In its work, EIOPA followed a step-by-step approach seeking to address the following questions in a sequential way:

- Does insurance create or amplify systemic risk?

- If yes, what are the tools already existing in the Solvency II framework, and how do they contribute to mitigate the sources of systemic risk?

- Are other tools needed and, if yes, which ones could be promoted?

Each paper published addresses one of the questions above. The publication of the three EIOPA papers on systemic risk and macroprudential policy in insurance has constituted an important milestone by which EIOPA has defined its policy stance and laid down its initial ideas on several relevant topics.

This work should now be turned into a specific policy proposal for additional macroprudential tools or measures where relevant and possible as part of the review of Directive 2009/138/EC (the ‘Solvency II5 Review’). For this purpose, and in order to gather the views of stakeholders, EIOPA is publishing this Discussion Paper on systemic risk and macroprudential policy in insurance, which focuses primarily on the third paper, i.e. on potential new tools and measures. Special attention is devoted to the four tools and measures specifically highlighted in the recent European Commission’s Call for Advice to EIOPA.

The financial crisis has shown the need to further consider the way in which systemic risk is created and/or amplified, as well as the need to have proper policies in place to address those risks. So far, most of the discussions on macroprudential policy have focused on the banking sector due to its prominent role in the recent financial crisis.

Given the relevance of the topic, EIOPA initiated the publication of a series of three papers on systemic risk and macroprudential policy in insurance with the aim of contributing to the debate and ensuring that any extension of this debate to the insurance sector reflects the specific nature of the insurance business.

EIOPA followed a step-by-step approach, seeking to address the following questions:

- Does insurance create or amplify systemic risk? In the first paper entitled ‘Systemic risk and macroprudential policy in insurance’, EIOPA identified and analysed the sources of systemic risk in insurance and proposed a specific macroprudential framework for the sector. If yes, what are the tools already existing in the current framework, and how do they contribute to mitigate the sources of systemic risk? In the second paper, ‘Solvency II tools with macroprudential impact’, EIOPA identified, classified and provided a preliminary assessment of the tools or measures already existing within the Solvency II framework, which could mitigate any of the systemic risk sources that were previously identified.

- Are other tools needed and, if yes, which ones could be promoted? The third paper carried out an initial assessment of other potential tools or measures to be included in a macroprudential framework designed for insurers. EIOPA focused on four categories of tools (capital and reservingbased tools, liquidity-based tools, exposure-based tools and pre-emptive planning). The paper focuses on whether a specific instrument should or should not be further considered. This is an important aspect in light of future work in the context of the Solvency II review.

The publication of the three EIOPA papers on systemic risk and macroprudential policy in insurance constitutes an important milestone by which EIOPA has defined its policy stance and laid down its initial ideas on several relevant topics. It should be noted that the ESRB (2018) has also identified a shortlist of options for additional provisions, measures and instruments, which reaches broadly similar conclusions as EIOPA.

EIOPA’s work should now be turned into a specific policy proposal for additional macroprudential tools or measures where relevant and possible as part of the Solvency II Review. For this purpose, and in order to gather the views of stakeholders, EIOPA is publishing this Discussion Paper on systemic risk and macroprudential policy in insurance.

This Discussion paper is based on the three papers previously published. They therefore back its content. Interested readers are recommended to consult them for further information or details. Relevant references are included in each of the sections.

EIOPA has included questions on all three papers. The majority of the questions, however, revolve around the third paper on additional tools or measures, which is more relevant in light of the Solvency II review.

The Discussion paper primarily focuses on the “principles” of each tool, trying to explain their rationale. As such, it does not address the operational aspects/challenges of each tool (e.g. calibration, thresholds, etc.) in a comprehensive manner. Similar to the approach followed with other legislative initiatives, the technical details could be addressed by means of technical standards, guidelines or recommendations, once the relevant legal instrument has been enacted.

Definitions

EIOPA provided all relevant definitions in EIOPA (2018a). It has to be noted, however, that there is usually no unique or universal definition for all these concepts. EIOPA’s work did not seek to fill this gap. Instead, working definitions are put forward in order to set the scene and should therefore be considered in the context of this paper only.

- Financial stability and systemic risk are two strongly related concepts. Financial stability can be defined as a state whereby the build-up of systemic risk is prevented.

- Systemic risk means a risk of disruption in the financial system with the potential to have serious negative consequences for the internal market and the real economy.

- Macroprudential policy should be understood as a framework that aims at mitigating systemic risk (or the build-up thereof), thereby contributing to the ultimate objective of the stability of the financial system and, as a result, the broader implications for economic growth.

- Macroprudential instruments are qualitative or quantitative tools or measures with system-wide impact that relevant competent authorities (i.e. authorities in charge of preserving the stability of the financial system) put in place with the aim of achieving financial stability.

In the context of this paper, these concepts (i.e. tools, instruments and measures) are used as synonyms.

The macroprudential policy approach contributes to the stability of the financial system — together with other policies (e.g. monetary and fiscal) as well as with microprudential policies. Whereas microprudential policies primarily focus on individual entities, the macroprudential approach focuses on the financial system as a whole.

It should be taken into account that, in some cases, the borders between microprudential policies and macroprudential consequences are blurring. That means, for example, that instruments that may have been designed as microprudential instrument may also have macroprudential consequences.

There are different institutional models for the implementation of macroprudential policies across EU, in some cases involving different parties (e.g. ministries, supervisors, etc.). This paper adopts a neutral approach by referring to the generic concept of the ‘relevant authority in charge of the macroprudential policy’, which should encompass the different institutional models existing across jurisdictions. Sometimes a simplified term such as ‘the authorities’ or ‘the competent authorities’ is used.

Systemic risk in insurance

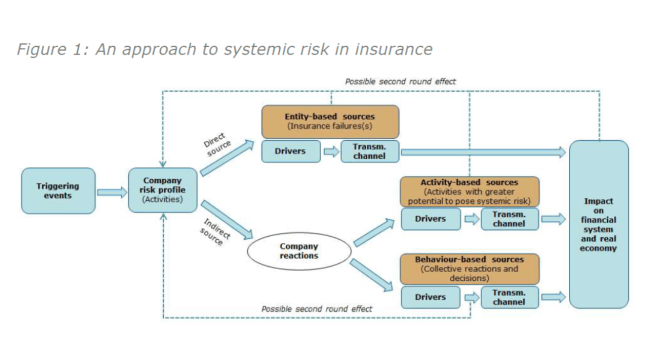

While a common understanding of the systemic relevance of the banking sector has been reached, the issue is still debated in the case of the insurance sector. In order to contribute to this debate, EIOPA developed a conceptual approach to illustrate the dynamics in which systemic risk in insurance can be created or amplified.

Main elements of EIOPA’s conceptual approach to systemic risk

- Triggering event: Exogenous event that has an impact on one or several insurance companies and may initiate the whole process of systemic risk creation. Examples are macroeconomic factors (e.g. raising unemployment), financial factors (e.g. yield movements) or non-financial factors (e.g. demographic changes or cyber-attacks).

- Company risk profile: The result of the collection of activities performed by the insurance company. The activities will determine: a) the specific features of the company reflecting the strategic and operational decisions taken; and b) the risk factors that the company is exposed to, i.e. the potential vulnerabilities of the company.

- Systemic risk drivers: Elements that may enable the generation of negative spill-overs from one or more company-specific stresses into a systemic effect, i.e. they may turn a company specific-stress into a system wide stress.

- Transmission channels. Contagion channels that explain the process by which the sources of systemic risk may affect financial stability and/or the real economy. EIOPA distinguishes five main transmission channels: a) Exposure channel; b) Asset liquidation channel; c) Lack of supply of insurance products; d) Bank-like channel; and e) Expectations and information asymmetries

- Sources of systemic risk: they result from the systemic risk drivers and their transmission channels. They are direct or indirect externalities whereby insurance imposes a systemic threat to the wider system. These direct and indirect externalities lead to three potential sources’ categories of systemic risks which are not mutually exclusive, i.e. entity-based related source, activity-based related source and behaviour-based related source.

In essence and as depicted in Figure 1, the approach developed by EIOPA considers that a ‘triggering event’ initially has an impact at entity level, affecting one or more insurers through their ‘risk profile’. Potential individual or collective distresses may generate systemic implications, the relevance of which is determined by the presence of different ‘systemic risk drivers’ embedded in the insurance companies.

In EIOPA’s view, systemic events could be generated in two ways.

- The ‘direct’ effect, originated by the failure of a systemically relevant insurer or the collective failure of several insurers generating a cascade effect. This systemic source is defined as ‘entity-based’.

- The ‘indirect’ effect, in which possible externalities are enhanced by engagement in potentially systemic activities (activity-based sources) or the widespread common reactions of insurers to exogenous shocks (behaviour-based source).

Potential externalities generated via direct and indirect sources are transferred to the rest of the financial system and to the real economy via specific channels (i.e. the transmission channel) and could induce changes in the risk profile of insurers, eventually generating potential second-round effects.

The following table provides an overview of possible examples of triggering events, risk profile, systemic risk drivers and transmission channels. It should therefore not be considered as a comprehensive list of elements.

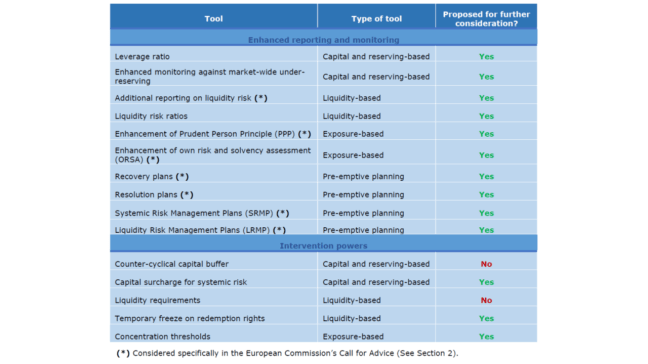

Potential macroprudential tools and measures to enhance the current framework

In its third paper, EIOPA (2018c) carried out an analysis focusing on four categories of tools:

a) Capital and reserving-based tools;

b) Liquidity-based tools;

c) Exposure-based tools; and

d) Pre-emptive planning.

EIOPA also considers whether the tools should be used for enhanced reporting and monitoring or as intervention power. Following this preliminary analysis, EIOPA concluded the following :

Example: Enhancement of the ORSA

Description. In an ORSA, an insurer is required to consider all material risks that may have an impact on its ability to meet its obligations to policyholders. In doing this a forward looking perspective is also required. Although conceived at first as a microprudential tool, this tool could be enhanced to take the macroprudential perspective also into account.

Potential contribution to mitigate systemic risk. The enhancement of ORSA could help in mitigating two of the sources of systemic risk identified.

Proposal. This measure is proposed for further consideration for enhanced reporting and monitoring purposes.

Operational aspects. A description of all relevant operational aspects is carried out in EIOPA (2018c). In essence, the idea is to supplement the microprudential approach by assigning certain roles and responsibilities to the relevant authority in charge of the macroprudential policy (see Figure below). This authority could carry out three different tasks:

- Aggregation of information;

- Analysis of the information; and

- Provision of certain information or parameters to supervisors to channel macroprudential concerns.

Supervisors would then request undertakings to include in their ORSAs particular macroprudential risks.

Issues for consideration: In order to make the ORSA operational from a macroprudential point of view, the following would be needed:

- A clarification of the role of the risk management function in order to include macroprudential concerns.

- The inclusion of a new paragraph in Article 45 of the Solvency II directive explicitly referring to the macroprudential dimension and the need to consider the macroeconomic situation and potential sources of systemic risk as followup of their assessment on whether the company complies on a continuous basis with the Solvency II regulatory capital requirements.

- Clarification that a follow-up is expected after input from supervisors, namely from authorities in charge of the macroprudential policy. On a risk-based approach this might imply the request of specific information in terms of nature, scope, format and point in time, where justified by likelihood or impact of materialisation of a certain source of systemic risk.

Furthermore, a certain level of harmonisation of the structure and content of the ORSA report would be needed, which would enable the identification of the relevant sections by the authorities in charge of macroprudential policies. This, however, would mean a change in the current approach followed with regard to the ORSA.

Click here to access EIOPA’s detailed Discussion Paper 2019