The global and European economic outlook has deteriorated in the past months with weakening industrial production and business sentiment and ongoing uncertainties about trade disputes and Brexit. In particular, the “low for long” risk has resurfaced in the EU, as interest rates reached record lows in August 2019 and an increasing number of countries move into negative yield territory for their sovereign bonds even at longer maturities in anticipation of a further round of monetary easing by central banks and a general flight to safety. Bond yields and swap rates have since slightly recovered again, but protracted low interest rates form the key risk for both insurers and pension funds and put pressure on both the capital position and long-term profitability. Large declines in interest rates can also create further incentives for insurers and pension funds to search for yield, which could add to the build-up of vulnerabilities in the financial sector if not properly managed.

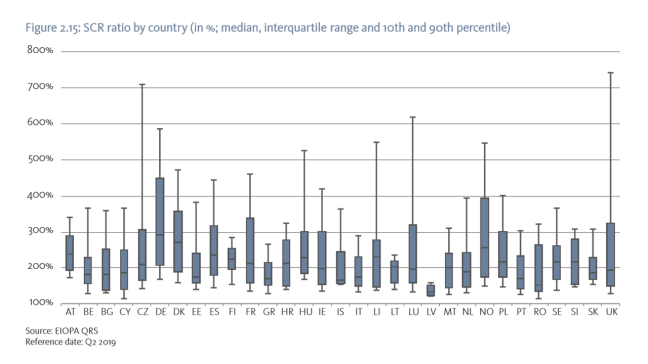

Despite the challenging environment, the European insurance sector remains overall well capitalized with a median SCR ratio of 212% as of Q2 2019. However, a slight deterioration could be observed for life insurers in the first half of 2019 and the low interest rate environment is expected to put further pressures on the capital positions of life insurers in the second half of 2019. At the same time, profitability improved in the first half of 2019, mainly due to valuation gains in the equity and bond portfolios of insurers. Nevertheless, the low yield environment is expected to put additional strains on the medium to long term profitability of insurers as higher yielding bonds will have to be replaced by lower yielding bonds, which may make it increasingly difficult for insurers to make investment returns in excess of guaranteed returns issued in the past, which are still prevalent in many countries.

THE EUROPEAN INSURANCE SECTOR

The challenging macroeconomic environment is leading insurance undertakings to further adapt their business models. In order to address the challenges associated with the low yield environment and improve profitability, life insurers are lowering guaranteed rates in traditional products and are increasingly focusing on unit-linked products. On the investment side, insurers are slowly moving towards more alternative investments and illiquid assets, such as unlisted equity, mortgages & loans, infrastructure and property. For non-life insurers, the challenge is mostly focused on managing increasing losses stemming from climate-related risks and cyber events, which may not be adequately reflected in risk models based on historical data, and continued competitive pressures.

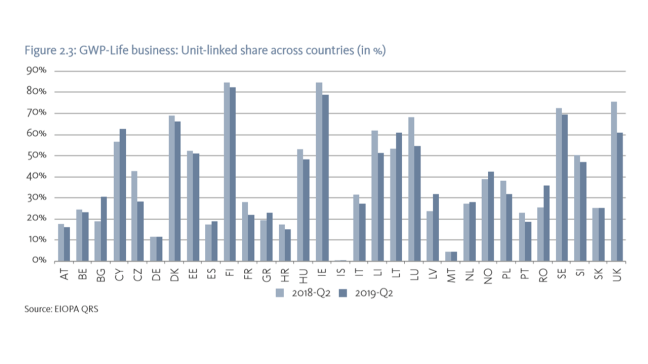

Despite the challenging environment, the European insurance sector overall gross written premiums slightly grew by 1.6% on an annual basis in Q2 2019. This growth is particularly driven by the increase in non life GWP (3.7%), in comparison to a slightly decrease in life (-0.5%). This reduction growth rate in life GWP is associated to the slowdown in the economic growth; however this does not seem to have affected the growth of non-life GWP to the same extent. Overall GWP as a percentage of GDP slightly increased from 9% to 11% for the European insurance market, likewise total assets as a share of GDP improved from 70% to 74%. The share of unit-linked business has slightly declined notwithstanding the growth expectations. Even though insurers are increasingly trying to shift towards unit-linked business in the current low yield environment, the total share of unit-linked business in life GWP has slightly decreased from 42% in Q2 2018 to 40% in Q2 2019, likewise the share for the median insurance company declined from 34% in Q2 2018 to 31% in Q2 2019. Considerable differences remain across countries, with some countries still being plagued by low trust due to misselling issues in the past. Overall, the trend towards unit-lead business means that investment risks are increasingly transferred to policyholders with potential reputational risks to the insurance sector in case investment returns turn out lower than anticipated.

The liquid asset ratio slightly deteriorated in the first half of 2019. The median value for liquid asset increased by 1.5% from 63.3% in 2018 Q2 to 64.8% in 2018 Q4, and after slightly decreased to 63.8% in Q2 2019. Furthermore, the distribution moved down (10th percentile reduced in the past year by 6 p.p. to 47.9%). Liquid assets are necessary in order to meet payment obligations when they are due. Furthermore, a potential increase in interest rate yields might directly impact the liquidity needs of insurers due to a significant increase in the lapse rate as policyholders might look for more attractive alternative investments.

Lapse rates in the life business remained stable slightly increased in the first half of 2019. The median value increased from 1.34% in Q2 2018 to 1.38% in Q2 2019. Moreover, a potential sudden reversal of risk premia and abruptly rising yields could trigger an increase in lapse rates and surrender ratios as policyholders might look for more attractive investments. Although several contractual and fiscal implications could limit the impact of lapses and surrenders in some countries, potential lapses by policyholders could add additional strains on insurers’ financial position once yields start increasing.

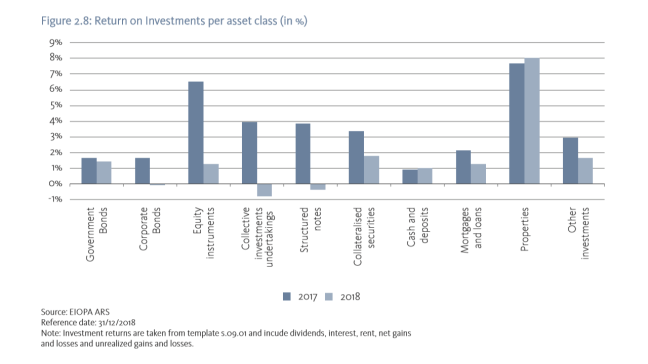

The return on investment has substantially declined further over 2018. The investment returns have significantly deteriorated for the main investment classes (bonds, equity and collective instruments). The median return on investment decreased to only 0.31% in 2018, compared to 2.83% in 2016 and 1.95% in 2017. In particular the four main investment options (government and corporate bonds, equity instruments and collective investment undertakings) – which approximately account for two-thirds of insurers’ total investment portfolios – have generated considerably lower or even negative returns in 2018. As a consequence, insurers may increasingly look for alternative investments, such as unlisted equities, mortgages and infrastructure to improve investment returns. This potential search for yield behaviour might differ per country and warrants close monitoring by supervisory authorities as insurers may suffer substantial losses on these more illiquid investments when markets turn sour.

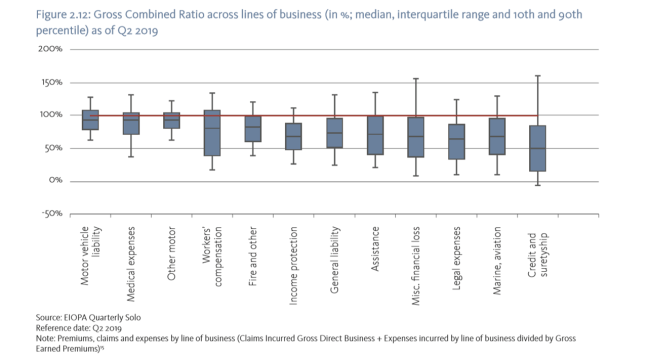

Despite the challenging investment climate, overall insurer profitability improved in the first half of 2019. The median return on assets (ROA) increased from 0.24% in Q2 2018 to 0.32% in Q2 2019, whereas the median return on excess of assets over liabilities (used as a proxy of return on equity), increased from 2.8% in Q2 2018 to 4.9 % in Q2 2019. The improvement in overall profitability seems to stem mainly from valuation gains in the investment portolio of insurers driven by a strong rebound in equity prices and declining yields (and hence increasing values of bond holdings) throughout the first half of 2019, while profitability could be further supported by strong underwriting results and insurers’ continued focus on cost optimisation. However, decreased expected profits in future premiums (EPIFP) from 11% in Q1 2019 to 10.3% in Q2 2019 suggest expectations of deteriorating profitability looking ahead. Underwriting profitability remained stable and overall positive in the first half of 2019. The median Gross Combined Ratio for non-life business remained below 100% in the first half of 2019 across all lines of business, indicating that most EEA insurers were able to generate positive underwriting results (excluding profits from investments). However, significant outliers can still be observed across lines of business, in particular for credit and suretyship insurance, indicating that several insurers have experienced substantial underwriting losses in this line of business. Furthermore, concerns of underpricing and underreserving remain in the highly competitive motor insurance markets.

Solvency positions slightly deteriorated in the first half of 2019 and the low interest rate environment is expected to put further pressures on the capital positions in the second half of the year, especially for life insurers. Furthermore, the number of life insurance undertakings with SCR ratios below the 100% threshold increased in comparison with the previous year from 1 in Q2 2018 to 4 in Q2 2019 mainly due to the low interest rate environment, while the number of non-life insurance undertakings with SCR ratios below 100% threshold decreased from 9 in Q2 2018 to 7 in Q2 2019. The median SCR ratio for life insurers is still the highest compared to non-life insurers and composite undertakings. However, the SCR ratio differs substantially among countries.

The impact of the LTG and transitional measures varies considerably across insurers and countries. The long term guarantees (LTG) and transitional measures were introduced in the Solvency II Directive to ensure an appropriate treatment of insurance products that include long-term guarantees and facilitate a smooth transition of the new regime. These measures can have a significant impact on the SCR ratio by allowing insurance undertakings, among others, to apply a premium to the risk free interest rate used for discounting technical provions. The impact of applying these measures is highest in DE and the UK, where the distribution of SCR ratios is signicantly lower without LTG and transitional measures (Figure 2.16). While it is important to take the effect of LTG measures and transitional measures into account when comparing across insurers and countries, the LTG measures do provide a potential financial stability cushion by reducing overall volatility.

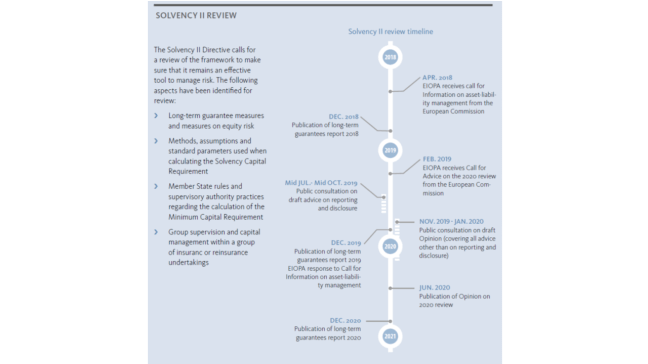

On October 15th 2019, EIOPA launched a public consultation on an Opinion that sets out technical advice for the 2020 review of Solvency II. The call for advice comprises 19 separate topics. Broadly speaking, these can be divided into three parts.

- The review of the LTG measures, where a number of different options are being consulted on, notably on extrapolation and on the volatility adjustment.

- The potential introduction of new regulatory tools in the Solvency II framework, notably on macro-prudential issues, recovery and resolution, and insurance guarantee schemes. These new regulatory tools are considered thoroughly in the consultation.

- Revisions to the existing Solvency II framework including in relation to

- freedom of services and establishment;

- reporting and disclosure;

- and the solvency capital requirement.

The main specific considerations and proposals of this consultation are as follows:

- Considerations to choose a later starting point for the extrapolation of risk-free interest rates for the euro or to change the extrapolation method to take into account market information beyond the starting point.

- Considerations to change the calculation of the volatility adjustment to risk-free interest rates, in particular to address overshooting effects and to reflect the illiquidity of insurance liabilities.

- The proposal to increase the calibration of the interest rate risk sub-module in line with empirical evidence, in particular the existence of negative interest rates. The proposal is consistent with the technical advice EIOPA provided on the Solvency Capital Requirement standard formula in 2018.

- The proposal to include macro-prudential tools in the Solvency II Directive.

- The proposal to establish a minimum harmonised and comprehensive recovery and resolution framework for insurance.

The European Supervisory Authorities (ESAs) published on the 4th October 2019 a Joint Opinion on the risks of money laundering and terrorist financing affecting the European Union’s financial sector. In this Joint Opinion, the ESAs identify and analyse current and emerging money laundering and terrorist financing (ML/ TF) risks to which the EU’s financial sector is exposed. In particular, the ESAs have identified that the main cross-cutting risks arise from

- the withdrawal of the United Kingdom (UK) from the EU,

- new technologies,

- virtual currencies,

- legislative divergence and divergent supervisory practices,

- weaknesses in internal controls,

- terrorist financing and de-risking;

in order to mitigate these risks, the ESAs have proposed a number of potential actions for the Competent Authorities.

Following its advice to the European Commission on the integration of sustainability risks in Solvency II and the Insurance Distribution Directive on April 2019, EIOPA has published on 30th September 2019 an Opinion on Sustainability within Solvency II, which addresses the integration of climate-related risks in Solvency II Pillar I requirements. EIOPA found no current evidence to support a change in the calibration of capital requirements for “green” or “brown” assets. In the opinion, EIOPA calls insurance and reinsurance undertakings to implement measures linked with climate change-related risks, especially in view of a substantial impact to their business strategy; in that respect, the importance of scenario analysis in the undertakings’ risk management is highlighted. To increase the European market and citizens’ resilience to climate change, undertakings are called to consider the impact of their underwriting practices on the environment. EIOPA also supports the development of new insurance products, adjustments in the design and pricing of the products and the engagement with public authorities, as part of the industry’s stewardship activity.

On the 15th July 2019 EIOPA submitted to the European Commission draft amendments to the Implementing technical standards (ITS) on reporting and the ITS on public disclosure. The proposed amendments are mainly intended to reflect the changes in the Solvency II Delegated Regulation by the Commission Delegated Regulation (EU) 2019/981 and the Commission Delegated Regulation 2018/1221 as regards the calculation of regulatory capital requirements for securitisations and simple, transparent and standardised securitisations held by insurance and reinsurance undertakings. A more detailed review of the reporting and disclosure requirements will be part of the 2020 review of Solvency II.

On 18th June 2019 the Commission Delegated Regulation (EU) 2019/981 amending the Solvency II Delegated Regulation with respect to the calculation of the SCR for standard formula users was published. The new regulation includes the majority of the changes proposed by EIOPA in its advice to the Commission in February 2018 with the exception of the proposed change regarding interest rate risk. Most of the changes are applicable since July 2019, although changes to the calculation of the loss-absorbing capacity of deferred taxes and non-life and health premium and reserve risk will apply from 1 January 2020.

RISK ASSESSMENT

QUALITATIVE RISK ASSESSMENT

EIOPA conducts twice a year a bottom-up survey among national supervisors to determine the key risks and challenges for the European insurance and pension fund sectors, based on their probability and potential impact.

The EIOPA qualitative Autumn 2019 Survey reveals that low interest rates remain the main risks for both the insurance and pension fund sectors. Equity risks also remain prevalent, ranking as the 3rd and 2nd biggest risk for the insurance and pension funds sectors respectively. The cyber risk category is now rank as the 2nd biggest risk for the insurance sector, as insurers need to adapt their business models to this new type of risk both from an operational risk perspective and an underwriting perspective. Geopolitical risks have become more significant for both markets, along with Macro risks, which continue to be present in the insurance and pension fund sectors, partially due to concerns over protectionism, trade tensions, debt sustainability, sudden increase in risk premia and uncertainty relating to the potential future post-Brexit landscape.

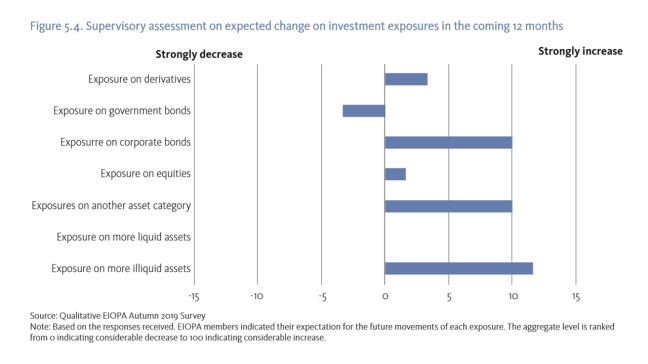

The survey further suggests that all the risks are expected to increase over the coming year. The increased risk of the low for long interest rate environment is in line with the observed market developments, particulary after the ECB’s announcement of renewed monetary easing in September 2019. The significant expected raise of cyber, property, equity, macro and geopolitical risks in the following year is also in line with the observed market developments, indicating increased geopolitical uncertainty, trade tensions, stretched valuations in equity and real estate markets and more frequent and sophisticated cyber attacks which could all potentially affect the financial position of insurers and pension funds. On the other hand, ALM risks and Credit risk for financials are expected to increase in the coming year, while in the last survey in Spring 2019 the expectations were following the opposite direction.

Although cyber risk is ranking as one of the top risks and expected to increase in the following year, many jurisdictions also see cyber-related insurance activities as a growth opportunity. The rapid pace of technological innovation and digitalisation is a challenge for the insurance market and insurers need to be able to adapt their business models to this challenging environment, nonetheless from a profitability perspective, increased digitalisation may offer significant cost-saving and revenue-increasing opportunities for insurance companies. The increase of awareness of cyber-risk and higher vulnerability to cyber threats among undertakings due to the increased adoption of digital technologies could drive a growth in cyber insurance underwriting.

The survey shows the exposure of an sudden correction of the risk premia significantly differs across EU countries. In the event of a sudden correction in the risk premia, insurance undertakings and pension funds with ample exposure to bonds and real estate, could suffer significant asset value variations that could lead to forced asset sales and potentially amplify the original shock to asset prices in less liquid markets. Some juridictions, however, confirm the limited exposure to this risk due to the low holding of fixed income instruments and well diversified portfolios.

The survey further indicates that national authorities expect the increase of investments in alternative asset classes and more illiquid assets. Conversely, holdings of governement bonds are expected to decrease in favour of corporate bonds within the next 12 months. Overall this might indicate potential search for yield behaviour and a shift towards more illiquid assets continues throughout numerous EU jurisdictions. Property investments – through for instance mortgages and infrastructure investment – are also expected to increase in some jurisdictions, for both insurers and pension funds. A potential downturn of real estate markets could therefore also affect the soundness of the insurance and pension fund sectors.

QUANTITATIVE RISK ASSESSMENT EUROPEAN INSURANCE SECTOR

This section further assesses the key risks and vulnerabilities for the European insurance sector identified in this report. A detailed breakdown of the investment portfolio and asset allocation is provided with a focus on specific country exposures and interconnectedness with the banking sector. The chapter also analyses in more detail the implications of the current low yield environment for insurers.

INVESTMENTS

Insurance companies’ investments remain broadly stable, with a slight move towards less liquid investment. Government and corporate bonds continue to make up the majority of the investment portfolio, with only a slight movement towards more non-traditional investment instruments such as unlisted equity and mortgage and loans. Life insurers in particular rely on fixed-income assets, due to the importance of asset-liability matching of their long-term obligations. At the same time, the high shares of fixed-income investments could give rise to significant reinvestment risk in the current low yield environment, in case the maturing fixed-income securities can only be replaced by lower yielding fixed-income securities for the same credit quality.

The overall credit quality of the bond portfolio is broadly satisfactory, although slight changes are observed in 2018. The vast majority of bonds held by European insurers are investment grade, with most rated as CQS1 (AA). However, the share of CQS2 has increased in the first half of 2019, and significant differences can be observed for insurers across countries.

INTERCONNECTEDNESS BETWEEN INSURERS AND BANKS

The overall exposures towards the banking sector remain significant for insurers in certain countries, which could be one potential transmission channel in case of a sudden reassessment of risk premia. The interconnectedness between insurers and banks could intensify contagion across the financial system through common risk exposures. A potential sudden reassessment of risk premia may not only affect insurers directly, but also indirectly through exposures to the banking sector. This is also a potential transmission channel of emerging markets distress, as banks have on average larger exposures to emerging markets when compared to insurers.

Another channel of risk transmission could be through different types of bank instruments bundled together and credited by institutional investors such as insurers and pension funds.

Insurers’ exposures towards banks are heterogeneous across the EU/EEA countries, with different levels of home bias as well. Hence, countries with primary banks exposed to emerging markets or weak banking sectors could be impacted more in case of economic distress. On average, 15.95% of the EU/EEA insurers’ assets are issued by the banking sector through different types of instruments, mostly bank bonds.

Click here to access EIOPA’s Dec 2019 Financial Stability Report