If implementation of the forthcoming insurance contracts standard is to reach the best possible outcome for your organization, we believe it needs to be seen as more than just a compliance exercise. This will entail

- combining multiple strands into a common program,

- identifying linkages

- and addressing dependencies

across the business in a logical sequence and thinking strategically about possible effects on the organization and its stakeholders. A well-developed and ‘living’ plan assigns clear accountabilities and breaks down objectives into manageable tasks for delivery to realistic time-scales in order to establish an effective blue-print for success.

Our methodology groups activities into four manageable phases:

- assess the change

- design your response

- implement your design

- sustain your new practices, securely embedding them in business as usual.

Key success factors

Our experience shows us there are many factors that will contribute to successfully implementing insurance accounting change, including:

- Dedicated staff: In our experience the single biggest factor contributing to program success is the presence of full-time staff dedicated to the project, with a wide range of skills including data management, IT implementation and project management and who know your business.

- Spend sufficient time and energy on the initial impact phase: It is essential that an insurer plans for this critical phase and allows for sufficient time to perform a gap analysis on a line-by-line basis through the income statement and balance sheet and supports disclosures.

- Consider fundamental questions surrounding core business drivers: earnings trends, growth opportunities and target operating models. The earlier effects are identified, the more time an insurer will have to develop and implement a strategic response.

- Training staff: Many organizations underestimate the amount of personnel training required. Designing a comprehensive training strategy and program is highly complex and requires careful planning.

- Robust project planning: The plan must be achievable and continuously refined with formal tracking and monitoring.

- Clear communications: Communication needs to be both formal and informal and applied throughout the life of the program.

- Careful change management: IFRS conversion will lead to significant changes in how people do their jobs. Some of the biggest challenges have arisen when the cultural issues have not been acknowledged and addressed.

- More than just an accounting and actuarial project: Implementing the forthcoming insurance contracts project will undoubtedly be a multi-disciplinary effort.

- IT specialists consider the functionality of source systems and enterprise performance management (EPM) systems;

- Change management specialists focus on behavioral change and communication;

- specialists in commercial functions (tax, data management, executive incentives, etc.) bring a holistic approach to the program.

Robust project management helps to bring everything together coherently.

Assessing what the forthcoming standard will mean for you

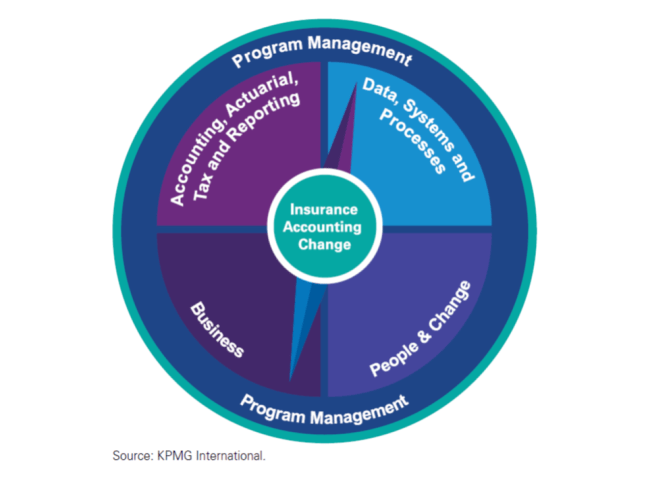

Accounting, actuarial, tax and reporting

Q1. What are the key accounting, actuarial, tax and disclosure differences between our current generally accepted accounting principles (GAAP) and the new standards? What are the key decisions that need to be made by management regarding the alternative treatments that are available?

Data, systems and processes

Q2. What will the impact be for our data requirements, and on the systems and processes used for

- data collection,

- actuarial projections,

- calculating and accruing interest on the contractual service margin

- and consolidation and financial reporting systems?

Are there quick fixes that we can use? Can we leverage recent investments in infrastructure or will we need a major overhaul?

Q3. How will the group‘s close and other processes be impacted?

Business

Q4. What is the estimated directional impact on profit and equity and what are the key decisions and judgments that this will influence?

Q5. What are the key impacts for my business and how will these be influenced by the choices open to us? Who will need to understand results and metrics on the new basis?

People and change management

Q6. Who will be impacted by the conversion, what skills and resources are likely to be needed and what training needs can we identify?

Program management

Q7. What would a high-level conversion plan look like and what is its likely impact on resources?