The evolution of financial technology (FinTech) is reshaping the broader financial services industry. Technology is now disrupting the traditionally more conservative insurance industry, as the rise of InsurTech revolutionises how we think about insurance distribution.

Moreover, insurance companies are improving their operating models, upgrading their propositions, and developing innovative new products to reshape the insurance industry as a whole.

Five key technologies are driving the change today:

- Cloud computing

- The Internet of Things (including telematics)

- Big data

- Artificial intelligence

- Blockchain

This report examines these technologies’ potential to create value in the insurance industry. It also examines how technology providers could create new income streams and take advantage of economies of scale by offering their technological backbones to participants in the insurance industry and beyond.

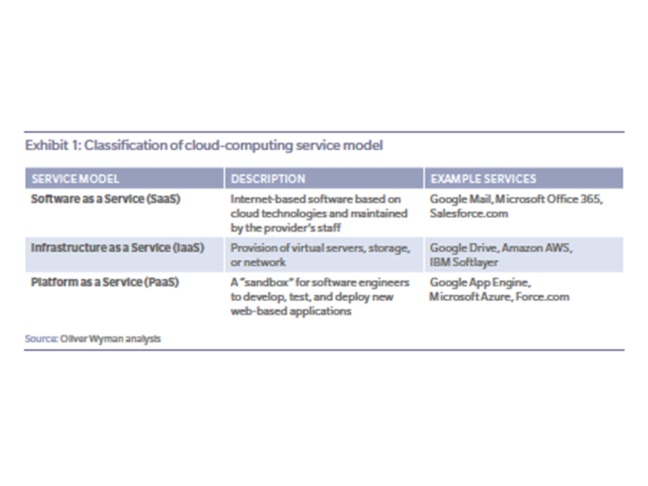

Cloud computing refers to storing, managing, and processing data via a network of remote servers, instead of locally on a server or personal computer. Key enablers of cloud computing include the availability of high-capacity networks and service-oriented architecture. The three core characteristics of a cloud service are:

- Virtualisation: The service is based on hardware that has been virtualised

- Scalability: The service can scale on demand, with additional capacity brought online within minutes

- Demand-driven: The client pays for the services as and when they are needed

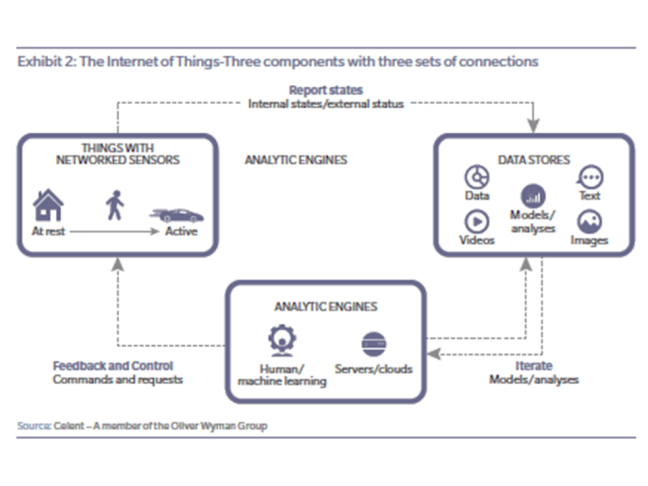

Telematics is the most common form of the broader Internet of Things (IoT). The IoT refers to the combination of physical devices, vehicles, buildings and other items embedded with electronics, software, sensors, actuators, and network connectivity that enable these physical objects to collect and exchange data.

The IoT has evolved from the convergence of

- wireless technologies,

- micro-electromechanical systems,

- and the Internet.

This convergence has helped remove the walls between operational technology and information technology, allowing unstructured, machine-generated data to be analysed for insights that will drive improvements.

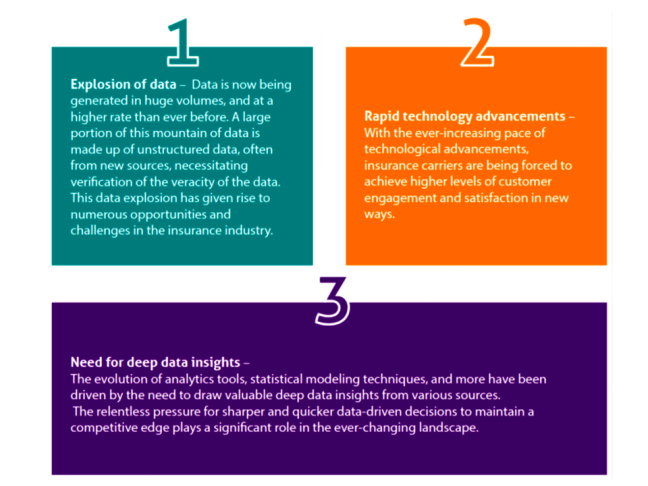

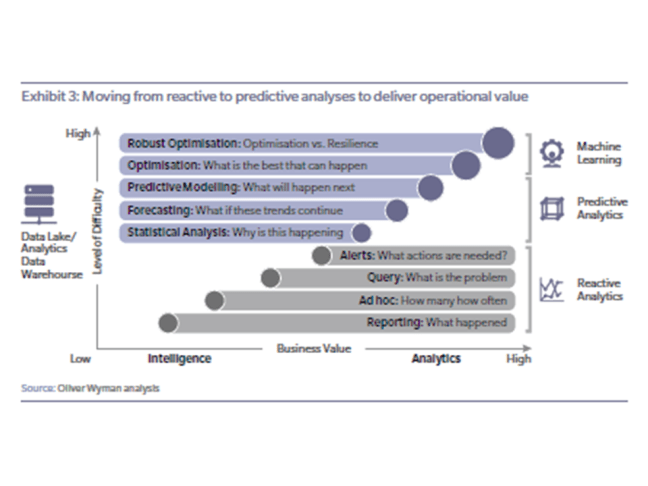

Big data refers to data sets that are so large or complex that traditional data processing application software is insufficient to deal with them. A definition refers to the “five V” key challenges for big data in insurance:

- Volume: As sensors cost less, the amount of information gathered will soon be measured

in exabytes

- Velocity: The speed at which data is collected, analysed, and presented to users

- Variety: Data can take many forms, such as structured, unstructured, text or multimedia. It can come from internal and external systems and sources, including a variety

of devices

- Value: Information provided by data about aspects of the insurance business, such as customers and risks

- Veracity: Insurance companies ensure the accuracy of their plethora of data

Modern analytical methods are required to process these sets of information. The term “big data has evolved to describe the quantity of information analysed to create better outcomes, business improvements, and opportunities that leverage all available data. As a result, big data is not limited to the challenges thrown up by the five Vs. Today there are two key aspects to big data:

- Data: This is more-widely available than ever because of the use of apps, social media, and the Internet of Things

- Analytics: Advanced analytic tools mean there are fewer restrictions to working with big data

The understanding of Artificial Intelligence AI has evolved over time. In the beginning, AI was perceived as machines mimicking the cognitive functions that humans associate with other human minds, such as learning and problem solving. Today, we rather refer to the ability of machines to mimic human activity in a broad range of circumstances. In a nutshell, artificial intelligence is the broader concept of machines being able to carry out tasks in a way that we would consider smart or human.

Therefore, AI combines the reasoning already provided by big data capabilities such as machine learning with two additional capabilities:

- Imitation of human cognitive functions beyond simple reasoning, such as natural language processing and emotion sensing

- Orchestration of these cognitive components with data and reasoning

A third layer is pre-packaging generic orchestration capabilities for specific applications. The most prominent such application today are bots. At a minimum, bots orchestrate natural language processing, linguistic technology, and machine learning to create systems which mimic interactions with human beings in certain domains. This is done in such a way that the customer does not realise that the counterpart is not human.

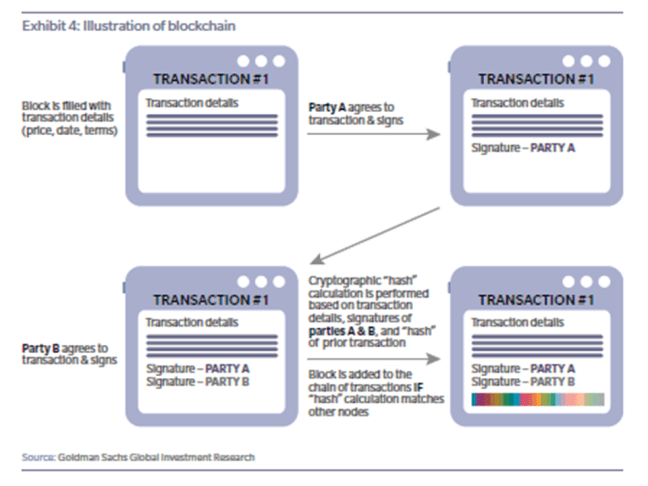

Blockchain is a distributed ledger technology used to store static records and dynamic transaction data distributed across a network of synchronised, replicated databases. It establishes trust between parties without the use of a central intermediary, removing frictional costs and inefficiency.

From a technical perspective, blockchain is a distributed database that maintains a continuously growing list of ordered records called blocks. Each block contains a timestamp and a link to a previous block. Blockchains have been designed to make it inherently difficult to modify their data: Once recorded, the data in a block cannot be altered retroactively. In addition to recording transactions, blockchains can also contain a coded set of instructions that will self-execute under a pre-specified set of conditions. These automated workflows, known as smart contracts, create trust between a set of parties, as they rely on pre-agreed data sources and and require not third-party to execute them.

Blockchain technology in its purest form has four key characteristics:

- Decentralisation: No single individual participant can control the ledger. The ledger

lives on all computers in the network

- Transparency: Information can be viewed by all participants on the network, not just

those involved in the transaction

- Immutability: Modifying a past record would require simultaneously modifying every

other block in the chain, making the ledger virtually incorruptible

- Singularity: The blockchain provides a single version of a state of affairs, which is

updated simultaneously across the network

Oliver Wyman, ZhongAn Insurance and ZhongAn Technology – a wholly owned subsidiary of ZhongAn insurance and China’s first online-only insurer – are jointly publishing this report to analyse the insurance technology market and answer the following questions:

- Which technologies are shaping the future of the insurance industry? (Chapter 2)

- What are the applications of these technologies in the insurance industry? (Chapter 3)

- What is the potential value these applications could generate? (Chapter 3)

- How can an insurer with strong technology capabilities monetise its technologies?

(Chapter 4)

- Who is benefiting from the value generated by these applications? (Chapter 5)

Click here to access Oliver Wyman’s detailed report