Digital transformation doesn’t stop creating surprise, admiration, innovation … but also deception and divide. In 2023, Gen AI has taken the lead regarding use, high speed engagement, discovery, and implementation.

How Tech Executives Rank Other C-suite Leaders’ Digital Skills and Mindset

They give the highest marks for proficiency and mindset (the ability to imagine digital solutions)

to chief marketing, strategy and operations officers and CEOs among non-tech roles – and rank legal

and HR leaders lowest, on average. Several potential reasons could explain this « gap »:

- one of it probably being the traditionally less developed business partnership among CTO/CIO functions and HR and especially Legal departments as these functions either work with robust legacy or with low or no IT solutions to produce their output;

- another root cause of underestimated « mindset » and « proficiency » might be stronger compliance requirements usually existing for HR and Legal functions, requirements natively less open for technical disruption;

- finally, both functions are frequently « (dis)qualified » by IT management as being too « open to shadow IT » solutions.

Three-Quarters of CEOs Have Tried ChatGPT Since Its Launch

A third of chief executives who have used the tool for work used it for writing and communication. More than 20% have employed it for general research, followed by market research and presentations (13% each).

Definitely a great start compared to significantly lower C-level adoption of previous IT innovations and disruptions. However, given the extremely broad potential among all other functions within an organization, from front lines to back office and all support functions, it’s critical to involve executives and boards in all inititiatives identified or to be identified as critical and potentially disruptive and/or transformative for the organizations future.

Otherwise, the risk to underestimate value and underallocate investments could be huge (e.g. past experience with social network, IoT, data science … too often considered being « for their kids or for freaks » than for their organizations and business).

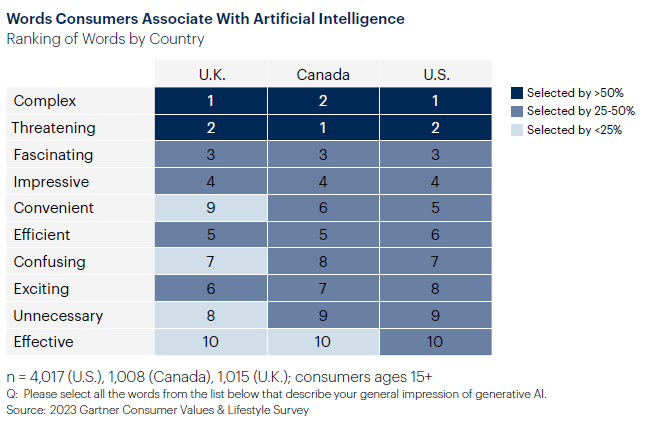

As Executives Laud AI, Consumers in the U.K., Canada and U.S. Express Fear

More than half of consumers in all three countries chose “complex” and “threatening” to describe AI, while “effective” was the least-selected word.

Not really a surprise as Big Tech is considered being a cunsumer unfriendly « oligopoly » after the skyrocketing of their market capitalization since Covid.

Fastly growing data privacy issues and cyber security incidents naturally add concerns regarding this technological disruption mainly built on Big Data and AI usage most consumers didn’t imagine prior to ChatGPT going mainstream.

How to Cope With Global Digital Divides

At least four digital infrastructures are emerging as ideology splits the world — in China, the U.S., the EU, and Russia. After three decades of global consistency for multinational companies, this shift has radical implications for business.

The number of national policies restricting data flows or access more than doubled from 2017 to 2021. With AI regulation following the same path, hoping this divided world will “return to normal” is futile. And a purely tactical C-suite response to one digital policy at a time is too costly.

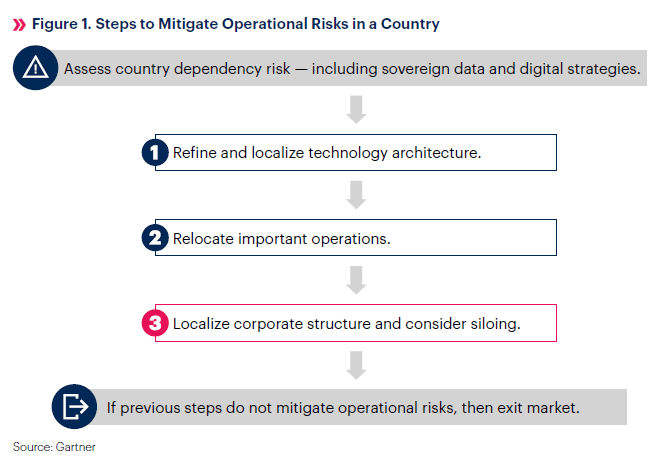

To reduce risks to growth, executive leaders should instead view geopolitical and digital tensions strategically while reacting to measures in specific jurisdictions. That means:

- Adjusting local enterprise technology architectures, operating models and corporate structures as needed

- Exiting the market as the final resort if following the steps outlined in Figure 1 does not sufficiently mitigate operational risks

Assess Country Dependency Risk — Including Sovereign Data and Digital Strategies

Executive leaders should first determine the business impact of geopolitical and digital risks in a country — including regulations — and consider appropriate mitigating steps. For example, some

multinational enterprises that continued to operate in Russia after February 2022 had to adjust their technology stack when one or more of their technology suppliers left the country.

Many multinational organizations are assessing the potential for a similar problem to arise in other regions of high tension. They also now need to manage China’s Personal Information Protection Law (PIPL) and India’s new Digital Personal Data Protection Act (passed in August 2023 but not yet effective) while remaining compliant with the EU’s general data protection regulation (GDPR).

Because digital technology is central to business, digital regulations affect almost everything a company does (as well as nearly all consumers and public-sector activities). Executive leaders must, therefore, take a broad view of how their enterprise uses data (see Figure 2).

Evaluate your digital risk in a country using Figure 2 as a guide. Take each element as a potential risk area you need to gauge due to one or more sovereign data and digital regulations. While this process will depend on where and how your company operates, a standardized assessment across all elements will help you make consistent, actionable changes faster at a strategic level.

Executive leaders addressing the enterprisewide impact of increasing digital regulations should:

- Identify the business scenarios and outcomes that are hardest to govern because of, for example,

geographic and organizational diversity, complexity and autonomy. - Consider establishing a virtual team to govern data and analytics throughout business functions and across geographies to address one of these situations. Using this connected governance framework will involve creating a proof of concept to test the benefits, risks and impacts associated with the scenario.