The overall picture that emerges from our InsurTech Radar is, first of all, that different business model categories vary significantly in terms of overall level of economic attractiveness and degree of startup activity. While some see little startup activity, others already appear overcrowded. The number of InsurTechs active in a category is not always in line with its relative attractiveness.

Secondly, even in the most attractive business model categories, it is not clear that InsurTechs will disrupt the industry and make the race. The players most likely to succeed vary by category. InsurTechs will not always be the winners. There are several categories in which either incumbents embracing digital change or firms from outside the insurance industry are most likely to succeed.

Thirdly, a number of underdeveloped categories present attractive opportunities. To be successful in these areas will require innovators to get creative on “demand side” thinking creating models that fundamentally change how risk coverage is presented and sold to customers, models that are not merely digital updates of traditional or slightly altered insurance propositions. Such thinking – substantially different from the “supply side” models of the current, first wave of InsurTechs – is essential for uncovering latent customer demand for risk cover.

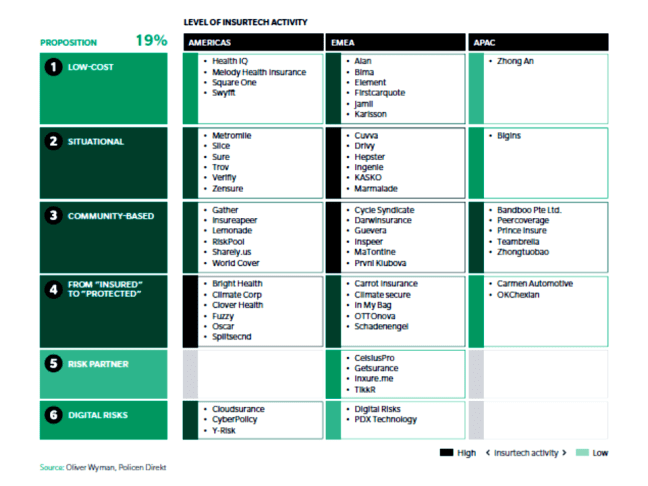

Segment 1: Proposition

The proposition segment is less than half the size of the others. It is also the most varied in terms of outlook. The InsurTech Radar shows that there is currently a major mismatch in this segment between the categories with the highest level of startup activity and those with the greatest overall potential. Examples include Situational and Community-Based business model categories which we see as over-emphasized. Nevertheless, the proposition segment includes some of the most attractive categories of any InsurTech segment, as they represent true innovation on how risk coverage is presented and sold to customers – some of these currently see relatively little activity so far (such as the Risk Partner business model category). While the news here is good for established insurers, in that they are likely to be the winners in several of these attractive categories, it is also quite clear that InsurTechs are here to stay. The emergence of newly funded and fully digital insurance carriers might bring forward real breakthroughs. It is very likely that the segment will look quite different in a few years.

Segment 2: Distribution

The InsurTech Radar shows the distribution segment to be much better matched in terms of the level of activity and the categories with the highest likelihood of success. On the down side, all but two of these areas have, comparatively only moderate potential at best, due either to limited premium pools, challenges in sustaining value generation, little opportunity for differentiation, or some combination of these (such as B2C Online Brokers). As in the proposition segment, some of the most crowded categories are also likely to see a shakeout.

Segment 3: Operations

The operations segment is the most consistent of the three: Only one business model category here currently shows limited potential (the “Balance Sheet / Financial Resource

Management” category). Most others are highly attractive. InsurTechs are likely to dominate the segment, albeit sharing honors in the underwriting category with reinsurers.

Oliver_Wyman_and_Policen_Direkt_Global_InsurTech_Report_2017