How the Distinct Roles of Internal Audit and the Finance Function Drive Good Governance

Effective governance involves many individuals and departments throughout an organization, including the Board of Directors, executive management, finance, and internal audit, among others. Yet each of these groups has a different set of skills and responsibilities. To successfully identify and manage risk, they must come together to create and maintain a sound system of corporate governance.

The insights shared here by 11 governance experts offer important perspective as to how finance and internal audit collaborate to support corporate governance, despite their distinct and separate missions.

Interviewees provided perceptions and experiences and shared best practices, as well as challenges, that they have encountered on their quest to achieve effective governance. These contributors come from organizations around the world that differ in size, industry, and management configurations. Several experienced governance from within both the finance function and internal audit.

A few shared perceptions include:

- The Board of Directors is responsible for setting the proper tone for the organization;

- It is critical to purposefully develop a consistent culture throughout the organization, driven by the CEO and senior management; and

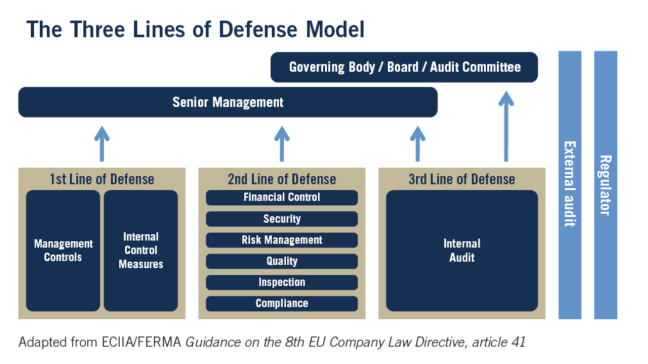

- Communication and coordination across complementary functions is vital.

Keys To Achieving Good Governance

There are many different definitions of governance. According to The Institute of Internal Auditors (hereafter The IIA), governance is “the combination of processes and structures implemented by the board in order to inform, direct, manage and monitor the activities of the organization toward the achievement of its objectives.”

The International Federation of Accountants (hereafter IFAC) uses a slightly different definition which focuses more on the creation of strategic objectives and stakeholder value, “Governance is to create and optimize sustainable organizational success and stakeholder value, balancing the interests of the various stakeholders. It comprises arrangements put in place to ensure that organizations define and achieve intended outcomes.”

Both definitions suggest that good governance and the achievement of organizational success are not the responsibility of the Board alone, but rather the outcome of a mosaic of organizational policies, processes, and cross-functional interactions.

When asked to provide the key objectives of governance, interviewees shared a number of different perspectives. Most frequently, good governance was defined as representing the interests of stakeholders by setting appropriate objectives and driving a culture that supports them.