI system. Yet creating this labeled dataset might be very challenging apply AI and in most cases would involve manually labeling a part of the data using the expertise of a specialist in the domain.”

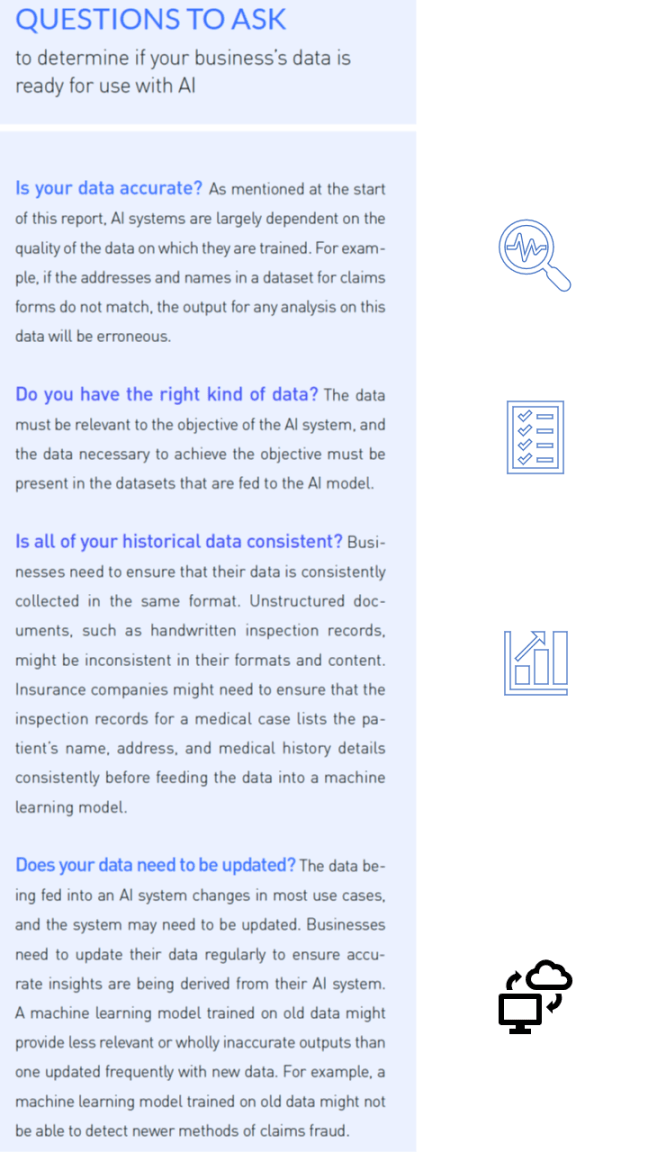

Businesses face many challenges in terms of collecting and structuring their data, which is key to the successful implementation of AI systems. An AI application is only as good as the data it consumes.

Natural language processing (NLP) and machine learning models often need to be trained on large volumes of data. Data scientists tweak these models to improve their accuracy.

This is a process that might last several months from start to finish, even in cases where the model is being taught relatively rudimentary tasks, such as identifying semantic trends in an insurance company’s internal documentation.

Most AI systems necessarily require the data to be input into an AI system in a structured format. Businesses would need to collect, clean, and organize their data to meet these requirements.

Although creating NLP and machine learning models to solve real-world business problems is by itself a challenging task, this process cannot be started without a plan for organizing and structuring enough data for these models to operate at reasonable accuracy levels.

Large insurance firms might need to think about how their data at different physical locations across the world might be affected by local data regulations or differences in data storage legacy systems at each location. Even with all the data being made accessible, businesses would find that data might still need to be scrubbed to remove any incorrect, incomplete, improperly formatted, duplicate, or outlying data. Businesses would also find that in some cases regulations might mandate the signing of data sharing agreements between the involved parties or data might need to be moved to locations where it can be analyzed. Since the data is highly voluminous, moving the data accurately can prove to be a challenge by itself.

Click here to access Iron Mountain – Emerj’s White Paper