Risks originating from the macroeconomic environment remained at a high level in Q4 2017, although most indicators improved slightly comparing with Q3. Positive developments in forecasted real GDP growth and increased expected inflation closer towards the ECB target contributed somewhat to a decrease in risk, as well as a slight reduction in the accommodative stance of monetary policy. Swap rates recently increased but remained low by historical standards. The credit-to-GDP gap was the only indicator to deteriorate since the previous assessment, moving further into negative territory.

Credit risks remain constant at a medium level in Q4 2017. Since the last assessment spreads have decreased across all bond segments, except for unsecured financial corporate bonds. Concerns about potential credit risk mispricing remain.

Market risks were stable at a medium level in Q4 2017. Most market indicators changed only little when compared to the previous risk assessment, except for investments in equity. Volatility of equity prices increased, with a temporary peak in February. A slight decline was reported for the price-to-book value ratio (PBV). In addition, Q4 Solvency II data seems to indicate a slight increase in median exposures to bonds and property and an increase of exposures to equity for insurers in the upper tail of the distribution.

Liquidity and funding risks remained constant at a medium level in Q4 2017, with most indicators pointing to a stable risk exposure.

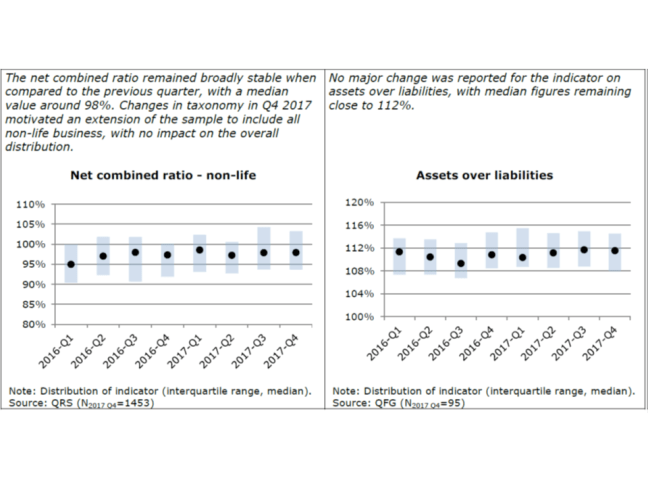

Profitability and solvency risks remained stable at a medium level in Q4 2017. Annual figures for some profitability indicators show a slight deterioration when compared to annualised Q2 indicators, but are broadly at the same level as in Q4 2016. Solvency ratios remain well above 100% for most insurers in the sample. A slight increase in the quality of own funds has also been observed.

Risks related to interlinkages and imbalances remain stable at a medium level in Q4 2017. Main observed developments relate to a slight decrease in median exposures to domestic sovereign debt and to a mild increase in the share of premiums ceded to reinsurers. Investment exposures to banks, insurers and other financial institutions remained broadly unchanged.

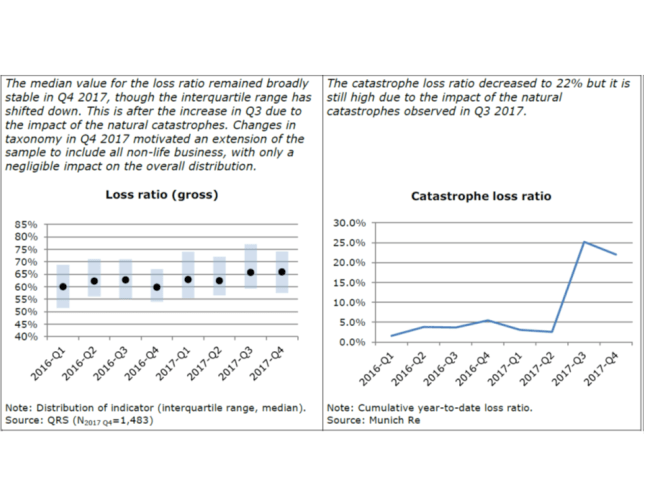

Insurance risks remained stable at a medium level when compared to Q3 2017. The impact of the catastrophic events observed in Q3 on insurers’ technical results still weights on the risk assessment.

Market perceptions remained stable at a medium level since the last assessment. Positive developments related to the performance of insurers’ stock prices relative to the overall market and a decrease in the upper tail of the distribution of price-to-earnings ratios contributed to decreased risk, but this was partially compensated by a deterioration of some insurers’ external rating outlooks. Other indicators, such as insurers’ CDS spreads and external ratings remained largely unchanged.

Summary

Click here to access EIOPA’s detailed Risk Dashboard – April 2018