Introduction

During the course of 2018, EIOPA carried out a European-wide stress test (ST) in accordance with Articles 21(2)(b) and 32 of Regulation (EU) 1094/2010 of 24 November 2010 of the European Parliament and of the Council (hereafter the ‘Regulation’).

The Recommendations contained in this document are issued in accordance with Article 21(2)(b) of the Regulation in order to address issues identified in the stress test.

EIOPA will support National Competent Authorities (NCAs) and undertakings through guidance and other measures if needed.

The 2018 Stress Test results showed that on aggregate the insurance sector is sufficiently capitalised to absorb the combination of shocks prescribed in the three scenarios. However, it also confirms the significant sensitivity to market shocks for the European insurance sector with Groups being vulnerable

- not only to low yields and longevity risk,

- but also to a sudden and abrupt reversal of risk premia, combined with an instantaneous shock to lapse rates and claims inflation.

The exercise further reveals potential transmission channels of the tested shocks to insurers’ balance sheets. For instance, in the YCU scenario the assumed claim inflation shock leads to a net increase in the liabilities of those Groups more exposed to non-life business through claims inflation. Finally, both the YCD and YCU scenario have similar negative impact on post-stress SCR ratios.

As outlined in the Executive Summary of the 2018 Insurance Stress Test Report, further analyses of the results are required by EIOPA and the NCAs to obtain a deeper understanding of the risks and vulnerabilities of the sector.

In order to follow-up on the main vulnerabilities, EIOPA is issuing the present Recommendations related to the 2018 stress test exercise.

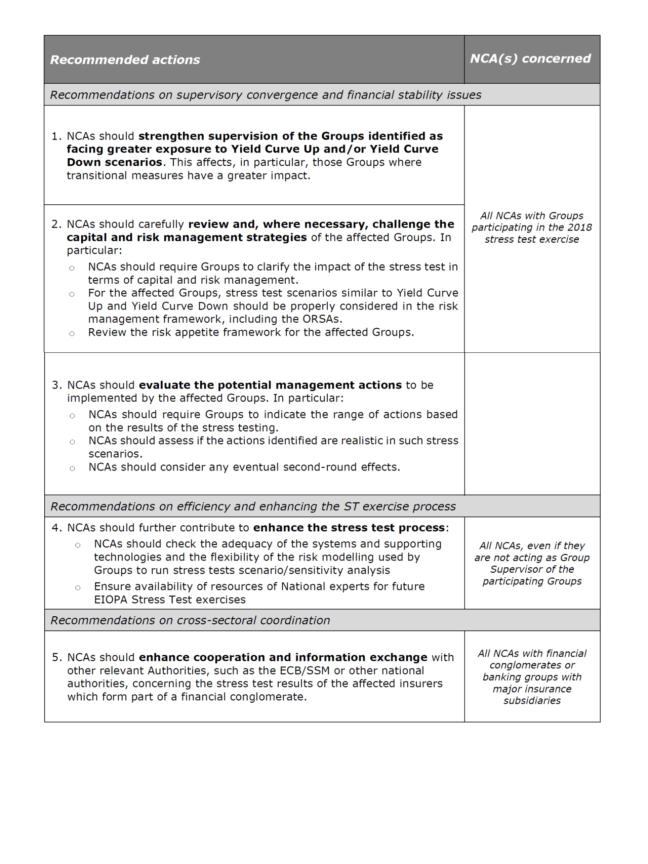

Recommendation 1

NCAs should strengthen the supervision of the Groups identified as facing greater exposure to Yield Curve Up and/or Yield Curve Down scenarios. This affects, in particular, those Groups where transitional measures have a greater impact.

Recommendation 2

NCAs should carefully review and, where necessary, challenge the capital and risk management strategies of the affected Groups. In particular:

- NCAs should require Groups to clarify the impact of the stress test in terms of capital and risk management.

- For the affected Groups, stress test scenarios similar to YCU and YCD should be properly considered in the risk management framework, including the ORSAs.

- Review the risk appetite framework for the affected Groups.

Recommendation 3

NCAs should evaluate the potential management actions to be implemented by the affected Groups. In particular:

- NCAs should require Groups to indicate the range of actions based on the results of the stress testing.

- NCAs should assess if the actions identified are realistic in such stress scenarios.

- NCAs should consider any eventual second-round effects.

Recommendation 4

NCAs should further contribute to enhance the stress test process.

Recommendation 5

NCAs should enhance cooperation and information exchange with other relevant Authorities, such as the ECB/SSM or other national authorities, concerning the stress test results of the affected insurers which form part of a financial conglomerate.