Who Benefits from Modularization?

With technology moving forward at an unprecedented pace, incumbents are increasingly electing to outsource functions to highly specialized new entrants, renting evolving modules of technology that can be tailored to suit their individual needs. Though this approach may be more cost effective, it further fuels the question of whether incumbents will allow value in the industry to shift towards new entrants. In time, market participants will come to understand which module in the chain generates the most value. It is plausible that automation in distribution will shift value towards efficiency of internal processes that support cutting-edge modeling and underwriting engines.

The State of InsurTech

InsurTech funding volume increased 36% year-over-year in 2017, demonstrating that technology driven innovation remains a core focus area for (re)insurance companies and investors heading into 2018. However, perhaps contrary to many of the opinions championed in editorial and press coverage of the InsurTech sector, further analysis of the growing number of start-ups successfully attracting capital from (re)insurers and financial investors reveals that the majority of InsurTech ventures are not focused on exiling incumbents by disrupting the pressured insurance value chain. According to research from McKinsey & Company,

- 61% of InsurTech companies aim to enable the value chain,

- 30% are attempting to disintermediate incumbents from customers

- 9% are targeting full scale value chain disruption.

Has the hype surrounding InsurTech fostered unjustified fear from overly defensive incumbents?

We have taken this analysis a step further by tracking funding volume from strategic (re)insurers versus financial investors for InsurTechs focused on enabling the value chain relative to their counterparts attempting to disintermediate customers from incumbents or disrupt the value chain altogether and found that 65% of strategic (re)insurer InsurTech investments have been concentrated in companies enabling the value chain, with only 35% of incumbent investments going to start-ups with more disruptive business models. What does it mean? While recognizing the subjective nature of surmising an early stage company’s ultimate industry application at maturity from its initial focus, we attribute this phenomenon to the tendency of incumbents to, consciously or subconsciously, encourage development of less perceptibly threatening innovation while avoiding more radical, potentially intimidating technologies and applications.

Recognizing that this behavior may allow incumbents to preserve a palatable status quo, it should be considered in the context in which individual investments are evaluated – on the basis of expected benefits relative to potential risk. We have listed several benefits that InsurTechs offer to incumbents :

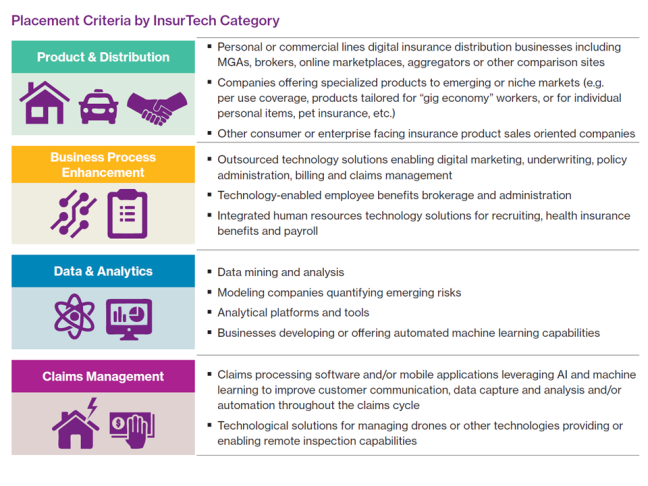

Segmenting the InsurTech Universe

As InsurTech start-ups continue to emerge across the various components of the insurance value chain and business lines, incumbents and investors are evaluating opportunities to deploy these applications in the insurance industry today and in the future. To simplify the process of identifying useful and potentially transformational technologies and applications, we have endeavored to segment the increasingly broad universe of InsurTech companies by their core function into four categories:

- Product & Distribution

- Business Process Enhancement

- Data & Analytics

- Claims Management

This exercise is complicated by the tendency of companies to operate across multiple functions, so significant professional judgment was used in determining the assignment for each company. A summary of the criteria used to determine placement is listed below. On the following pages, we have included market maps to provide a high level perspective of the number of players in each category, as well as a competitive assessment of each subsector and our expectations for each market going forward. Selected companies in each category, ranked by the amount of funding they have raised to date, are listed, followed by more detailed overviews and Q&A with selected representative companies from each subsector.