Financial institutions are acutely aware that cyber risk is one of the most significant perils they face and one of the most challenging to manage. The perceived intensity of the threats, and Board level concern about the effectiveness of defensive measures, ramp up continually as bad actors increase the sophistication, number, and frequency of their attacks.

Cyber risk management is high on or at the top of the agenda for financial institutions across the sector globally. Highly visible attacks of increasing insidiousness and sophistication are headline news on an almost daily basis. The line between criminal and political bad actors is increasingly blurred with each faction learning from the other. In addition, with cyberattack tools and techniques becoming more available via the dark web and other sources, the population of attackers continues to increase, with recent estimates putting the number of cyberattackers globally in the hundreds of thousands.

Cyber offenses against banks, clearers, insurers, and other major financial services sector participants will not abate any time soon. Looking at the velocity and frequency of attacks, the motivation for cyberattack upon financial services institutions can be several hundred times higher than for non-financial services organizations.

Observing these developments, regulators are prescribing increasingly stringent requirements for cyber risk management. New and emerging regulation will force changes on many fronts and will compel firms to demonstrate that they are taking cyber seriously in all that they do. However, compliance with these regulations will only be one step towards assuring effective governance and control of institutions’ Cyber Risk.

We explore the underlying challenges with regard to cyber risk management and analyze the nature of increasingly stringent regulatory demands. Putting these pieces together, we frame five strategic moves which we believe will enable businesses to satisfy business needs, their fiduciary responsibilities with regard to cyber risk, and regulatory requirements:

- Seek to quantify cyber risk in terms of capital and earnings at risk.

- Anchor all cyber risk governance through risk appetite.

- Ensure effectiveness of independent cyber risk oversight using specialized skills.

- Comprehensively map and test controls, especially for third-party interactions.

- Develop and exercise major incident management playbooks.

These points are consistent with global trends for cyber risk management. Further, we believe that our observations on industry challenges and the steps we recommend to address them are applicable across geographies, especially when considering prioritization of cyber risk investments.

FIVE STRATEGIC MOVES

The current environment poses major challenges for Boards and management. Leadership has to fully understand the cyber risk profile the organization faces to simultaneously protect the institution against everchanging threats and be on the front foot with regard to increasing regulatory pressures, while prioritizing the deployment of scarce resources. This is especially important given that regulation is still maturing and it is not yet clear how high the compliance bars will be set and what resources will need to be committed to achieve passing grades.

With this in mind, we propose five strategic moves which we believe, based on our experience, will help institutions position themselves well to address existing cyber risk management challenges.

1) Seek to quantify cyber risk in terms of capital and earnings at risk

Boards of Directors and all levels of management intuitively relate to risks that are quantified in economic terms. Explaining any type of risk, opportunity, or tradeoff relative to the bottom line brings sharper focus to the debate.

For all financial and many non-financial risks, institutions have developed methods for quantifying expected and unexpected losses in dollar terms that can readily be compared to earnings and capital. Further, regulators have expected this as a component of regulatory and economic capital, CCAR, and/or resolution and recovery planning. Predicting losses due to Cyber is particularly difficult because it consists of a combination of direct, indirect, and reputational elements which are not easy to quantify. In addition, there is limited historical cyber loss exposure data available to support robust cyber risk quantification.

Nevertheless, institutions still need to develop a view of their financial exposures of cyber risk with different levels of confidence and understand how this varies by business line, process, or platform. In some cases, these views may be more expert based, using scenario analysis approaches as opposed to raw statistical modeling outputs. The objectives are still the same – to challenge perspectives as to

- how much risk exposure exists,

- how it could manifest within the organization,

- and how specific response strategies are reducing the institution’s inherent cyber risk.

2) Anchor all cyber risk governance through risk appetite

Regulators are specifically insisting on the establishment of a cyber risk strategy, which is typically shaped by a cyber risk appetite. This should represent an effective governance anchor to help address the Board’s concerns about whether appropriate risks are being considered and managed effectively.

Setting a risk appetite enables the Board and senior management to more deeply understand exposure to specific cyber risks, establish clarity on the Cyber imperatives for the organization, work out tradeoffs, and determine priorities.

Considering cyber risk in this way also enables it to be brought into a common framework with all other risks and provides a starting point to discuss whether the exposure is affordable (given capital and earnings) and strategically acceptable.

Cyber risk appetite should be cascaded down through the organization and provide a coherent management and monitoring framework consisting of

- metrics,

- assessments,

- and practical tests or exercises

at multiple levels of granularity. Such cascading establishes a relatable chain of information at each management level across business lines and functions. Each management layer can hold the next layer more specifically accountable. Parallel business units and operations can have common standards for comparing results and sharing best practices.

Finally, Second and Third Line can have focal points to review and assure compliance. A risk appetite chain further provides a means for the attestation of the effectiveness of controls and adherence to governance directives and standards.

Where it can be demonstrated that risk appetite is being upheld to procedural levels, management will be more confident in providing the attestations that regulators require.

3) Ensure effectiveness of independent cyber risk oversight using specialized skills

From our perspective, firms face challenges when attempting to practically fit cyber risk management into a “Three Lines of Defense” model and align cyber risk holistically within an enterprise risk management framework.

CROs and risk management functions have traditionally developed specialized skills for many risk types, but often have not evolved as much depth on IT and cyber risks. Organizations have overcome this challenge by weaving risk management into the IT organization as a First Line function.

In order to more clearly segregate the roles between IT, business, and Information Security (IS), the Chief Information Security Officer (CISO) and the IS team will typically need to be positioned as a « 1.5 Line of Defense » position. This allows an Information Security group to provide more formal oversight and guidance on the cyber requirements and to monitor day-today compliance across business and technology teams.

Further independent risk oversight and audit is clearly needed as part of the Third Line of Defense. Defining what oversight and audit means becomes more traceable and tractable when specific governance mandates and metrics from the Board down are established.

Institutions will also need to deal with the practical challenge of building and maintaining Cyber talent that can understand the business imperatives, compliance requirements, and associated cyber risk exposures.

At the leadership level, some organizations have introduced the concept of a Risk Technology Officer who interfaces with the CISO and is responsible for integration of cyber risk with operational risk.

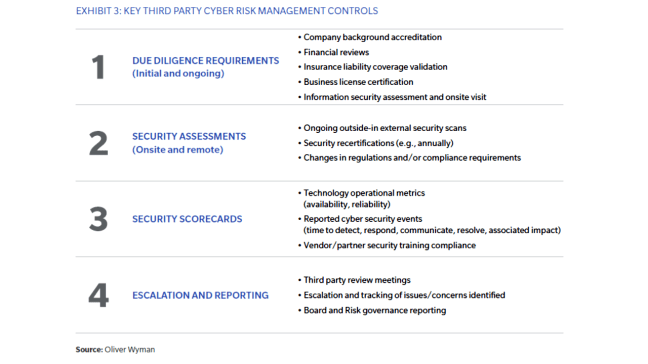

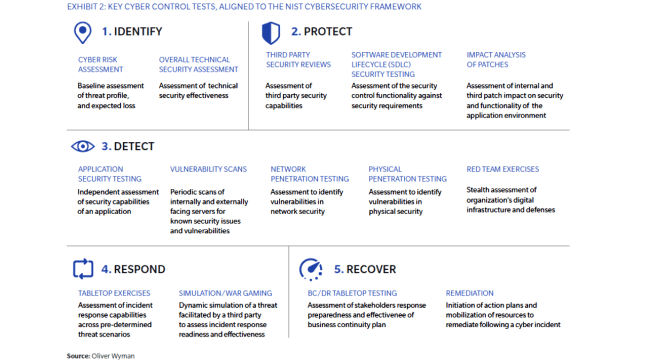

4) Comprehensively map and test controls, especially for the third party interactions

Institutions need to undertake more rigorous and more frequent assessments of cyber risks across operations, technology, and people. These assessments need to test

- the efficacy of surveillance,

- the effectiveness of protection and defensive controls,

- the responsiveness of the organization,

- and the ability to recover

in a manner consistent with expectations of the Board.

Given the new and emerging regulatory requirements, firms will need to pay closer attention to the ongoing assessment and management of third parties. Third parties need to be tiered based on their access and interaction with the institution’s high value assets. Through this assessment of process, institutions need to obtain a more practical understanding of their ability to get early warning signals against cyber threats. In a number of cases, a firm may choose to outsource more IT or data services to third party providers (e.g., Cloud) where they consider that this option represents a more attractive and acceptable solution relative to the cost or talent demands associated with maintaining Information Security in-house for certain capabilities. At the same time, the risk of third party compromise needs to be fully understood with respect to the overall risk appetite.

5) Develop and exercise incident management playbooks

A critical test of an institution’s cyber risk readiness is its ability to quickly and effectively respond when a cyberattack occurs.

As part of raising the bar on cyber resilience, institutions need to ensure that they have clearly documented and proven cyber incident response plans that include

- a comprehensive array of attack scenarios,

- clear identification of accountabilities across the organization,

- response strategies,

- and associated internal and external communication scenarios.

Institutions need to thoroughly test their incident response plan on an ongoing basis via table top exercises and practical drills. As part of a table top exercise, key stakeholders walk through specific attack scenarios to test their knowledge of response strategies. This exercise provides an avenue for exposing key stakeholders to more tangible aspects of cyber risk and their respective roles in the event of a cyberattack. It also can reveal gaps in specific response processes, roles, and communications that the institution will need to address.

Last but not least, incident management plans need to be reviewed and refined based on changes in the overall threat landscape and an assessment of the institution’s cyber threat profile; on a yearly or more frequent basis depending on the nature and volatility of the risk for a given business line or platform.

CONCLUSION

Cyber adversaries are increasingly sophisticated, innovative, organized, and relentless in developing new and nefarious ways to attack institutions. Cyber risk represents a relatively new class of risk which brings with it the need to grasp the often complex technological aspects, social engineering factors, and changing nature of Operational Risk as a consequence of cyber.

Leadership has to understand the threat landscape and be fully prepared to address the associated challenges. It would be impractical to have zero tolerance to cyber risk, so institutions will need to determine their risk appetite with regard to cyber, and consequently, make direct governance, investment, and operational design decisions.

The new and emerging regulations are a clear directive to financial institutions to keep cyber risk at the center of their enterprise-wide business strategy, raising the overall bar for cyber resilience. The associated directives and requirements across the many regulatory bodies represent a good and often strong basis for cyber management practices but each institution will need to further ensure that they are tackling cyber risk in a manner fully aligned with the risk management strategy and principles of their firm. In this context, we believe the five moves represent multiple strategically important advances almost all financial services firms will need to make to meet business security, resiliency, and regulatory requirements.

click here to access mmc’s cyber handbook