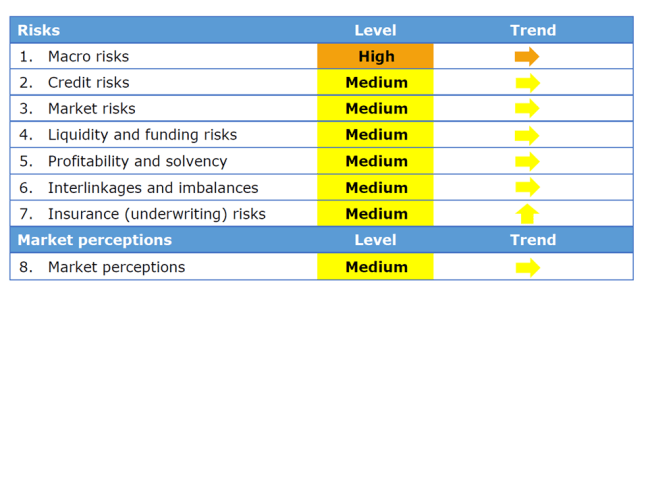

Risks originating from the macroeconomic environment remained stable and high. Improvements have been observed across most indicators, but were not sufficient to change the overall risk picture. The improving prospects for economic growth still contrast with the persistence of structural imbalances, such as fiscal deficit. The accommodative stance of monetary policy has been reduced only very gradually, with low interest rates continuing to put a strain on the insurance sector.

Credit risks remained constant at a medium level whereas observed spreads continued to decline. The average rating of investments has seen some marginal improvements. Concerns on the pricing of the risk premia remain.

Market risks remained stable at a medium level despite a reduction of the volatility on prices was observed. Only price to book value of European stocks moved in the direction of risk increase.

Liquidity and funding risks were constant at a medium level in 2017 Q3 and remained a minor issue for insurers. Catastrophe bond issuance significantly decreased when compared to the record high registered during the previous quarter. The low volume of issued bonds made the indicator less relevant.

Profitability and solvency risks remained stable at a medium level. A deterioration of the net combined ratio was observed in the tail (90 percentile) of the distribution mainly populated by reinsurers in this quarter. SCR ratios have improved across all types of insurers mainly due to an increase of the Eligible Own Funds. This has been especially marked for life solo companies.

Interlinkages & imbalances: Risks in this category remained constant at a medium level. Investment exposures to banks and other insurers increased slightly from the previous quarter.

Insurance risks increased when compared to 2017 Q2 and are now at a medium level. This was essentially driven by the significant increase in the catastrophe loss ratio resulting from the impact of the catastrophic events observed in Q3 mainly on reinsurers’ technical results. This is also reflected in the loss ratio. Other indicators in this risk category still point to a stable risk exposure.

Market perceptions remained constant, with the improvement in external rating outlooks outweighing the observed increase in price to earnings ratios. Insurance stocks slightly outperformed the market, especially for life insurance, and CDS spreads reduced.