Regulation is only effective for as long as it remains relevant. While EIOPA is evolving into a supervisory-focused organisation, it pays close attention to how regulation is applied and how effective it remains, with a view to reinforcing cross-sectoral consistency and improving fairness and transparency and with a focus on better and smart regulation.

INSURANCE

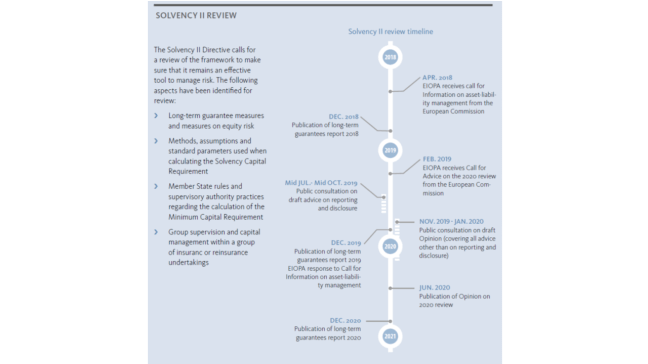

- SOLVENCY II REVIEW

Since the successful implementation of Solvency II Directive in 2016, EIOPA played an important role in monitoring its consistent implementation and during 2018 was able to provide valuable input into preparations for its review.

EIOPA provided advice to the European Commission on the review of the Solvency Capital Requirement based on an in-depth analysis of 29 different elements of the Standard Formula. The advice focused on increasing proportionality, removing unjustified constraints to financing the economy and removing technical inconsistencies.

EIOPA proposed further simplifications and reduced the burden to insurers by:

- Further simplifying calculations for a number of sub-modules of the Solvency Capital Requirement (SCR) such as natural, man-made and health catastrophes, in particular fire risk and mass accident;

- Simplifying the use of external credit ratings in the calculation of the SCR (an issue especially relevant for small insurers);

- Reducing the burden of the treatment of lookthrough to underlying investments;

- Developing simplifications in the assessment of lapse and counterparty default risks;

- Recommending the use of undertaking specific parameters for reinsurance stop-loss treaties.

Furthermore, one of the major technical inconsistencies found related to the calculation of interest rate risk, which did not capture very low or even negative interest rates. EIOPA recommended to adjust the methodology using a method already adopted by internal model users and, given the material impact on capital requirements, suggested to implement it gradually over three years.

EIOPA also carried out an analysis of the loss-absorbing capacity of deferred taxes practices. In face of the evidence of wide diversity, especially concerning the projection of future profits, EIOPA proposed a set of key principles that will ensure greater convergence and level playing field, while maintaining a certain degree of flexibility.

Finally, EIOPA analysed the treatment and the evidence available on unrated debt and unlisted equity and proposed criteria for a more granular treatment, namely with the use of financial ratios.

In some areas, the analysis of recent developments did not provide for sufficient reasons to change. This is, for example, the case of mortality and longevity risks and the cost of capital in the calculation of the risk margin. The evolution of financial markets does not justify a change in the cost of capital: the decrease in interest rates has not lead to a decrease in the cost of raising equity.

- REPORTING ON THE IMPLEMENTATION OF SOLVENCY II

In 2018, EIOPA published a number of reports related to different aspects of Solvency II.

- Report on group supervision and capital management

In response to a European Commission’s request for information, EIOPA submitted its Report on Group Supervision and Capital Management of (Re)Insurance Undertakings and specific topics related to Freedom to Provide Services (FoS) and Freedom of Establishment (FoE) under the Solvency II Directive. The report concluded that overall the Solvency II Group supervision regime was operating satisfactorily. The tools developed by EIOPA to further strengthen group supervision and supervision of cross-border issues contributed to further convergence of practices of NCAs’ supervisory practices.

The report also highlighted a number of gaps in the regulatory framework, including issues related to the application of Solvency II requirements for determining scope of insurance groups subject to Solvency II group supervision, the application of certain of these provisions governing the calculation of group solvency in particular where several methods are used, the definition and supervision of intra-group transactions, or the application of governance requirements at group level.

Further, EIOPA’s report emphasised that effective supervision of insurance groups will benefit from a harmonised approach on a number of areas, for example, early intervention, recovery and resolution and the assessment of group own funds.

- Second annual report on the use of capital addons under Solvency II

In December 2018, EIOPA published its second annual report on the use of capital add-ons by NCAs according to Article 52 of Solvency II. The objective was to contribute to a higher degree of supervisory convergence in the use of capital add-ons between supervisory authorities and to highlight any concerns regarding the capital add-ons framework. In general, the capital add-on appears to be a good and positive measure to adjust the Solvency Capital Requirement to the risks of the undertaking, when the application of other measures, for example the development of an internal model, is not adequate.

- Third annual report on the use of limitations and exemptions from reporting under Solvency II

This report, published in December 2018, addresses the proportionality principle on the reporting requirements, from which the limitations and exemptions on reporting – as foreseen in Article 35 of the Solvency II Directive – are just one of the existing proportionality tools. Reporting requirements also reflect a natural embedded proportionality and in addition, risk-based thresholds were included in the reporting Implementing Technical Standard (ITS).

- Third annual report on the use and impact of long-term guarantee measures and measures on equity risk

This is a regular report published in accordance with Article 77f(1) of the Solvency II Directive. This year’s report also included an analysis on risk management aspects in view of the specific requirements for LTG measures set out in Article 44 and 45 of the Directive as well as an analysis of detailed features and types of guarantees of products with long-term guarantees.

This report shows that – as in previous years – most of the measures, in particular the volatility adjustment and the transitional measures on technical provisions are widely used. The average Solvency Capital Requirement (SCR) ratio of undertakings using the voluntary measures is 231 % and would drop to 172 % if the measures were not applied. This confirms the importance of the measures for the financial position of (re)insurance undertakings.

- INVESTIGATING ILLIQUID LIABILITIES

The treatment of long-term insurance business remains a hotly debated issue. In particular, it has been discussed whether the risks of long-term insurance business and the associated investments backing those long-term insurance business are adequately reflected. The illiquidity characteristics of liabilities may contribute to the ability of insurers to mitigate short-term volatility by holding assets throughout the duration of the commitments, even in times of market stress.

To explore any new evidence on the features of liabilities, especially concerning their illiquidity characteristics, a dedicated EIOPA Project Group on illiquid liabilities was set up with the following main goals:

- To identify criteria of liquidity characteristics for the liabilities and measures for insurers’ ability to invest over the long term;

- To explore the link between the characteristics of liabilities and the management of insurers’ assets;

- To analyse whether the current treatment in the regulatory regime appropriately addresses the risks associated with the long-term nature of the insurance business.

Following a request for information from the European Commission on asset and liability management, EIOPA launched a request for feedback on illiquid liabilities in autumn and held a roundtable with interested stakeholders in December to discuss the submitted responses on illiquidity measurements and asset liability management practices.

- ANALYSIS OF THE INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRS) 17 INSURANCE CONTRACTS

Following the publication of International Financial Reporting Standards (IFRS) 17 Insurance Contracts by the International Accounting Standards Board (IASB), EIOPA assessed its potential effects on financial stability and the European public good, on product design, supply and demand of insurance contracts, and the practical implementation in light of the applicable inputs and processes for Solvency II.

EIOPA concluded that the introduction of IFRS 17 can be described as positive paradigm shift compared to its predecessor IFRS 4 Insurance Contracts, bringing increased transparency, comparability and additional insights on insures’ business models. EIOPA, however, noted a few reservations regarding concepts that may affect comparability and relevance of IFRS 17 financial statements.

PENSIONS

EIOPA promotes greater transparency in the European pensions sector. In support of this aim, EIOPA is working to enhance the information available to consumers and supporting pension providers by making clear the expectations, justifications and decisions linked with the information they provide, in particular to prospective members, members and beneficiaries as laid out in Articles 38 – 44 of the EU Directive on the activities and supervision of institutions for occupational retirement provision (IORP II).

- REPORT ON THE PENSION BENEFIT STATEMENT: GUIDANCE AND PRINCIPLESBASED PRACTICES IMPLEMENTING IORP II

The report presents the outcomes of NCA exchanges of views and assessments of current practices for the implementation of the IORP II Pensions Benefit Statement (PBS) requirement. Based on this investigation, several principles have been identified that will facilitate clear understanding and comparability of statements.

Two proposals are now in further development: a basic PBS and an advanced PBS (containing more detailed information) to meet the PBS goals. These proposals will, as far as possible, take account of the behavioral approach principle be subject to further consumer testing.

- DECISION ON THE CROSS-BORDER COLLABORATION OF NCAS WITH RESPECT TO IORP II DIRECTIVE

This Decision, published in November 2018, replaces the former Budapest Protocol which had to be revised as a result of the new IORP II Directive. The Decision introduces new rules to improve the way occupational pension funds are governed, to enhance information transparency to pension savers and to clarify the procedures for carrying out cross-border transfers and activities.

The Decision also describes different situations and possibilities for NCAs to exchange information about cross-border activities in relation to the ‘fit and proper’ assessment and the outsourcing of key functions, both new provisions of the IORP II Directive in addition to the cross-border transfer.

PRESERVING FINANCIAL STABILITY

As part of EIOPA’s mandate to safeguard financial stability, EIOPA works to identify trends, potential risks and vulnerabilities that could have a negative effect on the pension and insurance sectors across Europe.

- 2018 INSURANCE STRESS TEST

EIOPA published the results of its stress test of the European insurance sector in December 2018. This exercise assessed the participating insurers’ resilience to the three severe but plausible scenarios: a yield curve up shock combined with lapse and provisions deficiency shocks; a yield curve down shock combined with longevity stress; and a series of natural catastrophes.

In total, 42 European (re)insurance groups participated representing a market coverage of around 75 % based on total consolidate assets. EIOPA published for the first time the post-stress estimation of the capital position (Solvency Capital Requirement ratio) of major EU (re)insurance groups.

Overall, the stress test confirmed the significant sensitivity to market shocks combined with specific shocks relevant for the European insurance sector. On aggregate, the sector is adequately capitalised to absorb the prescribed shocks. Participating groups demonstrated a high resilience to the series of natural catastrophes tested, showing the importance of the risk transfer mechanisms, namely reinsurance, in place.

An additional objective of this exercise, stemming from recommendations from the European Court of Auditors, was to increase transparency in order to reinforce market discipline by requesting the voluntary disclosure of a list of individual stress test indicators by the participating groups. Since EIOPA does not have the power to impose the disclosure of individual results, participating groups were asked for their voluntary consent to the publication of a list of individual stress test indicators. Only four of the 42 participating groups provided such consent.

- RISK DASHBOARD

EIOPA publishes a risk dashboard on a quarterly basis and a financial stability report twice a year. In the December 2018 report, EIOPA concluded:

- the persistent low yield environment remains challenging for insurers and pension funds;

- the risk of a sudden reassessment of risk premia has become more pronounced over recent months amid rising political and policy uncertainty;

- interconnectedness with banks and domestic sovereigns remains high for European insurers, making them susceptible to potential spillovers;

- some European insurers are significantly exposed in their investment portfolios to climate-related risks and real estate.

- FINANCIAL STABILITY REPORT

EIOPA published two reports on the financial stability of the insurance and occupational pensions sector in 2018.

In general the persistent low yield environment remains challenging for both the insurance and pension fund sector, which continues to put pressure on profitability and solvency. However, towards the end of the year, as noted in the December report, the risk of a sudden reassessment of risk premia became more pronounced. This is largely due to rising political uncertainty and trade tensions, concerns over debt sustainability and the gradual normalisation of monetary policy. In the short run a sudden increase in yields driven by rising risk premia could significantly affect the financial and solvency position of insurers and pension funds as the investment portfolios could suffer large losses only partly offset by lower liabilities. In this regard, the high degree of interconnectedness with banks and domestic sovereigns of insurers could lead to potential spillovers in case a sudden reassessment of risk premia materialise.

While overall the insurance sector remains adequately capitalised, profitability is under increased pressure in the current low yield environment. The Solvency Capital Requirement ratio for the median company is 225 % for life and 206 % for non-life insurance sector, although significant disparities remain across undertakings and countries.

In the European occupational pension fund sector, total assets increased for the euro area and cover ratios slightly improved. However, the current macroeconomic environment and ongoing low interest rates continue to pose significant challenges to the sector, with the weighted return on assets considerably down in 2017.

- ENHANCED INFORMATION AND STATISTICS

EIOPA continuously works to improve the availability and quality of available information and statistics on insurance and pensions.

- Solvency II information

For the insurance sector, EIOPA publishes high-quality insurance statistics at both solo and group level. The statistics are based on Solvency II information from regulatory reporting and their regular publication demonstrates EIOPA’s commitment to transparency. Over the past year, through the increased availability of Solvency II data EIOPA has been able to increase the coverage of its statistics. In June 2018, for the first time, the Authority published further insight into the assets of solo (re)insurance undertakings at country level.

- Decision on EIOPA’s regular information requests towards NCAs regarding provision of occupational pensions information

In April 2018, the Authority published its decision regarding the submission of occupational pension information. The decision defined a single framework for the reporting of occupational pension information that facilitates reporting processes. As a result, EIOPA will receive the information required to carry out appropriate monitoring and assessment of market developments, as well as in-depth economic analyses of the occupational pension market. The requirements were developed in close cooperation with the European Central Bank in order to minimise the burden on the industry and will apply as of 2019.

- Pensions information taxonomy

In November 2018, EIOPA published the eXtensible Business Reporting Language (XBRL) Taxonomy applicable for reporting of information on IORPs. It provides NCAs with the technical means for the submission to EIOPA of harmonised information of all pension funds in the European Economic Area. Developed in close collaboration with the European Central Bank (ECB), it allows for integrated technical templates and means to report via a single submission both the information required by EIOPA and the ECB.

CRISIS PREVENTION

In addition to regular financial stability tools, EIOPA undertooka number of additional activities in 2018 related to crisis prevention.

- Development of a macroprudential framework for insurance

With the aim of contributing to the overall debate on systemic risk and macroprudential policy, over the last year, EIOPA has published a series of reports that extend the debate to the insurance sector and, more specifically, the characteristics of that sector. These reports cover the following:

- Systemic risk and macroprudential policy in insurance;

- Solvency II tools with macroprudential impact; and

- Other potential macroprudential tools and measures to enhance the current framework.

As a next step, EIOPA will consult on concrete proposals to include macroprudential elements in the upcoming review of Solvency II.

- Analysis of the causes and early identification of failures and near misses in insurance

In July 2018, EIOPA published ‘Failures and near misses in insurance: Overview of the causes and early identification’ as the first in a series aimed at enhancing supervisory knowledge of the prevention and management of insurance failures. The report’s findings are based on information contained in EIOPA’s database of failures and near misses, covering the period from 1999 to 2016, including sample data of 180 affected insurance undertakings in 31 European countries.

The report focuses on an examination of the causes of failure in insurance, as well as the assessment of the reported early identification signals. It also examines the underlying concepts ‘failure’ and ‘near miss’ as well as providing further information on EIOPA’s database, established in 2014.