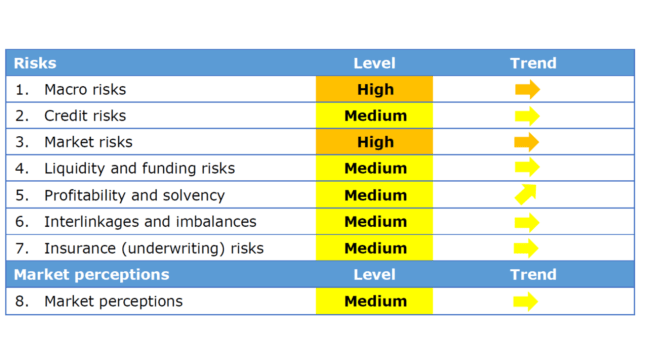

Risk exposures for the European insurance sector remain overall stable.

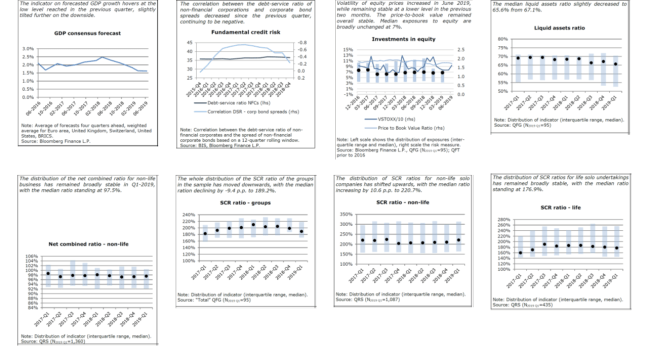

Macro and market risks are now at a high level due to a further decline in swap rates and lower returns on investments in 2018 which put strain on those life insurers offering guaranteed rates. The low interest rate environment remains a key risk for the insurance sector.

Credit risks continue at medium level with broadly stable CDS spreads for government and corporate bonds.

Profitability and solvency risks increased due to lower return on investments for life insurers observed in year-end 2018 data; SCR ratios are above 100% for most undertakings in the sample even when excluding the impact of the transitional measures.

Market perceptions were marked by a performance of insurers’ stocks broadly in line with overall equity markets, while median CDS spreads have slightly increased. No change was observed in insurers’ external ratings and rating outlooks.

Macro risks are now at a high level. Since the April 2019 assessment, swap rates have further declined for all the currencies considered (EUR, GBP, CHF, USD). The indicator on credit-to-GDP gaps has deteriorated due to a more negative gap in the Euro area. Key policy rates remained unchanged and the rate of expansion of major central banks’ (CB) balance sheets is now close to zero. Recent monetary policy decisions suggest that some degree of monetary accomodation is still to be expected for the forseeable future.

Credit risks remained stable at medium level. Since the previous assessment, spreads have remained broadly stable for all corporate bond segments except financials (unsecured). The average credit quality of insurers’ investments remained broadly stable, corresponding to an S&P rating between AA and A, while the share of below investment grade assets remains limited.

Market risks are now at a high level. Volatility of the largest asset class, bonds, remained broadly stable compared to the January’s assessment, whereas equity market volatility spiked in June 2019. Newly available annual information shows a decline in the spread of investment returns over the guaranteed rates to negative values in 2018, mainly due to lower investment returns. The mismatch between the duration of assets and liabilities remained broadly stable in the same period.

Liquidity and funding risks remained stable at medium level. Liquidity indicators have remained broadly unchanged since the previous quarter, while funding indicators such as the average ratio of coupons to maturity and the average multiplier for catastrophe bond issuance increased.

Profitability and solvency risks remain at medium level but show an increasing trend. This is mainly due to newly available data on the return on investments for life solo undertakings, which was considerably lower in 2018 than in the preceding year. SCR ratios are above 100% for the majority of insurers in the sample even when excluding the impact of the transitional measures on technical provisions and interest rates. The proportion of Tier 1 capital in total own funds remains high across the whole distribution and the share of expected profit in future premiums in eligible own funds is below 15% for most undertakings in the sample.

Interlinkages and imbalances risks remained at medium level in Q1-2019. A minor increase is observed for exposures to banks, while the opposite is true for exposures to other financial institutions. An increase has been reported in the share of premiums ceded to reinsurers.

Insurance risks remained constant at a medium level. Median premium growth of life and non-life business remains positive and a reduction has been reported in insurance groups’ loss ratios and cat loss ratios.

Market perceptions remained constant at medium level. Insurance groups stocks’ performance was broadly in line with the overall market. Median insurers’ CDS spreads have increased, while external ratings have remained unchanged.

Click here to access EIOPA’s Risk Dashboard July 2019