On 10 November 2022, the European Parliament voted to adopt a new EU regulation on digital operational resilience for the financial sector (DORA). With obligations under DORA coming into effect late in 2024 or early 2025 at the latest, in this briefing we take a closer look at its impact and consider what the regulation will mean for firms, their senior managers and operations and what firms should be doing now in preparation for day one compliance.

What is DORA?

Aimed at harmonising national rules around operational resilience and cybersecurity regulation across the EU, DORA establishes uniform requirements for the security of network and information systems of companies and organisations operating in the financial sector as well as critical third parties which provide services related to information communication technologies (ICT), such as cloud platforms or data analytics services.

DORA creates a regulatory framework on digital operational resilience whereby all in-scope firms need to make sure that they can withstand, respond to, and recover from, all types of ICT-related disruptions and threats. ICT is defined broadly to include digital and data services provided through ICT systems to one or more internal or external users, on an ongoing basis.

DORA forms part of the EU’s Digital Finance Package (DFP), which aims to develop a harmonised European approach to digital finance that fosters technological development and ensures financial stability and consumer protection. The DFP also includes legislative proposals on markets in cryptoassets (MiCA), distributed ledger technology and a digital finance strategy.

Who will need to comply with DORA?

DORA will apply to financial entities, including:

credit institutions,

payment institutions,

e-money institutions,

investment firms,

cryptoasset service providers (authorised under MiCA) and issuers of asset-referenced tokens,

central securities depositories,

central counterparties,

trading venues,

trade repositories,

managers of alternative investment funds and management companies,

data reporting service providers,

insurance and reinsurance undertakings,

insurance intermediaries,

reinsurance intermediaries and ancillary insurance intermediaries,

institutions for occupational retirement pensions,

credit rating agencies,

administrators of critical benchmarks,

crowdfunding service providers and

securitisation repositories (Financial Entities).

DORA will also apply to ICT third-party service providers which the European Supervisory Authorities (the European Banking Authority (EBA), the European Securities and Markets Authority (ESMA) and the European Insurance and Occupational Pensions Authority (EIOPA), acting through their Joint Committee) (ESAs) designate as « critical » for Financial Entities (Critical ICT Third-Party Providers) through a newly established oversight framework.

The ESAs would make this designation based on a set of qualitative and quantitative criteria, including:

the systemic impact on the stability, continuity or quality of financial services in the event that the ICT third-party provider faced a large-scale operational failure to provide its services;

the systemic character or importance of Financial Entities that rely on the ICT third-party service provider;

the degree of reliance of those Financial Entities on the services provided by the ICT third-party service provider in relation to critical or important functions of those Financial Entities; and

the degree of substitutability of the ICT third-party service provider.

Any ICT third-party service provider not designated as critical would have the option to voluntarily « opt in » to the oversight. The ESAs may not make a designation in relation to certain excluded categories of ICT third–party service providers, including where Financial Entities are providing ICT services

to other Financial Entities,

to ICT third–party service providers delivering services predominantly to the entities of their own group or

to those providing ICT services solely in one Member State to financial entities that are active only in that Member State.

What are the key obligations?

DORA introduces targeted rules on ICT risk management capability, reporting and testing, in a way which enables Financial Entities to withstand, respond to and recover from ICT incidents. In principle, some of the requirements imposed by DORA, such as for ICT risk management, are already reflected to a certain extent in existing EU guidance (for example, the EBA Guidelines on ICT and security risk management).

The proposals include requirements relating to:

ICT risk management

DORA sets out key principles around internal controls and governance structures. A Financial Entity’s management body will be expected to be responsible for defining, approving, overseeing and being continuously accountable for a firm’s ICT risk management framework as part of its overall risk management framework. As part of the ICT risk management framework, Financial Entities need to maintain resilient ICT systems, revolving around specific functions in ICT risk management such as

identification of risks,

protection and prevention,

detection,

response and recovery and

stakeholder communication.

Reporting of ICT-related incidents

DORA aims to create a consistent incident reporting mechanism, including a management process to detect, manage and notify ICT-related incidents. Incidents deemed « major » would need to be reported to competent authorities within strict time frames, including initial notifications « without delay » on the same day or next day by using mandatory reporting templates. In some cases, communication to service users or customers may be required.

Testing

As part of the ICT risk management framework, DORA requires Financial Entities to adopt a robust and comprehensive digital operational resilience testing programme covering ICT tools, systems and processes. Certain Financial Entities must carry out advanced testing of their ICT tools, systems and processes at least every three years using threat-led penetration tests.

Information sharing

DORA contains provisions which should facilitate the sharing, among Financial Entities, of cyber threat information and intelligence, including

indicators of compromise,

tactics,

techniques and procedures,

cyber security alerts and

configuration tools

to strengthen digital operational resilience.

Localisation

Financial Entities will only be permitted to make use of the services of a third-country Critical ICT Third-Party Provider if such provider establishes a subsidiary in the EU within 12 months following its designation as a Critical ICT Third-Party Provider.

A simplified set of ICT risk framework requirements will apply to certain Financial Entities, including small and non-interconnected investment firms and payment institutions exempted under the Second Payment Services Directive. Such entities will need to comply with a reduced set of requirements under DORA, including the requirement to put in place and maintain a sound and documented risk management framework that details the mechanisms and measures aimed at a quick, efficient and comprehensive management of all ICT risks, including for the protection of relevant physical components and infrastructures.

What should firms be doing now to prepare?

Although it is not expected that DORA will apply to in-scope entities until late 2024 (see below), firms should now begin considering the steps that they will need to take to ensure day one compliance. These include:

Scope out impact

Taking a risk-based approach reflective of their size, nature, scale and the complexity of their services and operations, Financial Entities should begin to scope out the impact of DORA on their business. Firms should carry out a comprehensive gap analysis of their existing ICT-risk management processes against the new requirements introduced by DORA to identify any aspects of their existing processes that will be impacted by the new requirements and develop detailed implementation plans setting out the steps that will need to be taken to effect relevant changes. As part of this, Financial Entities should ensure that they have in place appropriate:

(i) capabilities to enable a strong and effective ICT risk management environment;

(ii) mechanisms and policies for handling all ICT-related incidents and reporting major incidents; and

(iii) policies for the testing of ICT systems, controls and processes and the management of ICT third-party risk.

This process will be iterative as some of the more detailed requirements of DORA will be further developed through technical standards to be published by the ESAs in due course.

Critical ICT Third-Party Providers

Critical ICT Third-Party Providers will be required to have in place comprehensive, sound and effective rules, procedures, mechanisms and arrangements to manage the ICT risks which they may pose to Financial Entities. Although DORA provides that the designation mechanism (pursuant to which the ESAs may designate an ICT third-party service provider as « critical ») must not be used until the Commission has adopted a delegated act specifying further details on the criteria to be used in making such an assessment (to be adopted within 18 months after the date on which DORA enters into force), it is expected that certain categories of providers, such as cloud computing service providers who provide ICT services to Financial Entities, will be designated as Critical Third-Party Providers.

Consequently, such providers may wish to begin the task of benchmarking their existing systems, controls and processes against existing guidelines, such as the EBA Guidelines on ICT and security risk management and Guidelines on outsourcing arrangements, to the extent required, to identify areas that require further investment and maturity. They will also need to consider whether new and existing contracts give them sufficient flexibility to comply with new regulatory rules, orders and directions, even if this would otherwise be inconsistent with their contractual obligations. As set out above, certain categories of ICT third-party service providers are expressly excluded from the designation mechanism, including Financial Entities providing ICT services to other Financial Entities, ICT intra-group service providers and ICT third-party service providers providing ICT services solely in one Member State to Financial Entities that are only active in that Member State.

Third Country Critical ICT – Third-Party Providers – Subsidiarisation

The EU subsidiarisation requirement that will apply to third country Critical ICT Third-Party Providers is one that will necessitate early engagement between such providers and the Financial Entities that they serve. While it is not clear what role the EU subsidiary must play in the provision of services to the relevant Financial Entity (e.g. whether the provider must act as contractual counterparty), Recital 58 of DORA indicates that the requirement to set up a subsidiary in the EU does not prevent ICT services and related technical support from being provided from facilities and infrastructures located outside the EU. Nevertheless, where a relevant third country ICT third-party provider that is likely to be designated as « critical » indicates that it does not intend to establish a subsidiary in the EU, even following a designation as such by the ESAs, Financial Entities may wish to commence the process of identifying alternative providers, since they will not be permitted to obtain ICT services from a third country Critical ICT Third-Party Provider that fails to establish a subsidiary in the EU within 12 months following its designation as critical.

Companies that consider they are likely to be classified as Critical ICT Third-Party Providers that do not already have an establishment or subsidiary located in the EU should begin to consider now which Member State would be most appropriate to establish a new subsidiary in, taking into account their business operations and the various applicable legal requirements.

Documentation impact

As noted above, DORA sets out core contractual rights in relation to several elements in the performance and termination of contracts with a view to enshrine certain minimum safeguards underpinning the ability of Financial Entities to monitor effectively all risk emerging at ICT third-party level. Some contractual requirements set out in DORA are mandatory and will need to be included in contracts, if not already reflected. Others take the form of principles and recommendations and may require negotiation between the relevant parties. Early mapping and engagement in this respect will be important. Additionally, parties may wish to consider benchmarking their existing contractual arrangements against relevant requirements set out in DORA, as well as existing standard contractual clauses developed by EU institutions.

For example, Recital 55 of DORA notes that « the voluntary use of contractual clauses developed by the Commission for cloud computing services may provide comfort for Financial Entities and ICT third-party providers by enhancing the level of legal certainty on the use of cloud computing services in full alignment with requirements and expectations set out by the financial services regulation ».

As the industry awaits more detailed technical standards to be developed and published by the relevant ESAs, as well as DORA compromise/Level 1 text, in-scope entities may consider using existing guidelines such as the EBA Guidelines on ICT and security risk management and Guidelines on outsourcing arrangements as useful benchmarking tools in preparation for day one compliance.

How does DORA interact with NIS2?

The second iteration of the Security of Network and Information Systems Directive (NIS2) aims to strengthen security requirements and provide further harmonisation of Member States’ cybersecurity laws, replacing the original NIS Directive of 2016 (NIS1). Its timeline is similar to that for DORA, with a provisional agreement among EU institutions reached in May 2022, and its adoption confirmed in a European Parliament plenary session vote on 10 November 2022. NIS2 significantly extends the scope of NIS1 by adding new sectors, including « digital providers » such as social media platforms and online marketplaces, for example, but importantly also introduces uniform size criteria for assessing whether certain financial institutions (and other entities) fall within its scope. NIS2 sets out cybersecurity risk management and reporting obligations for relevant organisations, as well as obligations on cybersecurity information sharing, so there is some overlap in coverage with DORA.

However, this has been addressed during the legislative process to ensure that financial entities will have full clarity on the different rules on digital operational resilience that they need to comply with when operating within the EU. NIS2 specifically provides that any overlap will be addressed by DORA being considered as lex specialis (ie a more specific law that will override the more general NIS2 provisions).

How does DORA compare with international developments?

The introduction of DORA in the EU reflects a global focus on operational resilience and strengthening cybersecurity standards in the wake of ever-increasing digitalisation of financial services and increasingly sophisticated cyber incidents. For example, in March 2021, the Basel Committee on Banking Supervision issued its Principles for operational resilience, as well as an updated set of Principles for the sound management of operational risk (PSMOR), which aim to make banks better able to withstand, adapt to and recover from severe adverse events.

In October 2022, following a G20 request, the Financial Stability Board (FSB) published a consultation on Achieving Greater Convergence in Cyber Incident Reporting, recognising that timely and accurate information on cyber incidents is crucial for effective incident response and recovery and promoting financial stability and with a view to ensuring that financial institutions operating across borders are not subject to multiple conflicting regimes. The FSB proposals include recommendations to address the challenges to achieving greater international convergence in cyber incident reporting, work on establishing common terminologies related to cyber incidents and a proposal to develop a common format for incident reporting exchange.

Following its departure from the EU, the UK has introduced a Financial Services and Markets Bill (the UK Bill) which includes proposals to regulate cloud service providers and other critical third parties supplying services to UK regulated firms and financial market infrastructures. HM Treasury would have powers to designate service suppliers as ‘critical’ and the UK regulators would have new powers to directly oversee designated suppliers, which would be subject to new minimum resilience standards. While the proposals have the same ambitions as, and there are similarities with, the requirements under DORA, there are a number of key differences between them.

For example, the proposed enforcement regime under DORA for Critical ICT Third-Party Providers is very different from the equivalent regime proposed by the UK Bill. Under DORA, the ESAs will be designated as « Lead Overseers », but with the power only to make ‘recommendations’ to Critical ICT Third-Party Providers, in contrast to the ability for UK regulators to make rules applying to, or to give directions to, critical third parties subject to the UK Bill, with the ability to issue sanctions for non-compliance. Under DORA, non-compliance by a Critical ICT Third-Party Provider with recommendations gives the Lead Overseer the ability to notify and publicise such non-compliance and « as a last resort » the option to require Financial Entities to temporarily suspend services provided by such provider until the relevant risks identified in the recommendations have been addressed.

This means that the liability and contractual issues for Critical ICT Third-Party Providers providing services in the EU will be different than for those providing services in the UK, and that contracts for each will need to be considered and negotiated carefully.

Next steps and legislative timeline

Following adoption of DORA by the European Parliament plenary session on 10 November 2022, the regulation is now passing through the final technical stages of the formal procedure for European legislation. The text still needs to be formally approved by the Council of the EU before being published in the Official Journal, which is expected in December 2022 or January 2023.

DORA will come into effect on the twentieth day following the day on which it is published in the Official Journal. It will apply, with direct effect, 24 months from the date on which it enters into force. Therefore, it is expected that DORA will apply to in-scope firms from late 2024 or early 2025 at the latest.

EXECUTIVE SUMMARY AND POLICY ACTIONS The recovery associated with the receding pandemic has slowed as a result of the Russian aggression in Ukraine. It has contributed to high inflation and is damaging the economic outlook, which led to increased financial market risks across the board. The economic and financial impact of the invasion has been felt globally, alongside enormous humanitarian consequences. Prices in energy and commodity markets have risen to record highs. Production and logistics costs have risen and household purchasing power has weakened. After a long period characterized by very low inflation and interest rates, policy rates are being raised in response to high inflation. The resulting higher financing costs and lower economic growth may put pressure on the government, and on corporate and household debt refinancing. It will likely also have negative impact on the credit quality of financial institution loan portfolios. Financial institutions are moreover faced with increased operational challenges associated with heightened cyber risks and the implementation of sanctions against Russia. The financial system has to date been resilient despite the increasing political and economic uncertainty.

In light of the above risks and uncertainties, the Joint Committee advises national competent authorities, financial institutions and market participants to take the following policy actions:

Financial institutions and supervisors should continue to be prepared for a deterioration in asset quality in the financial sector. In light of persistent risks that have been amplified by the Russian invasion and a deteriorating macroeconomic outlook, combined with a build-up of medium-term risks with high uncertainty, supervisors should continue to closely monitor asset quality, including in real estate lending, in assets that have benefitted from previous support measures related to the pandemic, and in assets that are particularly vulnerable to rising inflation and to high energy- and commodity prices.

The impact on financial institutions and market participants more broadly from further increases in policy rates and the potential for sudden increases in risk premia should be closely monitored. Inflationary pressures coupled with uncertainty on risk premia adjustment raise concerns over potential further market adjustments. Rising interest rates and yields are expected to improve the earnings outlook for banks given their interest rate sensitivity. They could also reduce the valuation of fixed income assets, and result in higher funding costs and operating costs, which might affect highly indebted borrowers’ abilities to service their loans. Credit risks related to the corporate and banking sector also remain a primary concern for insurers and for the credit quality of bond funds. High market volatility stemming from the above economic and geopolitical situation could also raise short-term concerns and disruptions for market infrastructures.

Financial institutions and supervisors should be aware and closely monitor the impact of inflation risks. The economic consequences of the Russian aggression mainly channel through energy and commodity markets, trade restrictions due to sanctions and the possible fragmentation of the global economy. Financial fragmentation, including fragmentation of funding costs, could threaten financial stability and put pressure on price stability. Inflation is not only relevant from a risk perspective, but is expected to reflect also on the actual benefits and pensions, inflationary trends should be taken into account in the product testing, product monitoring and product review phases. Financial institutions and regulators should make extra efforts to ensure investor awareness on the effects of inflation on real returns of assets, and how these can vary across different types of assets.

Supervisors should continue to monitor risks to retail investors some of whom buy assets, in particular crypto-assets and related products, without fully realizing the high risks involved. Some retail investors may not be fully aware of the long-term effects of rising inflation on their assets and purchasing power. In the context of growing retail participation and significant volatility in crypto-assets and related products, retail investors should be aware of the risks stemming from these. The recent events and subsequent sell-off of crypto assets raises concerns on the appropriate assessment of the risks and the developments of this market segment going forward and requires particular attention of financial institutions and supervisors. Where disclosures are ineffective, these risks are compounded.

Financial institutions and supervisors should continue to carefully manage environmental related risks and cyber risks. They should ensure that appropriate technologies and adequate control frameworks are in place to address threats to information security and business continuity, including risks stemming from increasingly sophisticated cyber-attacks.

1 MARKET DEVELOPMENTS The Russian invasion and inflationary pressures have significantly impacted the risk environment of EU securities markets. Recoveries in most equity indices from the beginning of 2022 came to a halt, following the March 2020 market stress, with global equity indices broadly declining (in 1H22: Europe -18%, China -8%, US -20%). This was mostly linked to energy costs and lower trade flows due to the Russian invasion, supply-side bottlenecks linked to the continued effects of the COVID-19 pandemic and the tightening of credit conditions for firms. At the same time, volatility as measured by the European volatility index VSTOXX rose in early March (41%) to about half the levels of March 2020. In Europe, more energy intensive sectors, such as consumer discretionary (-31% YTD), industrials (-29%), and technology (-36%), saw larger price falls than other sectors. Price-earnings ratios tumbled, though they remained above 10-year historical averages (at 3% EU and 9% US respectively). The decreases partly reflect lower earnings expectations for the future, due to the potential long term effects of the pandemic and the impacts of higher long-term interest rates.

Fixed income markets were characterized by investor expectations of slower economic growth, higher inflation and a less accommodating interest rate environment. Despite a short-lived fall right after the invasion, EU sovereign bond yields rose in 1H22 to levels unseen since 2016 with significant news-flow related volatility (IT +213bps, GR +230bps, DE +150bps). As of end-June, spreads to the Bund also widened, e.g. for Italy (1.9%, +70bps) and Spain (1.1%, +39bps). Corporate bond markets showed sensitivity to the evolving outlook, recording significant selloffs across all rating categories and reduced liquidity. Investment grade (IG) bonds experienced a peak-to-trough fall of 15% (August 2021 to May 2022), nearly twice that of the pandemic, and declined by 12% in the year to June. High-yield (HY) bonds performed slightly worse (‑15%) but their peak-tot rough losses were lower than during the pandemic. Credit spreads widened on concerns that the slowdown could weigh on firms’ debt capacity. Significant spreads upswings were also seen in February with the invasion, and in May and June as rates hikes occurred in the US and were announced for the EA.

The crypto-asset market experienced a continued sell-off in 2Q22 in line with the decline of traditional financial assets (especially tech equities) with which Bitcoin (BTC) shares a close (40%) correlation. The collapse of crypto-asset TerraUSD in May and the pausing of customer withdrawals by crypto-asset Celsius in June, added to the shift in investor sentiment away from these assets, sending BTC price to an 18-month low. In May, the largest algorithmic stablecoin (third largest overall), TerraUSD, failed to maintain its peg to the USD after its underlying decentralised finance (DeFi) protocol, Anchor, suffered a confidence run on its deposits. The combination of the sharp fall in crypto-asset prices, and the demise of the Anchor protocol linked to TerraUSD, caused the total value of assets ‘locked’ (deposited) in DeFi smart contracts to fall from over EUR 186bn at the start of May to EUR 62bn by June. In another development in June, centralized finance (CeFi) lending platform, Celsius, halted customer withdrawals of deposits, signaling that it had liquidity issues or a deeper insolvency problem. This coincided with a 21% fall in the Bitcoin price and led Binance to temporarily suspend Bitcoin withdrawals from its exchange. The Celsius token price had fallen by 94% since the start of 2022 with market speculation that it could sell a sizeable stake in crypto asset Ethereum to avoid collapse.

The turmoil triggered by the Russian invasion also affected environmental, social and governance (ESG) markets. In 1Q22, EU ESG equity funds had net outflows of EUR 5bn, compared with average inflows of EUR 11bn per quarter in 2021. ESG bond issuance volumes fell 29% from the start of the year to June, as compared with the same period in 2021. In the banking sector, ESG bond issuance as a share of total bond issuance decreased compared to 2021, though they often enjoy higher subscription levels than non-ESG bonds, allowing banks to pay lower risk premia on new issuances. Despite this, some fundamental factors driving the rise of ESG investing remain in place. Most importantly, investor preferences continue to shift towards sustainable investments, with portfolio allocations increasingly tilted towards ESG investments. Similarly, issuance of ESG bonds by EU corporates remained on par with early 2021, supported by a rapid expansion of the sustainability-linked bond market. This contrasts with a 32% fall in broader EU corporate bond issuance.

2 DEVELOPMENTS IN THE FINANCIAL SECTOR In 1H22, European investment funds faced heightened volatility in securities markets given the increasingly uncertain economic outlook and the expected increase in interest rates. The performance of most EU fund categories dropped significantly, from a 12-month average monthly performance of 1.6% for equity funds in December 2021 to 0.9% in June 2022. In the meantime, the performance of bond funds turned negative (-0.7%). In contrast, commodity funds outperformed the sector in 1Q22, reflecting the surge in commodity prices following the Russia’s invasion of Ukraine and the sanctions on Russia, before slightly receding, to 2.1%, in end-June. Equity fund flows were also negative (-0.9%). Declining performance led to redemption requests with net outflows in 1H22 totalling 1.6% of the net asset value (NAV) of the fund sector. Bond funds were particularly affected (-4.8% NAV) due to negative performance (-0.7%) and exposures to growing credit and interest risks. Commodity funds experienced outflows (-5.8%), albeit from a low base and only in 2Q22, when their performance declined. MMFs funds also experienced substantial outflows ( -9.2% NAV exceeding the -4.6% NAV observed during COVID-19 stress). MMFs denominated in all currencies experienced outflows, though USD MMFs experienced higher returns (1.1% average monthly performance) than EUR denominated MMFs (-0.1%). While MMFs may generally benefit from a flight-to-quality during uncertain market conditions, investors currently appear to be turning away from fixed-income funds in general. Outflows were partly driven by the expected increase in interest rates. In contrast, real estate funds (1.7% of NAV) and mixed funds (1% of NAV) recorded inflows in 1H22.

The European insurance sector entered 2022 in good shape notwithstanding the adverse developments since the COVID-19 outbreak. During 2021, gross written premiums (GWP) for the life business grew (y-o-y) quite substantially (+14%), while growth was lower for the non-life business (8%). The positive change has partially been driven by the previous reduction in GWP throughout 2020 during the pandemic; although GWP remain still below pre-Covid levels, in particular for life business. The good performance of financial markets and the high returns obtained during 2021 pushed insurer’s profitability up to the levels reached back in 2019, with a median return on assets standing at 0.57% in 4Q21 (0.38% in 4Q20).

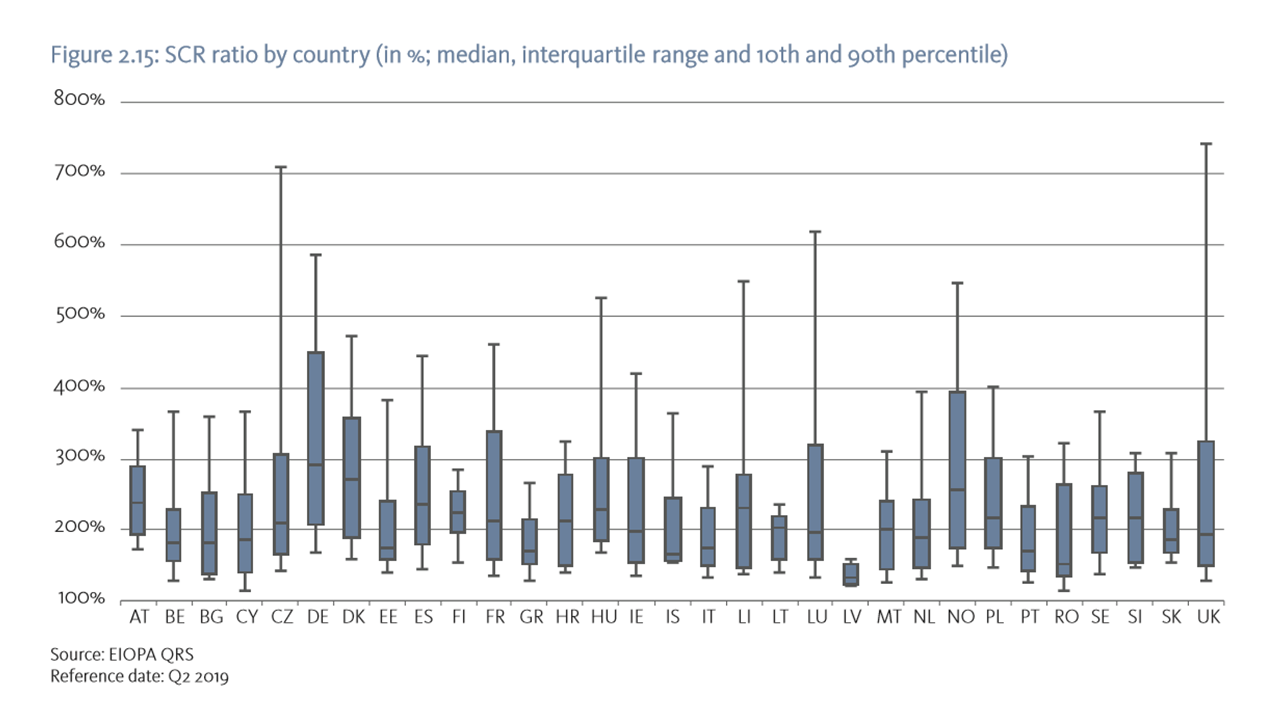

At the beginning of 2022 insurers’ capital buffers on aggregate were solid with a median SCR ratio of 216%. An improvement was observed for life insurers while a slight decline was observed for non-life insurers. As the risk-free interest rate increased throughout 2021, due to the long maturities of life insurers’ liabilities the value of technical provision decreased relatively more than the value of assets, with a positive effect on net capital. This contributed to an increase the median SCR ratio for life insurers, from 216% to 225%. However, the SCR ratio did not reach the high levels observed at the end of 2019 (236%). On the other hand, the median SCR ratio for non-life insurers slightly decreased from 218% towards 211%. This might be driven by the increase in claims negatively affecting the liabilities of some representative undertakings, combined with the fact that asset values declined more than liabilities when interest rates increased given that non-life insurers tend to be characterized by a positive duration gap. Likewise, the financial position of EEA IORPs displayed a recovery in 2021. The total amount of assets grew to EUR 2,713 bn in 4Q21 (From EUR 2,491 bn. in 4Q20), while liabilities remained more or less unchanged. Similarly, the Excess of Assets over Liabilities exhibited a positive trend.

The European banking sector entered 2022 with relatively strong capital- and liquidity positions. The capital ratio (CET1 fully loaded) is, at 15.0% in 1Q22, at the same level as it was before the pandemic broke out (in 4Q19). Yet the capital ratio was 50bps lower than in the previous quarter, mainly driven by rising risk weighted assets (RWA). After a steadily rise in previous quarters, the liquidity coverage ratio (LCR) also slightly deteriorated in 1Q22. A reported LCR ratio of 168.1% in 1Q22 (174.8% in 4Q21) was nevertheless still substantial.

EU banks are facing additional challenges to asset quality and profitability while pandemic-related vulnerabilities continue to loom. Deteriorating economic prospects, high uncertainties and high inflation with a phasing-out of accommodative monetary policy are affecting the outlook for EU banking sector. Loan portfolios with pre-existing vulnerabilities from disruptions caused by the pandemic may also be further affected in a slower economic recovery. Accordingly, 45% banks responding to the EBA’s spring 2022 risk assessment questionnaire (RAQ) indicated their plans to maintain their overlays related to the pandemic to cover potential losses that may materialize in the next quarters, while 35% of banks indicated plan to release them fully or partially. Supervisors should continue to closely monitor the adequacy of banks’ provisions.

The NPL ratio further improved in the first quarter of the year (to 1.9%), mainly driven by decreasing volumes of non-performing loans (NPL). However, rising cost of risks and an increasing share of loans allocated under Stage 2 under IFRS points to slightly deteriorating asset quality. The quality of loans under previous support measures related to the pandemic continues to show signs of deterioration and also requires vigilance. The total volume of loans with expired EBA-compliant moratoria reached EUR 649bn in 1Q22, a 7.8% decline compared to the previous quarter. The volume of subject to public guarantee schemes (PGS) stood at EUR 366bn in 1Q22, almost unchanged compared to the previous quarter. The NPL ratio of loans under expired moratoria and of loans subject to PGS is, at 6.1% and 3.5% in 1Q22, respectively, substantially higher than the overall NPL ratio, and has increased further since 4Q21. PGS loans are mostly concentrated to a few countries only. The allocation of Stage 2 under IRFS 9 for loans under previous support measures is, at 24.5% for loans under expired moratoria and 22.7% for loans subject to PGS, substantially higher than stage 2 allocations for all loans and advances (9.1% in 1Q22). In spite of their slight deterioration in 1Q22, EU banks’ capital and liquidity positions nevertheless provide, for the time being, sufficient cushioning in banks’ balance sheets should the economic situation deteriorate further, or heightened market volatility persist.

Positive operating trends were observed for European banks in 1Q 2022, with a profitability of 6.6% return on equity (ROE) achieved under difficult market conditions, though this is lower than the 7.7% ROE reported in the previous year (1Q21) and lower than the 7.3% ROE of the previous quarter. The contraction can be explained mainly by rising contributions to deposit guarantees schemes and resolutions funds in some countries and various one-off effects, whereas net operating income improved. In 1Q21, lending growth offset a slight decline in net interest margins (NIM) and led to improved net interest income (NII). Net trading income also increased, supported by market volatility. Overall increasing net operating income also outweighed the impact of rising inflation on operating expenses in the first quarter of 2021.

3 IMPACT OF RU-UA WAR ON THE EUROPEAN FINANCIAL SECTORS Securities markets experienced volatility with some key commodity markets strongly impacted by the Russian invasion and sanctions. Bond yields rose in response to the increasing inflation and anticipated higher rates, while equity markets were volatile and experienced periodic sell-offs. Such volatility can create short-term risks on financial markets. Margin calls on derivatives related to commodities can create liquidity strains for counterparties, as was witnessed by the calls for emergency liquidity assistance for energy traders and the London Metal Exchange suspending nickel trading for five trading days in early March. While commodity derivatives markets in the EU are of limited size relative to EU derivative markets as a whole, these markets create sensitive interlinkages between commodity producing or processing companies, commodity traders, banks acting as intermediaries in the clearing process, central counterparties, and other financial institutions.

The Russian invasion negatively affected credit rating agencies’ (CRA) credit outlook for EEA30 debt. The number of corporate downgrades grew relative to upgrades over 1H22, with a jump in downgrades around the time of the invasion. Russian and Ukrainian ratings were mainly affected, with a series of downgrades in late February and March among both corporates and sovereigns. By mid-April CRAs had withdrawn their Russian ratings in response to the EU measures banning the rating of Russian debt and the provision of rating services to Russian clients. In addition, sanctions have made it difficult for Russia to make sovereign coupon payments. In this context, Russia defaulted on some debt payments due in late June.

Direct impacts of the invasion on investment funds were limited. Exposures to both Russian and Ukrainian counterparties were EUR 50bn (below 0.5% of EU fund assets as of end-January 2022). Some fund exposures were higher, with 300 funds holding over 5% of their portfolios in Russian and Ukrainian assets (total EUR 225bn). The massive fall in prices and liquidity of Russian financial instruments led to serious valuation issues for exposed EU funds. In 1H22, 100 Russia-exposed EU funds (EUR 15bn in combined assets) temporarily suspended redemptions. However, funds with material Russian exposures before the invasion account for a very small share of the EU fund population (less than 0.1% of the EU industry). A number of ETFs tracking Russian benchmarks also suspended share creation. While direct impacts of the Russian invasion on funds, such as losses, were limited, existing risks were amplified by the invasion and the deteriorating macroeconomic outlook. Credit, valuation and liquidity risks remained elevated in the bond fund sector, linked to multiple factors. Bond fund exposures to credit risk stayed elevated, especially for HY funds. The credit quality of the portfolio of HY funds remained close to an average rating between BB- and B+ (5-year low). The likelihood of credit risk materialization also increased with the deteriorating macroeconomic environment and rising interest rates, as visible in the higher credit spreads. In comparison, liquidity risk remained steady for corporate bond funds. Based on asset quality and cash holdings, portfolio liquidity remained stable in 1H22.

EU insurers’ exposure to assets issued in Russia, Ukraine and Belarus is also limited. These assets amount to EUR 8.3 bn, less than 0.1% of the total investment of the sector. The exposure to Russia is EUR 6.3 bn, which is 0.066% of total investments and the asset exposure to Ukraine is EUR 1.8 bn, 0.019% of total Investments. The exposure to Belarus is negligible. Most of the investments in Russia are through investment funds (84% of total investments). Within funds, the largest asset classes are represented by sovereign bonds and equities associated to unit linked portfolios. A large share of investments to Russia, Ukraine and Belarus (42%) is in index- and unit-linked portfolios, whose risk is born directly by policyholders.

EU insurers have limited activities in the Russian, Ukrainian and Belarusian markets. A small number of EEA groups are active in those countries through subsidiaries. Their size in terms of total assets is minimal if compared to the total assets of the groups. In terms of liability portfolios exposures are also limited. Total technical provision in Russia, Ukraine and Belarus is EUR 0.36 bn., mostly concentrated in the life business.

With regards to IORPs, asset exposures are also limited, at EUR 7.5 bn. (0.23% of total investments). In absolute numbers this is similar to the exposure of the insurance sector. It is worth noting that the size of the IORPs total investment is smaller with respect to the insurance sector.

In the banking sector, direct exposure to Russia and Ukraine appears limited on an EU level and country level. In 1Q22, exposures of the EU/EEA banking sector were at EUR 75.3bn (ca. 0.3% of total assets) towards Russian counterparties, at EUR 10.0bn towards Ukrainian counterparties, and at EUR 2.0bn towards Belorussian counterparties, slightly decreasing towards the three countries compared to the previous quarter. However, exposures are concentrated in a few countries, and a few banks report an up to 10% share of their exposures towards Russia and Ukraine. Some banks also booked substantive provisions related to their exposure to Russia and related to the deteriorating economic environment in the first quarter of this year.

While immediate, first round implications from the Russian invasion appear contained for financial institutions across sectors, the possibility of second round effects is a source of concern. The invasion, heightened uncertainties and inflation are not only weighing on economic prospects, but also affect consumer- and business confidence. Exposures of economic sectors more sensitive to rising energy- and commodity prices require attention across sectors.

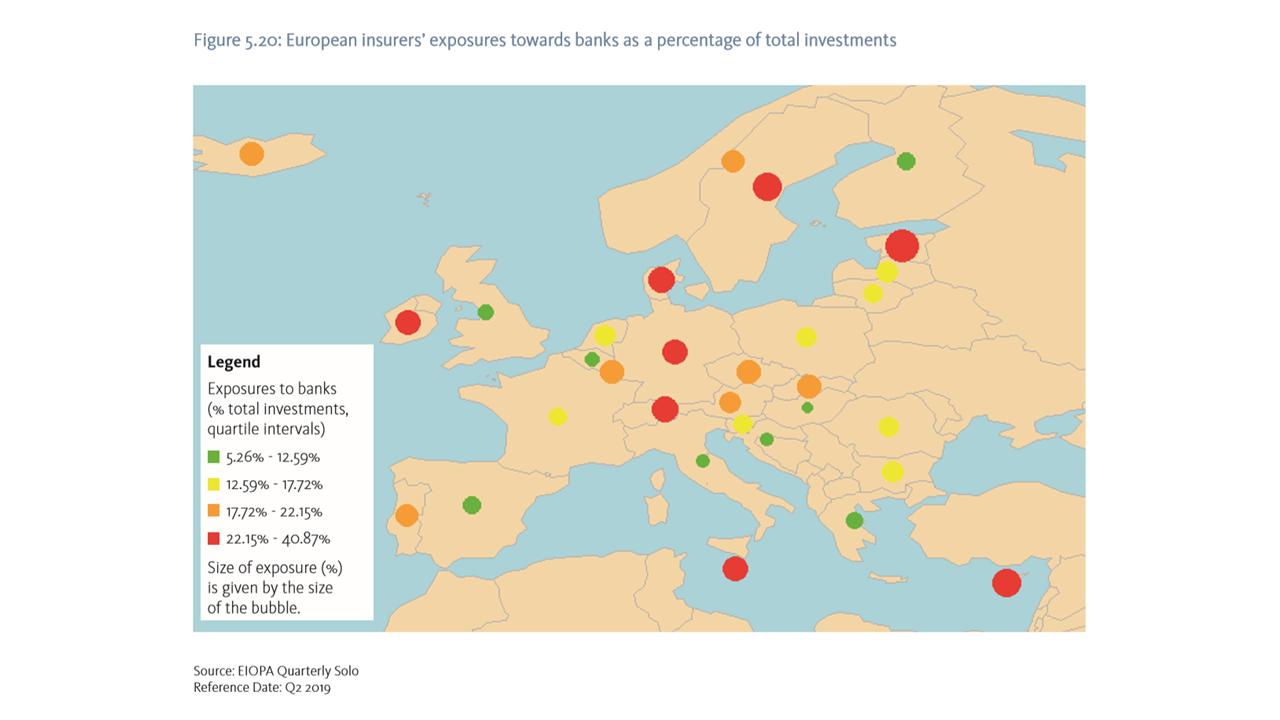

In the insurance sector, second-round effects could emerge via exposures to sectors which, in turn, are highly exposed to the current crisis. Losses in these sectors could have spill-over effects through losses on investments. Two areas could be the most relevant: the exposures of insurers to the banking sector and the exposure to sectors of the economy that are more sensitive to energy and gas prices. Insurers have significant holdings of bank assets, and in this context also hold a significant amount of assets issued by banks that are assumed to be more vulnerable to the evolution of the current crisis. The exposure of EEA insurers to those banks is estimated to only a total amount of EUR 55 bn (0.57% to total investments). Furthermore, insurers have significant asset exposure to sectors sensitive to energy and gas prices.6 The total exposures sum to EUR 174 bn, which includes almost 3% of the equity portfolio of insurers and 7.5% of corporate bond holdings.

In the banking sector, second-round effects could emerge via deteriorating asset quality and further increasing provisioning needs in a deteriorating economic environment. Fee and commission income might also be affected. Banks’ securities portfolios might moreover be negatively affected as fair value declines when interest rates rise. The worsening economic outlook has already resulted in slightly deteriorating early warning indicators for asset quality. The cost of risk increased to 0.51% in 1Q22, a 4bps increase compared to the previous quarter, as borrowers’ debt servicing capacity might be affected by lower economic growth. The increase was mainly driven by the numerator, i.e. by increasing allowances for credit losses. Also, the share of loans allocated under Stage 2 under IFRS increased in 1Q22 and 4Q21, and it another early-warning indicator pointing to slightly deteriorating asset quality. Responses to the EBA RAQ moreover indicate that a majority of banks expect asset quality to deteriorate.

In line with the deteriorating economic outlook and heightened market- and interest rate volatility, bank funding conditions have worsened since the Ukrainian war started and since interest rates increased. Wholesale bank debt spreads have widened for debt and capital instruments across the capital ladder, and particularly for subordinated instruments. Interest rates for bank debt instruments have risen substantially across durations, albeit from extremely low levels. Since the beginning of the war, bank debt issuance activity has been mainly focused on issuing covered bonds, amid challenging market conditions and as banks have begun to roll over expiring long-term central bank funding facilities. Bank funding conditions are likely to stay more challenging while volatility persists and as interest rates continue to rise. Yet current ample liquidity buffers should allow banks to withstand further periods of market turmoil for the time being. In the medium-term, the substitution of expiring extraordinary central bank funding with other sources of funding could prove challenging for some banks.

In spite of positive operating trends in 1Q2022, the outlook for EU bank profitability is subdued. The deteriorating economic environment might affect lending growth and might result in lower loan- and payment-related fee income. Inflationary pressure, higher provisioning needs for expected deteriorating asset quality, costs related to digital transformation and higher compliance costs, e.g. related to the enforcement of sanctions will all likely affect costs, and may offset operating cost savings achieved. While rising rates may have a positive impact on interest income, rising funding costs might also offset additional income from asset repricing.

4 INFLATION AND INTEREST RATE RISKS The Russian aggression and the sanctions applied contributed to inflation pressures via the resulting supply shocks in energy, food and metals commodities, which added to the supply chain bottlenecks related to the pandemic. Higher energy prices particularly contribute to inflation, widely increasing input and distribution costs. In terms of investment impacts, inflation directly lowers real returns. Inflation changes relative attractiveness of assets both across asset classes and within asset classes. Higher inflation reduces the values of existing assets with fixed returns, such as (most) bonds. By reducing short-term growth, higher rates lower profitability and typically reduce equity values. However, if a rate rise is expected to be effective in increasing long-term growth, it can also increase equity values. Inflation has indirect impacts through its effects on actual and anticipated monetary policy, especially interest rate rises, to reduce demand and bring inflation down. Higher interest rates increase returns on savings and raise borrowing and refinancing costs, reducing debt sustainability. Variable-rate loans face higher debt servicing costs, raising credit risk, including for securitizations backed by variable-rate loans.

In the investment fund sector, interest rate risk increased in a context of rising inflation expectations. Fund portfolios with a longer duration will see their value fall, as inflation drives rates up. However, adjustments are already being made in some funds. Bond fund portfolio durations fell in 1H22, remaining higher for Government (7.6 years, down from 8.6 years) and IG bond funds (6.5 years, down from 7.3 years) than for HY funds (4.3 years, down from 4.8 years). Based on current duration, a 100bps increase of in yield could have a potential impact of -7% on bond fund NAV, about EUR 270bn, which could lead to significant fund outflows. In the MMF sector, funds also significantly reduced the weighted average maturity of their portfolios from 44 days to 30 days (a 3-year low) to lower interest rate risk and improve resilience to a rate rise.

As a period of low inflation and low interest rate is coming to an abrupt end, medium-term risks for asset managers are considerable. Impacts on performance and fund flows are likely to vary across asset classes. For example, the recent US increase in rates led to significant reallocation across fund types from bond funds (-4.7% NAV in 1H22) towards funds offering some form of protection against higher rates. To-date, this contrasts with the EU. In 1H22, US cumulative flows into funds offering protection against higher inflation or rates, such as inflation-protected funds (EUR 1.5bn), loan funds (EUR 13.9bn) and commodity funds (EUR 16.3bn), outpaced their EU equivalents.

Inflation can have a significant impact on borrowers and retail investors. It can heighten vulnerabilities of debtors exposed to flexible lending rates, or where low interest rates on their loans will expire in the near term, including in mortgage lending. Inflation can also have large effects on real returns on savings and investments of retail investors both in the immediate term as well as in the long term. Retail investors may be unaware of inflation or not pay enough attention to its effects on their assets and purchasing power. Consumers can suffer from behavioral biases, such as money illusion or exponential growth bias, that can lead to insufficient saving and investing. Moreover, when inflation is rising, the effects of insufficient saving on long-term wealth become more pronounced.

Insurer positions are affected by inflation on both on the asset and liabilities side typically negative net effects for the non-life segment. On the asset side, insurer investments whose market prices are sensitive to inflation will see a direct or indirect impact through movements of the interest rates. On the liability side, inflation affects insurers through higher costs of claims. This is mostly relevant for non-life lines of business, because non-life guarantees are in nominal terms; crucially, insurers’ build-up provisions for future claims payments and in doing so they must make assumptions today about future price developments. Life insurers are less affected by costs of claims, these typically have liabilities in nominal terms, i.e. claims do not increase with the price development; this is because potential future benefits are often stipulated at inception. Higher general costs can have negative profitability implication for both life and non-life. Finally, the sensitivity on inflation and to interest rate depends also crucially on the duration gap of the undertakings: those with positive duration gaps are more likely to be negatively affected by inflation than those with negative long duration gap, such as life insurers.

On the liability side, the price development relevant for claims expenses, i.e. claims inflation, is particularly important for insurers. Claims inflation tends to outpace the general inflation rate, claims cost depends only to a small extent on inflation as measured by the Harmonized Index of Consumer Prices (HICP); the reason is that the goods for which insurers pay are significantly different from those which consumers buy. Moreover, claims of insurers encompass various costs, not just costs of goods and services. For Europe, there are no time series available on estimates of future claims inflation; each insurer makes its own business line specific forecast.

Developments in the term structure and risk premia, which remain uncertain, are also having an impact on the net effect on insurer positions, through their exposure to interest rate sensitive assets and the duration of their liabilities. A potential increase in long-term rates would be accompanied by a repricing of the risk premia, and the negative impact on the asset side would not be limited to the fixed income assets but would be reflected to other asset classes through the reduction of market prices. A similar scenario was tested in the EIOPA 2018 Stress Test exercise (Yield Curve Up scenario). This showed relatively high resilience of the insurance sector as a result of the solid capital buffers of the sector in aggregate.

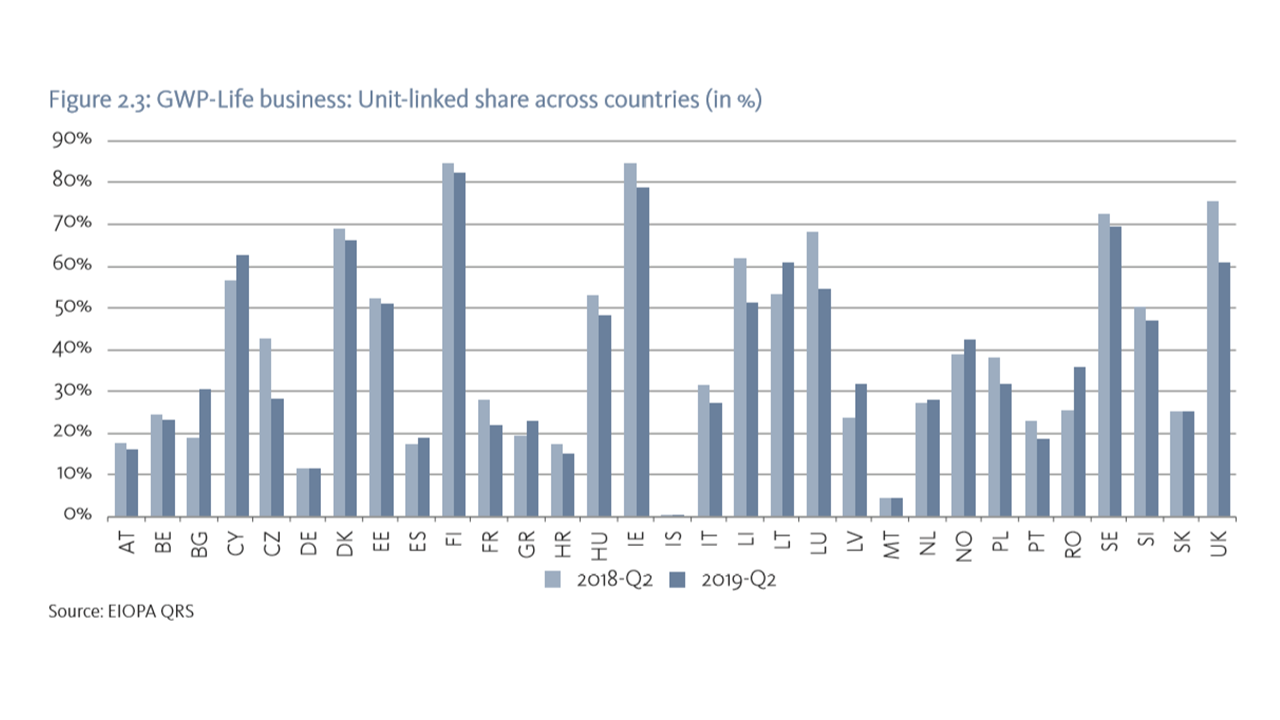

Insurance products can be sensitive to inflation, policyholders and pension beneficiaries face the risk of inflation eroding the real value of their benefits. This ultimately depends on the particular features and details of each contract sold. In the traditional business case of nominal interest rate guarantees, higher inflation than expected (relative to that already factored in the guarantees) has a negative impact in real terms for the policyholder, while contracts with profit sharing may help policyholder returns. In case of unit-linked policies, the policyholder can select the underlying assets from a range of investments e.g. mutual funds. The allocation could involve assets that provide inflation protection or not. Crucially, it requires policyholder financial knowledge/literacy to navigate through the complex dynamics of how investments affect their benefits. In the last years, the share of unit-linked in the life segment continues to increase, now reaching a peak of 39% since the introduction of Solvency II reporting, notwithstanding the considerable differences in the popularity of unit-linked products that remain across countries.

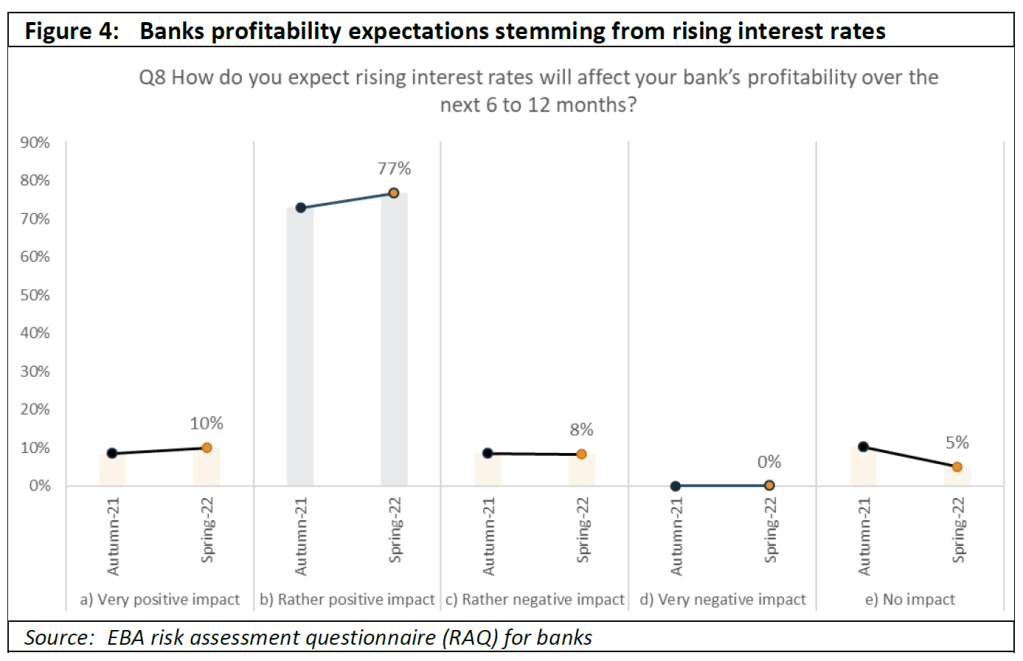

In the banking sector, increasing interest rates are usually expected to have a positive impact on interest income and on net interest margins (NIMs). Accordingly, a vast majority of banks responding to the spring 2022 EBA RAQ expect a positive impact on their profitability from rising interest rates with a repricing of assets. Both banks and analysts are optimistic about the impact of rising rates, and 85% of banks responding to the RAQ expect rising rates to have a positive impact on their profitability. However, analysts also expect an increase in provisions and impairments (at 80%, compared to 15% in the previous RAQ). Since 2014 NIMs have steadily decreased in the very low interest rate environment, and have remained nearly stable since Q1 2021 (1.25% in Q2 2022).

In spite of positive expectations, historic episodes of rising interest rates globally, as well as bank profitability trends in some European countries with an earlier cycle of increasing interest rates offer some indication that NIM may not improve substantially with rising interest rates. Expectations for a substantively positive impact on profitability may be overly optimistic. For example, during periods of stagflation in the USA between 1971 and 1973 and between 1976 and 1980, the sensitivity of NIM to interest rate rises was negligible. Disclosures from banks’ interest rate risks in the banking book (IRRBB) indicate that a parallel shift up of the yield curve positively affects NII for most banks. Yet, while about half of banks disclosing their IRRBB assume that a 200bp parallel rise of the yield curve will add at least a 10% to their NII, a majority of banks assume a negative net impact on their economic value of equity (EVE), a long-term measure of their interest rate risk.

On the liabilities’ side, bank funding costs have increased considerably in line with rising interest rates, which affects profitability. In the next months, analysts expect a broad-based increase in funding costs, including for deposits. Banks, particularly those relying more on wholesale funding, may be affected by a potential substantial increase in funding costs that could even offset positive effects from asset repricing. Banks that need to further build up their loss absorbing capacity could be particularly affected, as a majority of banks consider pricing as main constraint to issuing instruments eligible for MREL. In line with rising inflation, EU banks’ operating costs are also expected to increase further and have already increased substantially in 1Q22.

While general expectations suggest that banks will benefit from a repricing of assets amid rising interest rates, increasing rates might also affect borrower ability to service their debt, and could thus affect asset quality. Coupled with a deteriorating economic outlook, the rising interest rate environment risks in resulting in a reversal of the long-term trend of declining NPL in the banking sector. Rising rates could also contribute to adjustments to the already high real estate valuations in Europe, while the high levels of real estate exposure of EU banks has been identified as a risk. Monetary tightening might also impact lending growth, when, e.g., tightening is accompanied by lower GDP growth, and so could affect interest income.

5 DIGITAL RELATED RISKS The Russian war in Ukraine and the increasingly volatile geopolitical environment have heightened cybersecurity risks. The frequency of cyber incidents impacting all sectors of activity, as measured by publicly available data, increased significantly in the first quarter of 2022 compared to the same quarter of last year. The potential for escalation involving cyberattacks remains, and a successful attack on a major financial institution or on a critical infrastructure could spread across the entire financial system. Potential consequences also grow ever more far-reaching as the digitalization trend of the financial sector continues. These include disruptions to business continuity, as well as impact on reputation and, in extreme scenarios, liquidity and financial stability. Potential cyberattacks might not be limited to the financial sector only, but also to consumers. In a severe scenario, access to basic services could be impaired, including financial services, and personal data could be compromised.

The sharp market sell-off in May and June 2022 once again demonstrated the extremely volatile and speculative nature of many crypto-assets and related products and the high risks involved for investors, as highlighted in the recent joint-ESAs Warning. The collapse of the Terra ecosystem in May exposed fragilities in stable coins markets, which if left unmanaged, could have ripple effects with negative implications for financial stability, calling for a swift implementation of the Markets in Crypto Assets (MiCA) proposed regulation.

The current geopolitical situation underscores the relevance of the legislation on digital operational resilience (DORA). DORA, which builds on the ESAs Joint Advice in the area of information and communication technology (ICT), is expected to enter into force in early 2023. On 10 May 2022 co-legislators reached a provisional political agreement on its final text. DORA aims to establish a comprehensive framework on digital operational resilience for EU financial entities, and consolidate and upgrade ICT risk requirements spread over various financial services legislation (e.g. PSD2, MiFID, NIS). The geopolitical situation has highlighted some of the risks that DORA will address and underscores the importance of the legislation. The ESAs will be working closely together on the many joint deliverables and new tasks under DORA to help implement the legislation. Moreover, the ESAs, in cooperation with NCAs, have launched a high-level exercise (covering a sample of financial entities) to obtain a better understanding of the exposure of the financial sector to ICT third party providers. The exercise will help authorities and entities to prepare for the forthcoming DORA regime for oversight of critical third-party providers of ICT services.

Digitalization and cyber risks are currently assessed as high and show an increasing trend for the financial sector. In the banking sector, cyber risks are assessed to be very high by both banks and supervisors. The insurance, banking and markets sectors likewise remain on high alert. Since the beginning of the war, cyber-related incidents and disruptions beyond Ukraine and Russia have been rather limited to date, but related risks nevertheless remain unabatedly high. Cyber negative sentiment in the insurance sector, measured as the frequency of negative cyber terms pronounced during insurers’ earning calls, indicates an increased concern in the first quarter of 2022. From an insurance cyber underwriting perspective, cyber-related claims are increasing alongside a growth in the frequency and sophistication of cyber-attacks across financial sectors. In response to increasing cyber-attacks, cyber insurers are strengthening the wording to protect them against losses and could eventually also adjust pricing. Insurers seem to have pushed up attempts to tighten policies and to clarify coverage in the case of a retaliation by Russia and its allies in response to sanctions – the so-called war exclusion, which dictates that losses caused by armed conflict are usually not compensated. In this context, clear communication and disclosure to policyholders on the scope of the coverage and level of protection offered by insurance policies is crucial, in order to avoid a mismatch between their expectations and the actual coverage provided.

Supervisors aim at enhancing monitoring of cyber-related risk framework due to the increased relevance of digitalization and cyber risks. ESMA has recently facilitated increased information-sharing among its competent authorities to ensure supervisors receive timely updates on cyber incidents to inform their work. Turning to the insurance sector, EIOPA has produced exploratory indicators that rely on supervisor responses to the EIOPA Insurance Bottom-Up Survey and on publicly available external data. They will be improved once new supervisory data becomes available. To establish an adequate assessment and mitigation tools to address potential systemic cyber and extreme risks, throughout 2022 and 2023 EIOPA will be working on improving its methodological framework for bottom-up insurance stress tests, including cyber risk.

The unexpected COVID-19 virus outbreak led European countries to shut down major part of their economies aiming at containing the outbreak. Financial markets experienced huge losses and flight-to-quality investment behaviour. Governments and central banks committed to the provision of significant emergency packages to support the economy, as the economic shock, caused by demand and supply disruptions accompanied by its reflection to the financial markets, is expected to challenge economic growth, labour market and the consumer sentiment across Europe for an uncertain period of time.

Amid an unprecedented downward shift of interest rate curves during March, reflecting the flight-to-quality behaviour, credit spreads of corporates and sovereigns increased for riskier assets, leading effectively to a double-hit scenario. Equity markets dramatically dropped showing extreme levels of volatility responding to the uncertainties on virus effects and on the status of government and central banks support programs and their effectiveness. Despite the stressed market environment, there were signs of improvement following the announcements of the support packages and during the course of the initiatives of gradually reopening the economies. The virus outbreak also led to extraordinary working conditions, with part of the services sector working from home, which rises the potential of those conditions being preserved after the virus outbreak, which could decrease demand and market value for commercial real estate investments.

Within this challenging environment, insurers are exposed in terms of solvency risk, profitability risk and reinvestment risk. The sudden reassessment of risk premia and the increase of default risk could trigger large-scale rating downgrades and result in decreased investments’ value for insurers and IORPs, especially for exposures to highly indebted corporates and sovereigns. On the other hand, the risk of ultra-low interest rates for long has further increased. Factoring in the knock on effects of the weakening macro economy, future own funds position of the insurers could be further challenged, due to potential lower levels of profitable new business written accompanied by increased volume of profitable in-force policies being surrendered or lapsed.

Finally, liquidity risk has resurfaced, due to the potential of mass lapse type of events and higher than expected virus and litigation related claims accompanied by the decreased inflows of premiums.

For the European occupational pension sector, the negative impact of COVID-19 on the asset side is mainly driven by deteriorating equity market prices, as, in a number of Member States, IORPs allocate significant proportions of the asset portfolio (up to nearly 60%) in equity investments. However, the investment allocation is highly divergent amongst Member States, so that IORPs in other Member States hold up to 70% of their investments in bonds, mostly sovereign bonds, where the widening of credit spreads impair their market value. The liability side is already pressured due to low interest rates and, where market-consistent valuation is applied, due to low discount rates. The funding and solvency ratios of IORPs are determined by national law and, as could be seen in the 2019 IORP stress test results, have been under pressure and are certainly negatively impacted by this crisis. The current situation may lead to benefit cuts for members and may require sponsoring undertakings to finance funding gaps, which may lead to additional pressure on the real economy and on entities sponsoring an IORP.

Climate risks remain one of the focal points for the insurance and pension industry, with Environmental, Social and Governance (ESG) factors increasingly shaping investment decisions of insurers and pension funds but also affecting their underwriting. In response to climate related risks, the EU presented in mid-December the European Green Deal, a roadmap for making the EU climate neutral by 2050, providing actions meant to boost the efficient use of resources by

moving to a clean, circular economy and stop climate change,

revert biodiversity loss

and cut pollution.

At the same time, natural catastrophe related losses were milder than previous year, but asymmetrically shifted towards poorer countries lacking relevant insurance coverages.

Cyber risks have become increasingly relevant across the financial system in particular during the virus outbreak due to the new working conditions that the confinement measures imposed. Amid the extraordinary en masse remote working arrangements an increased number of cyber-attacks has been reported on both individuals and healthcare systems. With increasing attention for cyber risks both at national and European level, EIOPA contributed to building a strong, reliable, cyber insurance market by publishing its strategy for cyber underwriting and has also been actively involved in promoting cyber resilience in the insurance and pensions sectors.

The ebb and flow of attitudes on the adoption and use of technology has evolving ramifications for financial services firms and their compliance functions, according to the findings of the Thomson Reuters Regulatory Intelligence’s fourth annual survey on fintech, regtech and the role of compliance. This year’s survey results represent the views and experiences of almost 400 compliance and risk practitioners worldwide.

During the lifetime of the report it has had nearly 2,000 responses and been downloaded nearly 10,000 times by firms, risk and compliance practitioners, regulators, consultancies, law firms and global systemically-important financial institutions (G-SIFIs). The report also highlights the shifting role of the regulator and concerns about best or better practice approaches to tackle the rise of cyber risk. The findings have become a trusted source of insight for firms, regulators and their advisers alike. They are intended to help regulated firms with planning, resourcing and direction, and to allow them to benchmark whether their resources, skills, strategy and expectations are in line with those of the wider industry. As with previous reports, regional and G-SIFI results are split out where they highlight any particular trend. One challenge for firms is the need to acquire the skill sets which are essential if they are to reap the expected benefits of technological solutions. Equally, regulators and policymakers need to have the appropriate up-todate skillsets to enable consistent oversight of the use of technology in financial services. Firms themselves, and G-SIFIs in particular, have made substantial investments in skills and the upgrading of legacy systems.

Key findings

The involvement of risk and compliance functions in their firm’s approach to fintech, regtech and insurtech continues to evolve. Some 65% of firms reported their risk and compliance function was either fully engaged and consulted or had some involvement (59% in prior year). In the G-SIFI population 69% reported at least some involvement with those reporting their compliance function as being fully engaged and consulted almost doubling from 13% in 2018, to 25% in 2019. There is an even more positive picture presented on increasing board involvement in the firm’s approach to fintech, regtech and insurtech. A total of 62% of firms reported their board being fully engaged and consulted or having some involvement, up from 54% in the prior year. For G-SIFIs 85% reported their board being fully engaged and consulted or having some involvement, up from 56% in the prior year. In particular, 37% of G-SIFIs reported their board was fully engaged with and consulted on the firm’s approach to fintech, regtech and insurtech, up from 13% in the prior year.

Opinion on technological innovation and digital disruption has fluctuated in the past couple of years. Overall, the level of positivity about fintech innovation and digital disruption has increased, after a slight dip in 2018. In 2019, 83% of firms have a positive view of fintech innovation (23% extremely positive, 60% mostly positive), compared with 74% in 2018 and 83% in 2017. In the G-SIFI population the positivity rises to 92%. There are regional variations, with the UK and Europe reporting a 97% positive view at one end going down to a 75% positive view in the United States.

There has been a similar ebb and flow of opinion about regtech innovation and digital disruption although at lower levels. A total of 77% reported either an extremely or mostly positive view, up from 71% in the prior year. For G-SIFIs 81% had a positive view, up from 76% in the prior year.

G-SIFIs have reported a significant investment in specialist skills for both risk and compliance functions and at board level. Some 21% of G-SIFIs reported they had invested in and/or appointed people with specialist skills to the board to accommodate developments in fintech, insurtech and regtech, up from 2% in the prior year. This means in turn 79% of G-SIFIs have not completed their work in this area, which is potentially disturbing. Similarly, 25% of G-SIFIs have invested in specialist skills for the risk and compliance functions, up from 9% in the prior year. In the wider population 10% reported investing in specialist skills at board level and 16% reported investing in specialist skills for the risk and compliance function. A quarter (26%) reported they have yet to invest in specialist skills for the risk and compliance function, but they know it is needed (32% for board-level specialist skills). Again, these figures suggest 75% of G-SIFIs have not fully upgraded their risk and compliance functions, rising to 84% in the wider population.

The greatest financial technology challenge firms expect to face in the next 12 months have changed in nature since the previous survey, with the top three challenges cited as keeping up with technological advancements; budgetary limitations, lack of investment and cost; and data security. In prior years, the biggest challenges related to the need to upgrade legacy systems and processes as well as budgetary limitations, the adequacy and availability of skilled resources together with the need for cyber resilience. In terms of the greatest benefits expected to be seen from financial technology in the next 12 months the top three are a strengthening of operational efficiency, improved services for customers and greater business opportunities.

G-SIFIs are leading the way on the implementation of regtech solutions. Some 14% of G-SIFIs have implemented a regtech solution, up from 9% in the prior year with 75% (52% in the prior year) reporting they have either fully or partially implemented a regtech solution to help manage compliance. In the wider population, 17% reported implementing a regtech solution, up from 8% in the prior year. The 2018 numbers overall showed a profound dip from 2017 when 29% of G-SIFIs and 30% of firms reported implementing a regtech solution, perhaps highlighting that early adoption of regtech solutions was less than smooth.

Where firms have not yet deployed fintech or regtech solutions various reasons were cited as to what was holding them back. Significantly, one third of firms cited lack of investment; a similar number of firms pointed to a lack of in-house skills and information security/data protection concerns. Some 14% of firms and 12% of G-SIFIs reported they had taken a deliberate strategic decision not to deploy fintech or regtech solutions yet.

There continues to be substantial variation in the overall budget available for regtech solutions. A total of 38% of firms (31% in prior year) reported that the expected budget would grow in the coming year, however, 31% said they lack a budget for regtech (25% in the prior year). For G-SIFIs 48% expected the budget to grow (36% in prior year), with 12% reporting no budget for regtech solutions (6% in the prior year).

Focus : Challenges for firms

Technological challenges for firms come in all shapes and sizes. There is the potential, marketplace changing, challenge posed by the rise of bigtech. There is also the evolving approach of regulators and the need to invest in specialist skill sets. Lastly, there is the emerging need to keep up with technological advances themselves.

The challenges for firms have moved on. In the first three years of the report the biggest financial technology challenge facing firms was that of the need to upgrade legacy systems and processes. This year the top three challenges are expected to be the need to keep up with technology advancements; perceived budgetary limitations, lack of investment and cost, and then data security.

Focus : Cyber risk

Cyber risk and the need to be cyber-resilient is a major challenge for financial services firms which are targets for hackers. They must be prepared and be able to respond to any kind of cyber incident. Good customer outcomes will be under threat if cyber resilience fails.

One of the most prevalent forms of cyber attack is ransomware. There are different types of ransomware, all of which will seek to prevent a firm or an individual from using their IT systems and will ask for something (usually payment of a ransom) to be done before access will be restored. Even then, there is no guarantee that paying the fine or acceding to the ransomware attacker’s demands will restore full access to all IT systems, data or files. Many firms have found that critical files often containing client data have been encrypted as part of an attack and large amounts of money are demanded for restoration. Encryption is in this instance used as a weapon and it can be practically impossible to reverse-engineer the encryption or “crack” the files without the original encryption key – which cyber attackers deliberately withhold. What was previously viewed often as an IT problem has become a significant issue for risk and compliance functions. The regulatory stance is typified by the UK Financial Conduct Authority (FCA) which has said its goal is to “help firms become more resilient to cyber attacks, while ensuring that consumers are protected and market integrity is upheld”. Regulators do not expect firms to be impervious but do expect cyber risk management to become a core competency.

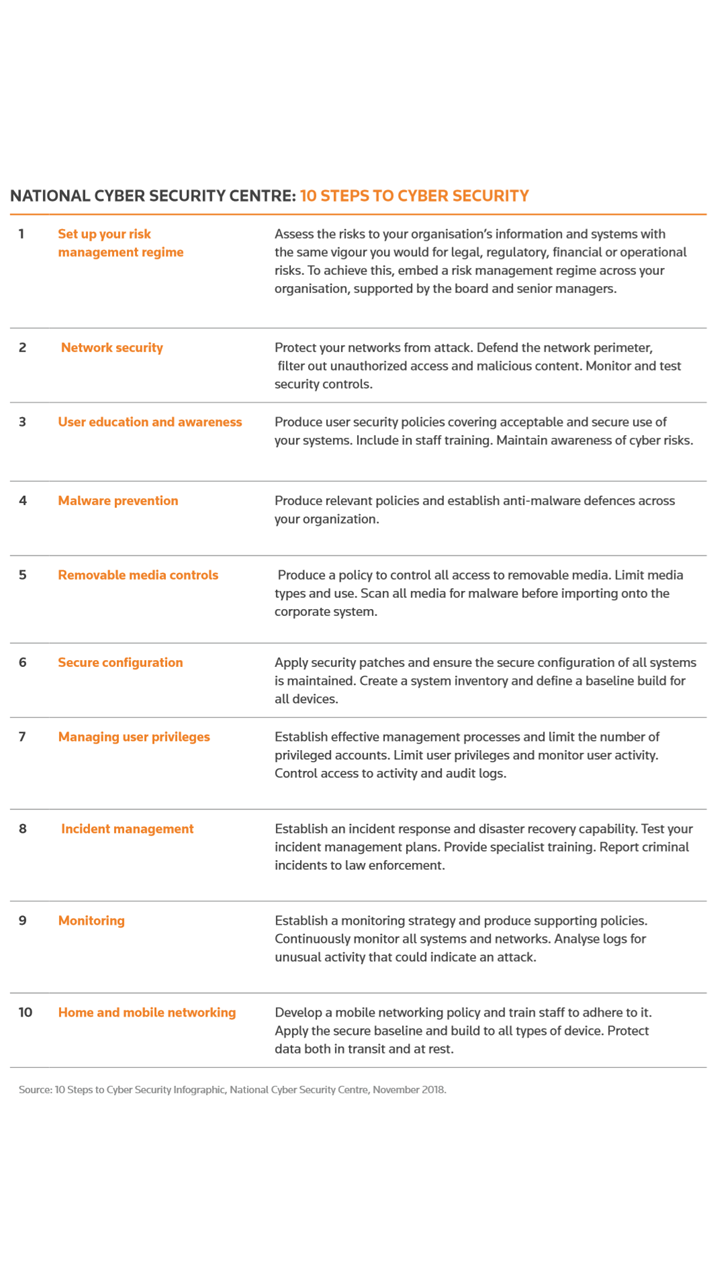

Good and better practice on defending against ransomware attacks Risk and compliance officers do not need to become technological experts overnight but must ensure cyber risks are effectively managed and reported on within their firm’s corporate governance framework. For some compliance officers, cyber risk may be well outside their comfort zone but there is evidence that simple steps implemented rigorously can go a long way towards protecting a firm and its customers. Any basic cyber-security hygiene aimed at protecting businesses from ransomware attacks should make full use of the wide range of resources available on cyber resilience, IT security and protecting against malware attacks. The UK National Cyber Security Centre has produced some practical guidance on how organizations can protect themselves in cyberspace, which it updates regularly. Indeed, the NCSC’s 10 steps to cyber security have now been adopted by most of the FTSE350.

Closing thoughts

The financial services industry has much to gain from the effective implementation of fintech, regtech and insurtech but practical reality is there are numerous challenges to overcome before the potential benefits can be realised. Investment continues to be needed in skill sets, systems upgrades and cyber resilience before firms can deliver technological innovation without endangering good customer outcomes.

An added complication is the business need to innovate while looking over one shoulder at the threat posed by bigtech. There are also concerns for solution providers. The last year has seen many technology start-ups going bust and far fewer new start-ups getting off the ground – an apparent parallel, at least on the surface, to the bubble that was around dotcom. Solutions need to be practical, providers need to be careful not to over promise and under deliver and above all developments should be aimed at genuine problems and not be solutions looking for a problem. There are nevertheless potentially substantive benefits to be gained from implementing fintech, regtech and insurtech solutions. For risk and compliance functions much of the benefit may come from the ability to automate rote processes with increasing accuracy and speed. Indeed, when 900 respondents to the 10th annual cost of compliance survey report were asked to look into their crystal balls and predict the biggest change for compliance in the next 10 years, the largest response was automation.