The Geneva Association 2018 Customer Survey in 7 mature economies reveals that for half of the respondents, increased levels of trust in insurers and intermediaries would encourage additional insurance purchases, a consistent finding across all age groups. In emerging markets this share is expected to be even higher, given a widespread lack of experience with financial institutions, the relatively low presence of well-known and trusted insurer brands and a number of structural legal and regulatory shortcomings.

Against this backdrop, a comprehensive analysis of the role and nature of trust in insurance, with a focus on the retail segment, is set to offer additional important insights into how to narrow the protection gap—the difference between needed and available protection—through concerted multi-stakeholder efforts.

The analysis is based on economic definitions of trust, viewed as an ’institutional economiser’ that facilitates or even eliminates the need for various procedures of verification and proof, thereby cutting transaction costs.

In the more specific context of insurance, trust can be defined as a customer’s bet on an insurer’s future contingent actions, ranging

- from paying claims

- to protecting personal data

- and ensuring the integrity of algorithms.

Trust is the lifeblood of insurance business, as its carriers sell contingent promises to pay, often at a distant and unspecified point in the future.

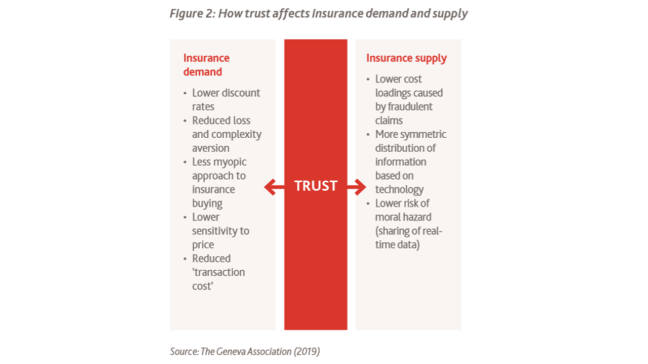

From that perspective, we can explore the implications of trust for both insurance demand and supply, i.e. its relevance to the size and nature of protection gaps. For example, trust influences behavioural biases such as customers’ propensity for excessive discounting, or in other words, an irrationally high preference for money today over money tomorrow that dampens demand for insurance. In addition, increased levels of trust lower customers’ sensitivity to the price of coverage.

Trust also has an important influence on the supply side of insurance. The cost loadings applied by insurers to account for fraud are significant and lead to higher premiums for honest customers. Enhanced insurer trust in their customers’ prospective honesty would enable

- lower cost loadings,

- less restrictive product specifications

- and higher demand for insurance.

The potential for lower cost loadings is significant. In the U.S. alone, according to the Insurance Information Institute (2019), fraud in the property and casualty sector is estimated to cost the insurance industry more than USD 30 billion annually, about 10% of total incurred losses and loss adjustment expenses.

Another area where trust matters greatly to the supply of insurance coverage is asymmetric information. A related challenge is moral hazard, or the probability of a person exercising less care in the presence of insurance cover. In this context, however, digital technologies and modern analytics are emerging as potentially game-changing forces. Some pundits herald the end of the age of asymmetric information and argue that a proliferation of information will

- counter adverse selection and moral hazard,

- creating transparency (and trust) for both insurers and insureds

- and aligning their respective interests.

Other experts caution that this ‘brave new world’ depends on the development of customers’ future privacy preferences.

One concrete example is the technology-enabled rise in peer-to-peer trust and the amplification of word-of-mouth. This general trend is now entering the world of insurance as affinity groups and other communities organise themselves through online platforms. In such business models, trust in incumbent insurance companies is replaced with trust in peer groups and the technology platforms that organise them. Another example is the blockchain. In insurance, some start-ups have pioneered the use of blockchain to improve efficiency, transparency and trust in unemployment, property and casualty, and travel insurance, for example. In more advanced markets, ecosystem partners can serve as another example of technology-enabled trust influencers.

These developments are set to usher in an era in which customer data will be a key source of competitive edge. Therefore, gaining and maintaining customers’ trust in how data is used and handled will be vitally important for insurers’ reputations. This also applies to the integrity and interpretability of artificial intelligence tools, given the potential for biases to be embedded in algorithms.

In spite of numerous trust deficits, insurers appear to be in a promising position to hold their own against technology platforms, which are under increasing scrutiny for dubious data handling practices. According to the Geneva Association 2018 Customer Survey, only 3% of all respondents (and 7% of the millennials) polled name technology platforms as their preferred conduits for buying insurance. Insurers’ future performance, in terms of responsible data handling and usage as well as algorithm building, will determine whether their current competitive edge is sustainable. It should not be taken for granted, as—especially in high-growth markets—the vast majority of insurance customers would at least be open to purchasing insurance from new entrants.

In order to substantiate a multi-stakeholder road map for narrowing protection gaps through fostering trust, we propose a triangle of determinants of trust in insurance.

- First, considering the performance of insurers, how an insurer services a policy and settles claims is core to building or destroying trust.

- Second, regarding the performance of intermediaries, it is intuitively plausible that those individuals and organisations at the frontline of the customer interface are critically important to the reputation and the level of trust placed in the insurance carrier.

- And third, taking into account sociodemographic factors, most recent research finds that trust in insurance is higher among females.

This research also suggests that trust in insurance decreases with age, and insurance literacy has a strong positive influence on the level of trust in insurance.

Based on this paper’s theoretical and empirical findings, we propose the following road map for ensuring that insurance markets are optimally lubricated with trust. This road map includes 3 stakeholder groups that need to act in concert: insurers (and their intermediaries), customers, and regulators/ lawmakers.

In order for insurers and their intermediaries to bolster customer trust—and enhance their contribution to society—we recommend they do the following:

- Streamline claims settlement with processes that differentiate between honest and (potentially) dishonest customers. Delayed claims settlement, which may be attributable to procedures needed for potentially fraudulent customer behaviour, causes people to lose trust in insurers and is unfair to honest customers.

- Increase product transparency and simplicity, with a focus on price and value. Such efforts could include aligning incentives through technology-enabled customer engagement and utilising data and analytics for simpler and clearer underwriting procedures. This may, however, entail delicate trade-offs between efficiency and privacy.

- ‘Borrow’ trust: As a novel approach, insurers may partner with non-insurance companies or influencers to access new customers through the implied endorsement of a trusted brand or individual. Such partnerships are also essential to extending the business model of insurance beyond its traditional centre of gravity, which is the payment of claims.

Customers and their organisations are encouraged to undertake the following actions:

- Support collective action against fraud. Insurance fraud hinders mutual trust and drives cost loadings, which are unfair to honest customers and lead to suboptimal levels of aggregate demand.

- Engage with insurers who leverage personal data for the benefit of the customer. When insurers respond to adverse selection, they increase rates for everyone in order to cover their losses. This may cause low-risk customers to drop out of the company’s risk pool and forego coverage. ‘Real time’ underwriting methods and modern analytics are potential remedies to the undesirable effects of adverse selection.

Recommendations for policymakers and regulators are the following:

- Protect customers. Effective customer protection is indispensable to lubricating insurance markets with trust. First, regulators should promote access to insurance through regulations that interfere with the market mechanism for rate determination or through more subtle means, such as restrictions on premium rating factors. Second, regulators should make sure that insurers have the ability to pay claims and remain solvent. This may involve timely prudential regulatory intervention.

- Promote industry competition. There is a positive correlation between an insurance market’s competitiveness and levels of customer trust. In a competitive market, the cost to customers for switching from an underperforming insurance carrier to a more favourable competitor is relatively low. However, the cost of customer attrition for insurers is high. Therefore, in a competitive market, the onus is on insurers to perform well and satisfy customers.

Click here to access Geneva Association’s Research Debrief